It is a truism of current pension policy that the DWP deliberates and the Treasury pulls the trigger.

The Treasury approach certainly attracts headlines but will create casualties “through ignorance, weakness or our own deliberate fault”.

Nowhere will the blood be spilt as it will be post April as the entire population of those who have ever reached 55 with a DC pot will be in a position to release some “sexy-cash” from their pensions.

How “Sexy-cash” has been turned from evil inducement to healthy incentive

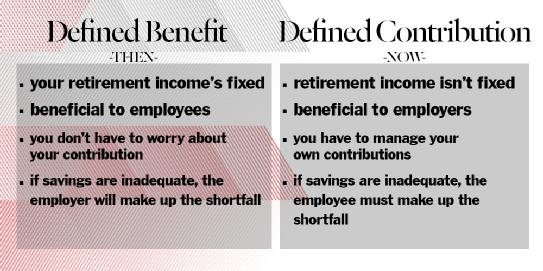

Sexy-cash is not my term, it is a term used by Steve Webb to describe the cash inducements that were used to lure people away from the guarantees in their DB plans. Only a couple of years ago, the idea that cash inducements might be used as a means to freedom would have been laughed out of court.

Add to the 6m who are in possession of an income secured by an annuity purchase, the 400,000 reaching 55 this year and a proportion of those yet to draw their DB pensions (up to 8% of those in funded DB (Hargreaves Lansdowne) and you get an idea of the carnage that could ensue.

The problem is that while we’re all dressed up- we have nowhere for our money to go.

There are not enough financial understand (see my article on this, this week)

There is not enough advice

There is no obvious product for the silent majority of us who have no wish to buy annuities and no capacity or appetite to manage our own self-invested income drawdown arrangement.

Redington have been writing about the shift in responsibility from collective to individual

We are like the young men of England and Germany marched off to Flanders from 1914. We might think this is collective endeavour but once the whistle blows it’s every man for himself.

George Osborne reminds me of General Melchett ordering his men out of the trench into the teeth of enemy gunfire. Except Blackadder was a comedy.

This battlefield needs tanks, this ship-wreck lifeboats!

In the face of the carnage to come, the bloodbath created by the office of pension irresponsibility (the name by which the Treasury should be known) , we need a lifeboat , or to extend my analogy, a tank behind which we can hide.

We need a middle way product between drawdown and annuity that looks like a pension but has property rights so people can move into an annuity, into drawdown, or just cash out.

We know for research done by Aon and the DWP that around 70% of us, when asked what we want from our pension pot , describe a pension.

The only way that we can offer more than an annuity, without the uncertainty of a drawdown is through a non guaranteed target pension – what is referred to as CDC.

Unless we have a clear purpose for CDC- we should mothball it.

But with the print still wet on the Pension Scheme Act that allows CDC to happen, Dame Ann Begg, Chair of the DWP Select Committee on Pensions called for a halt to work on the secondary legislation on CDC.

She also calls for a review of just about everything else going on right now which is like trying to direct the traffic at Spaghetti junction!

I am not overly concerned by calls for policy changes within 50 days of a general election, all now is just political posturing, but I am concerned that Dame Ann Begg, who is an extremely able politician, has not had the opportunity to understand just why CDC is so relevant to the problems we are and will face.

Those of us who are Friends of CDC (and we are meeting the DWP next week to discuss this issue) need to be absolutely clear about the relevance of our product.

We must dispel myths we have created and allow to malinger to the detriment of CDC and our pension system.

CDC is not a means to replace DB (though it could be used to de-risk the most derelict schemes as it has been in Canada (New Brunswick).

Nor is CDC a means to replace DC workplace pensions (which are working very well thank you)

CDC is the tank behind which we can move across the battlefield

CDC is the tank behind which we foot soldiers ,out of our trenches, can move forward. CDC is a means for us to receive more income from our pension pot than we can purchase from an annuity and more security than we can extract from income drawdown.

CDC is a means of collectively insuring ourselves against living too long, while offering those who do not want to join the pool to bet individually underwritten for an enhanced individual annuity.

CDC is a means of having something that works like a DB pension but with the option of cashing out at any time.

In short, CDC is the answer not the problem. To stop working on CDC would be as crass an error as IBM ignoring personal computers or Nokia not building a smartphone.

The reason that Dame Ann Begg and the DWP select committee see CDC as a luxury that can be mothballed is because they have not been misled about what CDC should be.

But CDC and employers don’t mix

So let me make this absolutely clear. CDC is not going to work as an employer sponsored product. That is because employers do not want to participate in any pension where there is a risk (however remote) that they might be responsible for the member outcomes.

CDC will not work if employers have to pay into it or even be deemed a “participator”. Nor will it work as a group of personal pensions. The two existing pension structures which dominate private pensions are simply not fit for the purpose of clearing up the carnage of pension freedoms.

We don’t just need CDC, we need CDC in a new pension product that has the collective properties of an occupational pension scheme but the separation from the employer of a personal pension.

Into such a structure can be tipped the proceeds of our DC saving. Like the farmers in a European commune bringing their grapes to the collective vinery, we can exchange our money for pension.

The structure I am talking about actually exists, there is a statutory instrument on the DWP’s statue books which allows a Regulatory Own Fund (ROF)to be created for undefined purposes. As I understand it, a ROF is no more or less than a super trust like the Pension Protection Fund, set up by Government for the public good.

The ROF is my tank, or my lifeboat if I want to switch from the battlefield to the shipwreck.

CDC is the means of salvage and- much better- the means of salvation.

The simple solution to Dame Ann Begg’s problem!

You may wonder why Dame Ann Begg and the DWP Select Committee do not know about all this. You would be right to wonder- I wonder too. I don’t understand why many of our Friends of CDC keep peddling the idea of CDC as a replacement for DB or for workplace DC. Nor do I understand why they want to make CDC employer sponsored.

CDC – to work – must have nothing to do with employers. All employers need to do is signpost Pension Wise, or in extremis, explain that CDC exists.

All the Government needs to do is to allow this paired down vision for CDC to be created through secondary legislation created within the DWP by their excellent policy team.

So long as CDC is targeted at the problem – the carnage of pension freedoms and not the success story (DC workplace pension saving schemes), it is hugely relevant.

If it is billed as an alternative to employers to DC and DB, it will be irrelevant and should be binned.

It is as simple as that.

Henry

Your analogy of the Co-Op vinery is interesting. The village where I live in Spain they grow olives, and I mean lots of olives. For years the growers of the village have used a Cooperative where they took their grapes to be pressed into oil and sold along with all the other villages in the region. However, the they are now starting to band together into smaller entities as the Cooperative they have used for years has grown to big and unwieldy, (they have to wait 12 months to be paid). Conclusion, big is not always best.

Now where did I put my Martini?