It could be the trending chant at any event that Alex Ferguson turns up to – a taunt to a man who having lost control has seen slump into mundanity in a few short months.

Financial wellbeing in later life

But football is not the subject of this blog- retirement is and in particular thoughts on Financial wellbeing in later life. This is the title of a quite excellent piece of research launched jointly by the University of Bristol , SDAI and the International Longevity Centre and downloadable from the link.

I attended yesterday’s launch which had as its theme (and twitter hashtag) “balancing the books”. At half time, after the research had been presented and before the bun fight on equity release schemes had begun, I had a conversation with one of the academics about why I was there.

Why was I there?

It seemed totally obvious to me, I advise people on planning for retirement, my job is about getting people to prepare for “financial wellbeing in later life”. The report sets out to provide data from over 20,000 people on

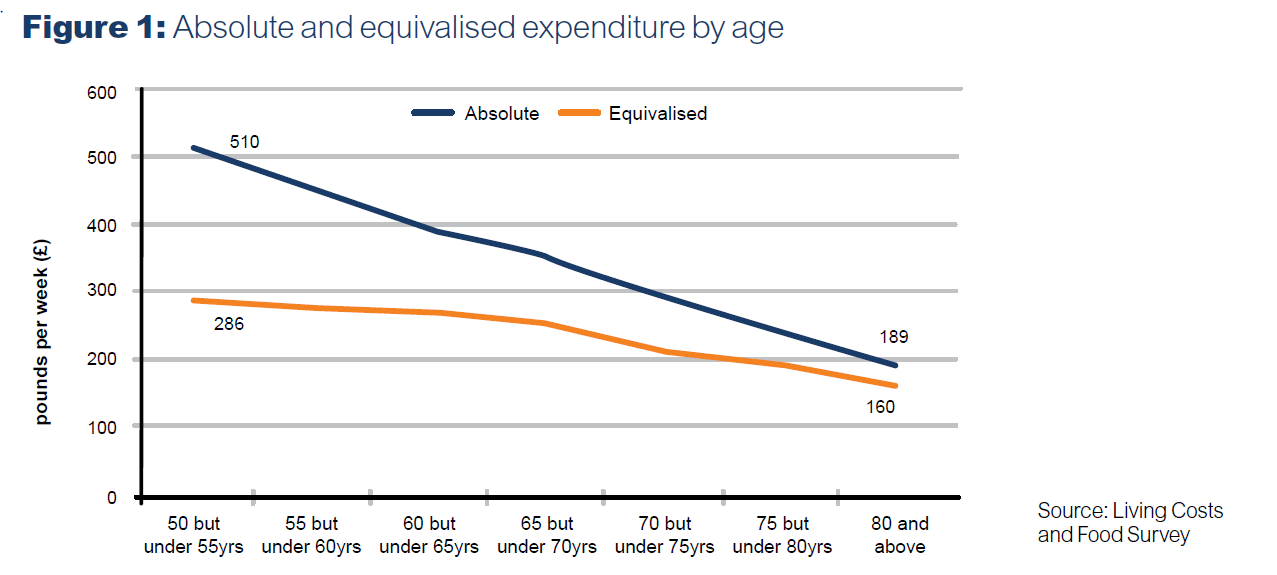

- What do older people spend their money on?

- What are the main patterns of spending among older customers?

- What mortgage borrowing’s going on in older households?

- What other types of debt are older households taking on?

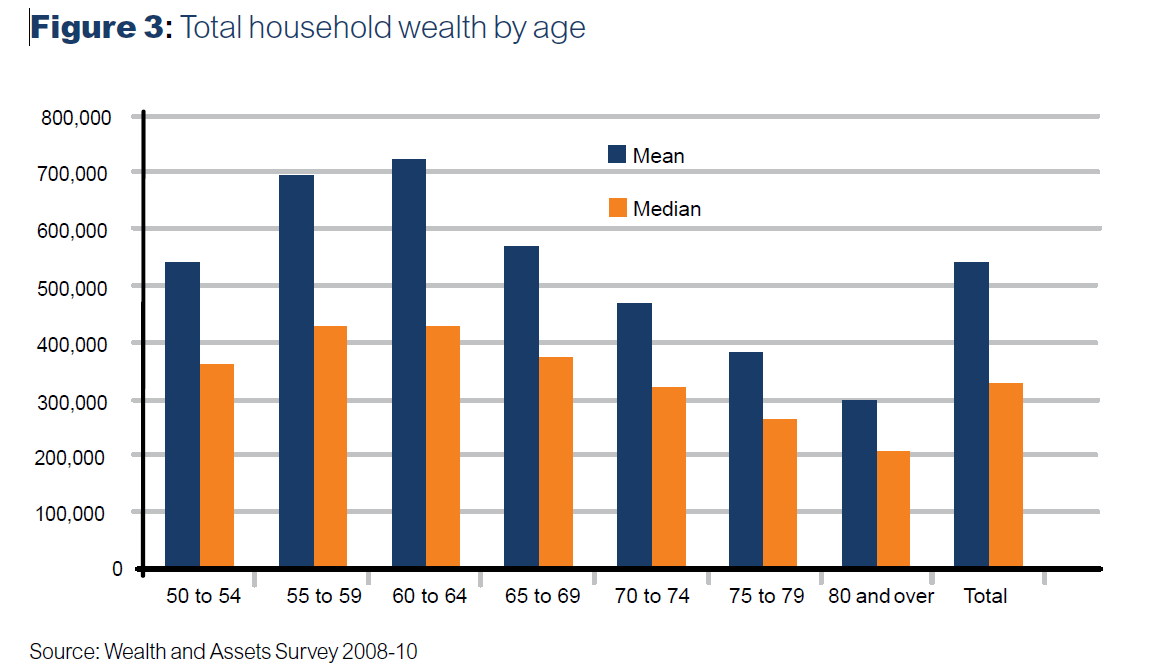

- What is the composition of older people’s wealth?

