This morning and regularly over the next few weeks, I will be speaking at Money Marketing Auto-Enrolment invitational events around Britain.

These are the slides that I will be using

The known opportunity

We know people have made money out of auto-enrolment, but that was when dinosaurs ruled the world and when you could get paid commission from the pension and when employers still had budgets to pay fees.

Competence declines

In house competence, both about pensions , payroll and HR is in sharp decline. In a year’s time, we reckon it will plateau at “low to non-existent” for those staging auto-enrolment.

The support mechanisms needed to meet the increased demand for help need are changing. The regulated adviser is having to compete to provide this help. As numbers increase, so must the support.

“I will life mine eyes unto the hills, from whence comet mine aid” (?)

Did anyone ever consider advice?

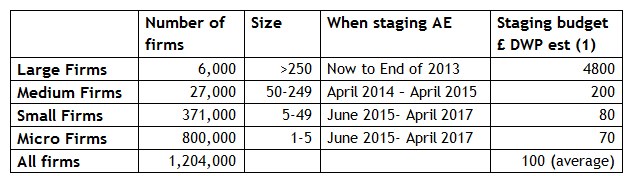

These are the numbers that the DWP didn’t want you to see, it shows what they told the Treasury auto-enrolment would cost companies.

The total AE staging budget is reckoned to be £120m, a fifth of the loan to NEST. Several large employers have reported staging costs north of £1m and we reckon the average employer is still spending £1500 today, while costs will fall in years to come, we think the minimum budget for the work should be £300.

These low-side projections have created an expectation of auto-enrolment for free. How will advisers get paid let alone make any money?

So what support do bosses want?

Unsurprisingly, bosses are looking at AE tactically not strategically. Communicating to staff and getting the pension decision right are low on the list of priorities, not getting fined by the Regulator and keeping initial and ongoing costs down are high ticket items.

It was ever thus. The adviser’s job has always been to get people to think strategically about the “what if’s” but will advisers be rewarded for selling the idea of properly communicated good pensions?

When do they want it?

Again the messages coming from NEST Insight and other sources employers mostly want help when they run into trouble and by trouble they are staring down the barrel of the game-keepers gun. Interestingly, employers appear to be fearful of choosing and setting up a pension , which is the second most “worried about item on NEST’s list

Who do they want it from?

They want support from their accountants, only 14% of NEST’s respondents said they’d be going to an IFA.

Nearly a quarter of employers said they wouldn’t be needing help.

IFA’s inside?

Though employers may think they will get help from accountants, it looks like the accountants are more than happy to palm this work off on IFAs, 73% told NEST they were already working with an IFA on this.

But is payroll cleaning up?

Our research suggests that payroll gets paid for doing this work, while IFAs struggle

IFAs are rather less keen on the auto-enrolment opportunity than payrolls and accountants aren’t very keen on it at all!

Payroll the new experts?

Payroll people may not class themselves as “knowing a lot” but they rate themselves as “knowing enough” at least about how auto-enrolment processes work

They are now able to use software provided by Sage and IRIS at a fraction of the cost and at less perceived risk than from “middleware”, the emergence of PAPDIS, the common data standard is likely to make payroll software companies and those managing bureaux, more confident about managing the pension administration.

Payroll is still fractured but is more likely to manage going forward

There are too many ways for payroll to be administered for a single auto-enrolment solution to emerge. For the meantime the adviser, with or without middleware will still have opportunities to support the payroll processing, deal with the statutory communications and help with the Pensions Regulator, but we see that more and more payroll operatives will compete for these roles.

So maybe , it is by paying attention to the pension that financial advisers make their money

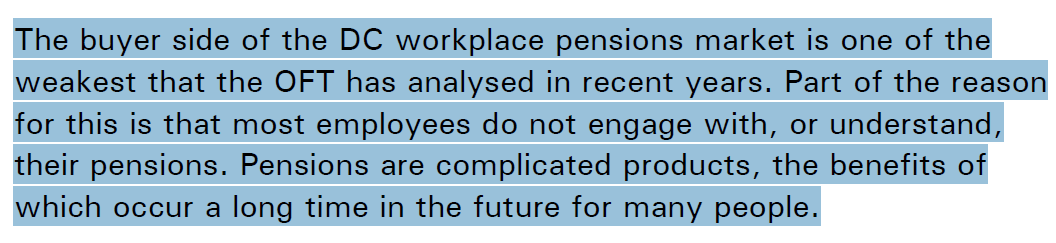

As the OFT put it

The regulatory position still favours IFAs to talk about pensions

Comments from the Regulator concerning the need for “skill and knowledge” and warnings from the ICAEW about “FSMA” have been enough to scare accountants and payroll away from advising on pensions

But , as earlier charts have shown, employers are still worried about pensions and employees still ignorant about where their money goes.

Can Financial Advisers make money out of Auto-enrolment?

I think it looks very difficult. If they can break even on the work they do , they will be the lucky ones, many advisers are seeing better opportunities elsewhere.

But if IFAs are serious about building a corporate practice, with all the advantages it brings over retail business, then it is advice on the workplace pension that could be the way to do it.