Today’s the day those over 55 can start taking their pension pots as they like;-

- except you can’t because the insurance companies are closed for the Bank Holiday

- except your defined contribution pension provider may not have adapted its systems yet

- except you should still be in bed

- and then have a conversation with Pension Wise

- and probably take financial advice

Most people are positive about pension saving

Whatever happens over the next few weeks, we’ll have the case study on Britain’s financial prudence/fecklessness or apathy.

This simple video can help you make your mind up about what is best for you

Your 3 pension options in 3 minutes from QR on Vimeo.

The last time we had such a pension plebiscite, we found- to our amazement that – we were all in. Well nearly all!

Those who have most to win from the pension freedoms- certainly from a tax point of view- are those over 50 with no pension savings and little prospect of retirement income. Ironically, this group of workers has been most reluctant to pick up the free money available from the taxman and their employers.

But too many older workers are giving up on pensions

Amidst all the noise about scams and Lamborghinis, spare a thought for the 23% of the over 50s who opted out of auto-enrolment. You can read the Government’s report on older people’s attitudes to pension saving here.

People cited

- concerns about affordability

- they already had enough in retirement

- they were too close to retirement

- contribution rates were too low

- were thinking of moving employers

- were concerned about pensions as a means of saving

For the vast majority of the over 50s opting out, it looks as this decision will be a bad decision which will only benefit employers and tax-payers. Almost all these excuses for not saving look feeble, certainly for those who do not have substantial savings “in a pension”.

What’s more, these look the most vulnerable group for whom the time to save is running out and the prospect of long-term poverty in retirement is greatest.

Should we be sending Panorama after these people? Should they be hounded by pension experts wagging their fingers? Should their employers be exposed for allowing these decision to be taken on their watch?

We should not.

We should trust people with their own money. We should trust the free independent guidance from Pension Wise. We should not be pointing fingers.

The upgraded state pension should be enough to ensure that the vast majority of people will not be a burden on the next generation or indeed on other members of their generation.

Most people build up more in state benefits than in private pensions, especially if you count civil service and local Government pensions as part of the state system.

Stop wagging that finger!

The bad mistakes that people make, whether in failing to pick up free money as they work, or in giving back tax relief when they retire or (in the worse case) blowing their money on some idiotic investment, are those people’s to make.

There is a proper system of controls in place, including the guidance from Pension Wise . People want choice but don’t want to take irreversible decisions. For the most part, the choice people will take will be to work longer, save harder and wait till a viable pension option comes along.

Start making pension spending easier!

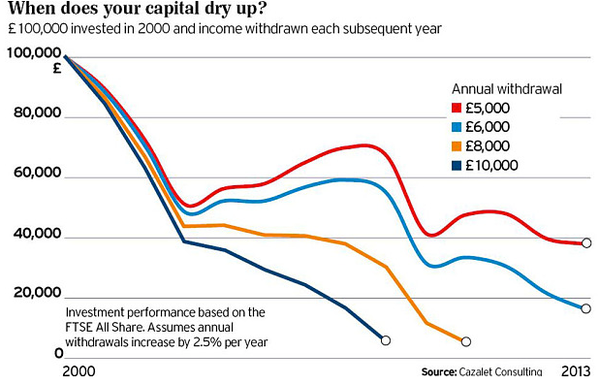

We really have to bring down the cost of spending our pension savings. The cost of annuities, the cost of drawdown and the cost of advice are too high for people with limited pension wealth. To independently manage an income through the whole of the rest of our lives, we need to (individually) be our own chief investment officer, actuary and pension administrator. For most people that is simply not on.

We need a collective means of spending our savings and the sooner the better. A collective scheme that can be fair to all but which allows people the right to change their mind, gives peace of mind to those worried about money running out and which allows people to have confidence that their later life affairs are being properly minded.

Don’t press any panic buttons.

It took Osborne five minutes to announce but it may take five years to get the new options properly in place. Getting a new pension system in place that can allow people to spend their money through target pensions may not happen much before 2018. This is not because of lethargy among policy makers but because pension policy is complex and every change throws up many loopholes.

We must be patient.

In the meantime

There is much can be done as interim measures. Insurers and pension administrators can improve processes to help people spend their money using drawdown, annuities and the cash-out option, much more efficiently than is happening today.

New technologies make cash payments cheaper and easier. If it is possible to buy a loaf of bread in Kenya with a mobile phone, surely it should be possible in Britain to draw money from your pension via an ATM (some day soon!).

Freedom – a moral right

We are a liberal society that believe in allowing people to pursue their lives as they wish. We have constraints to protect others, but we know where to draw the line. The line was drawn in the wrong place with pensions. Annuities were killing pension savings and the pension freedoms give people back ownership of their pension pot.

The success of auto-enrolment has shown that people are not financial luddites, given the opportunity to save, they will save. The relatively high opt-out rates among the over 50s demonstrates how disaffected some older people have been by the pension system.

The task of those working in pensions over the next five years is to restore confidence in pensions. That is a huge and challenging task and it is our moral duty to help rather than hinder that process.

{kind=link}

New State Pension = £150 per week from 2016.

Housing benefit = £150 per week

Council tax ben = £20 per week

= Depending on State benefits to continue beyond 2016? Even if called Universal Credit?

I get your point about the fragility of some state benefits. Do you think that the Government are cynically using auto-enrolment to shift responsibility for the poor to the poor?

What about the millions of employees who were C/out and therefore do not qualify for the new state pension?

Hopefully the contracting out was worth it. The Contracting out deductions haven’t been finalised yet but I fear the worst!