The Pension Regulator has published an interesting document entitled “A quick guide to selecting a good quality pension scheme for auto-enrolment”. Reading it, I was conscious of just how hard the Regulator is trying to get people to take the right decisions about pensions and it is absolutely right when it asserts.

You should also choose a good quality

pension scheme that is well run, offers

value for money and protects your workers’

retirement savings. Selecting a good quality

pension scheme is not a difficult process and,

from your perspective, it doesn’t have to

cost more than a scheme which is of a lesser

quality.

As the title suggests, this is a DIY manual for employers who are coming afresh to the subject and it’s very well written. Instead of using intimidating language, it uses terms saving in it. that everyday people would use and it’s refreshingly candid.

But it is written from a sometimes odd perspective.. take this

You may be offered the option of setting up

a new trust-based scheme if you are using

the services of a financial adviser. This would

involve your organisation providing a board

of trustees who run the scheme. Our evidence

suggests that most employers will find that

it is not cost-effective to set up this type of

scheme unless it has at least 1,000 people

I am a financial adviser to companies looking to set up pension schemes and I have not offered this option for some years. For exactly the reasons outlined here. It is possible to operate the defined contribution kind of pension scheme using an existing trust and sometimes this is a good idea but we are talking here of companies who have a long history of pension provision to their staff- typically on a defined benefit basis.

This odd statement got me asking “where is the author’s head?”. My conclusion as I read on was “very much in the right place”. There are a number of sections – particularly those on the safety of the pension scheme (entitle simply “Pension Provider”) and the beautifully crafted piece on “communications” which I am quoting directly in the help sections of http://www.pensionplaypen.com.

The Regulator’s document is good on explaining what features a scheme needs to be Qualify to be used as a workplace pension but light on any detail surrounding what makes for good support to an employer looking for help fulfilling “employer duties”. We suspect that it will be the Providers of workplace pensions who will do most to keep employers compliant though the Guide is silent on this.

And the author’s head has not quite got around how an employer can organise a proper comparison of the options available. This is what we call “the employer’s journey”.

The Guide asks you to click on http://www.abi.org.uk/Insurance-andsavings/Products/Pensions/Automaticenrolment/Providers and this takes you to a page listing 11 insurers two of which (Prudential and HSBC Life) no longer market workplace pensions to the general customer. The list is incomplete (in relation to insurers – where is Zurich, or BlackRock both of which run AE arrangements?) It contains B&CE whose workplace pension is only partially insured (People’s Pension) and of course there is no mention of the mastertrusts like NOW and BlueSky.

NEST are given pride of place and there own website address.

My impression is that when it comes to understanding the legal governance of workplace pensions, the Pension Regulator’s Head is in the right place. But when it comes to understanding how to go about getting help in selecting a pension, the Regulator’s head is scrambled!

It is high time that a long-list of providers of DC workplace pensions generally available to the public was published. We include talking about the excellent Plumber’s Scheme (which is DB) and one or two very small mastertrusts which we have not researched but here is the Pension Plowman’s list of workplace pension providers whose wares are within my terms of reference.

Aegon

Aviva

BlackRock Contract and Mastertrust

BlueSky

Fidelity Contract and Mastertrust

Friends Life

Legal and General Contract and Mastertrust

Merchant Navy Officers Pension Plan

National Pensions Trust

NEST

NOW Pensions

Pensions Umbrella Trust

Plumbing and Mechanical Services UK Pension Scheme

Salvus

Scottish Life

Scottish Widows

The Pensions Trust

Standard Life Contract and Mastertrust

Supertrust UK

Welplan

Zurich Contract and Mastertrust

Where there is a huge gap in the “employer’s journey” is in getting to a position where employers can properly understand what is available to them. I am not being rude about the Pensions Regulator (hi!), I am simply pointing out that, as with their earlier comment about what advisers advise on, they simply don’t understand DC distribution (which is what the FCA are supposed to do -but don’t either).

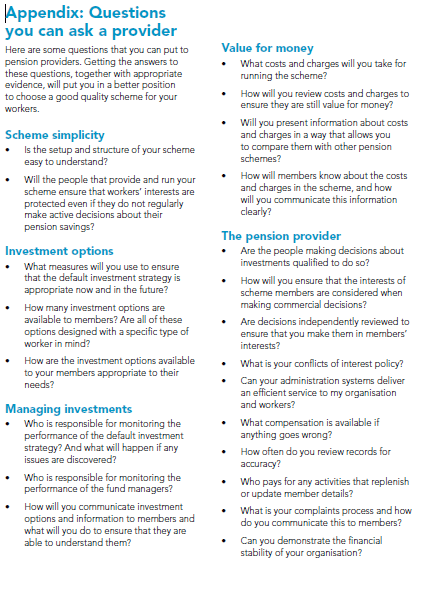

The Regulator’s Guide finishes with a number of questions you can ask Providers.

These are the right questions, but how do you find your providers?

For an answer to that question click on https://www.pensionplaypen.com/choose-new-pension . We haven’t fully launched our new service yet (we are expecting to in September) but we are getting there. When we do, we intend to incorporate the wisdom of the Pension Regulator! I thoroughly recommend this document to any employer.

This article first appeared at https://www.pensionplaypen.com/top-thinking/show/104/the-regulator-offers-employers-help-in-choosing-a-workplace-pension.html

I find this guide interesting but, in parts, off the rails. In general terms it is keen to point out how simple it is to choose a scheme, but even as a pension adviser, the areas that need to be covered are quite complex. Good luck to any employer armed only with this document. I’m also a little perplexed as to what happened to the principles and outcomes previously published?

A few comments I would have regarding this most recent guide are: under the section on scheme quality, tPR states – “so we have asked all pension scheme providers to make sure their schemes are designed in a way which is tailored to the needs of your workers. “ What does that mean? Can we just use anyone then, if they’re all ok?

Secondly, under value for money, it states “some services that pension providers offer may make the scheme more expensive but can add value to the scheme for your workers. These include administration services, technology platforms, higher quality communications or more support from members as they approach retirement.” Again I’m not entirely sure what this means – surely these should be provided as part of any decent pension scheme? How can you have a pension scheme without administration services or a technology platform to access it?

Generally, I’m more concerned now, following review of this guide, that pension providers are building in auto enrolment compliance software for “free” but including it within a higher annual management charge for workers and claiming this represents reasonable value for money. Can they use the statement above to justify this approach?

I think auto enrolment compliance software, like consultancy charging, is an employer cost and should be borne by the employer. If consultancy charging is being banned, so should AE compliance software charges sitting with the workforce.