- What’s the connection between having money and being healthy for older people?

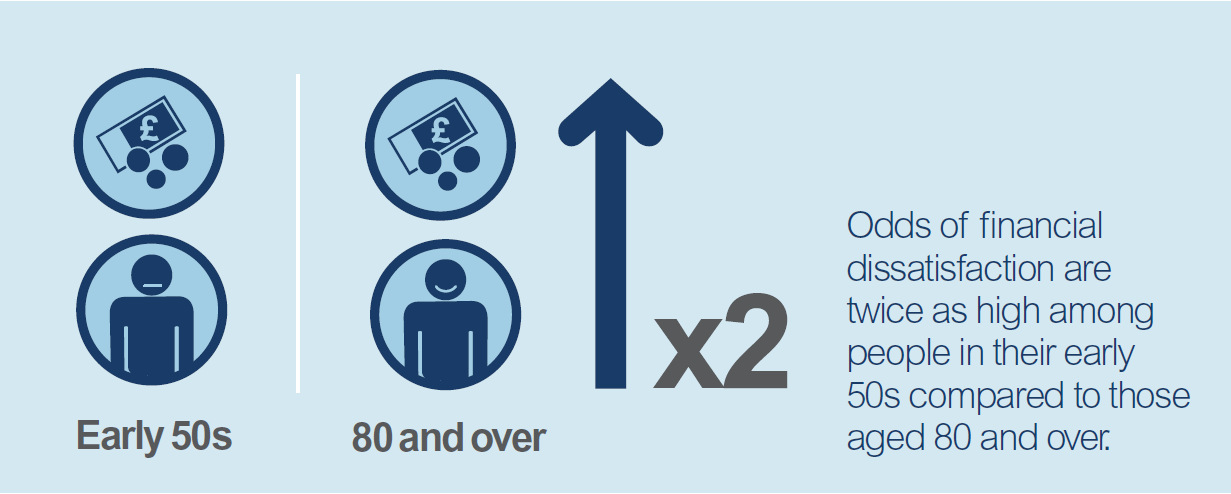

- Are older people financially satisfied and does this make them happy?

- What makes for quality of life in later life?

- How is quality of life affected by having or not having money?

- What can be done to work out causal (chicken and egg) issues?

Why can’t every retirement debate be like this?

Frankly, if the NAPF made this their agenda I would be going to the conference – even at their extreme conferences. These are questions of real importance about which I would pay big money to be better informed. My livelihood should depend on being able to understand these questions and provide people preparing for retirement with not the questions, but the answers!

Yet the room was full of academics and virtually void of financial practitioners!

Some of the insights I gained yesterday are so valuable that, were I not the sharing type, I would keep to myself and use for my and my firm’s commercial advantage.

Chicken or egg?

And yet, even within the audience there was dis-satisfaction. There was dis-satisfaction over question ten, someone wanted to know whether older people are more likely to get ill because they’re skint or whether older people become skint because they’re ill. It’s a good question but one for another day. Common sense says it’s a bit of both and I’m sure that’s what the research would say. But my point is that even considering the question got me thinking how I could get younger people to think about the importance of keeping healthy by being wealthy and vice versa- that’s a strap that any IFA could use!

Is this what it’s like or just a passing trend?

Others were concerned about the paucity of “longitudinal” research, that’s the research into how people change in retirement – so if you follow me at 52 and 57 and 62 and 67 (and many like me), you can find out whether the snapshot of 2014, 2019 etc represents circumstances particular to the time or whether what I’m going through as a 67 year old is the same as all 67 year olds for all time. I agree- this kind of research is even more brilliant than the snapshot stuff that was mostly served up in the report.

But let’s not look a gift-horse in the mouth! Here –served up for free- is a source book for anyone interested in Financial Education whether they be IFA, or EBC or Actuarial Consultant or one of the third sector advisers that Laurence Churchill suggests we’ll be relying on going forward (MAS,TPAS,CaB take a bow – on you we dump).

So what’s to be done?

I have three takeaways from this conference

- The most brilliant report that I’m going to read and read and read because it teaches me how to do my job

- The realisation that most of my competitors are missing a trick (hurrah!)

- That sadly, the financial services industry is simply not listening to its customers.

Of these, from a macro perspective, the third is the most important. The findings of this report, based on a magnificent data set and superb work by world-leading social scientists, demographers and gerontologists, should be on every bank and insurance company’s agenda today, this year and going forward. Until we shape policy and design products around the needs of elderly people and not around what will sell, politicians and financial services companies will bark up the wrong trees.

I do not know what it will be like for me in retirement, but reading this paper, I can have a much better informed view. My clients, the employers who fund the financial education courses we run and the staff who attend those courses are not looking for me to pander to what they don’t know- they are looking for what I do know- and they are paying for informed comment.

I would urge anyone who is in the business of preparing themselves and others for later life, to spend time with this document and to spend more time thinking “what’s it like to be retired”.

This post was first published in www.henrytapper.com (top thinking)