The weekend saw a disorderly queue of experts predicting how the previously simple system of default investments in workplace pensions would be complicated by the increased spending choices for people in retirement.

From 2015 people will be able to spend their savings by cashing in their chips all in one go, buying an annuity or drawing down from an individual or collective scheme. Apparently this is very complicated and will require employers to engage the services of all kinds of people to review their options and create multiple defaults to cater for each type of spend.

Wouldn’t it be wonderful if the financial services, instead of demanding we all bury our heads in our hands at the thought of all this complexity, actually promoted the positive aspects of choice.

We have a year to get this right, but before we start engineering solutions, let’s work out what the problems will be. The only way we can really design solutions is by looking at the spending patterns of those in retirement, both here and in other countries and fit solutions around them.

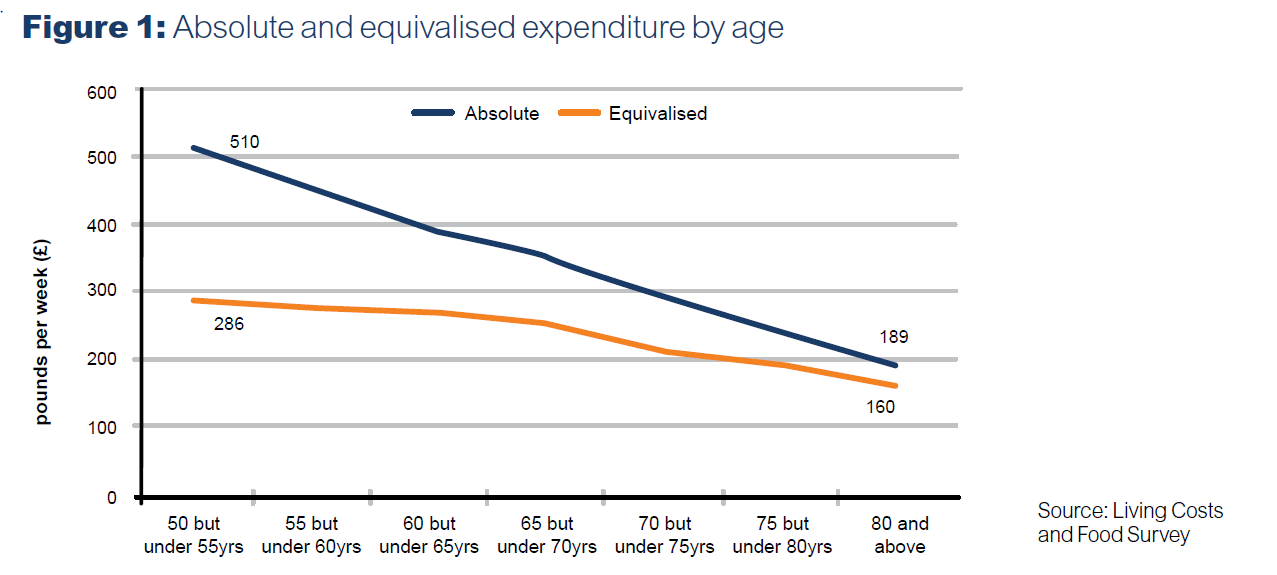

This graph shows that people do not spend in retirement as people earn before retirement. In real terms they spend less as they grow older. So while longevity may be a problem to the NHS , it is not such a financial strain to the individual (Dilmott makes this clear).

If you look closely at the way tax is structured you’ll note that there is a substantial gap between the personal allowance (including age allowance) and the guaranteed income in retirement (the single state pension). Clearly those with limited earnings in retirement will be able to draw down income into this tax free gap as tax free income or as a series of mini tax-free cash sums. Guidance for the low income is likely to be dramatically different to guidance for those who will be paying basic or higher rate tax.

Similarly those who phase their retirement may have the opportunity to defer taking income till they fall a tax bracket.

It seems absolutely clear that “premature annuitisation” will be rare as hen’s teeth, people will defer taking an annuity till the end is in sight- that may mean 97 for a fit person or a lot earlier if the health prognosis is poor.

For all these reasons, the obvious default position is to run with a “keep your choices open” investment strategy. Default lifestyles that point towards annuitisation look dead in the water, defaulting into smoothed managed funds (DGFs) look like they tick the “all things to all (wo)men” box. But calls for the death of the default are ludicrous and shout-outs for proprietary solutions at this point are counter-productive.

There may be an argument for arresting the glidepath for those actively switching from growth to protection assets at present. But we should not be frightening those in their fifties into supposing they will (after all) need to become their own CIO. We should certainly not be bouncing people out of default strategies and into home-made concoctions of funds and tactical asset allocation theories.

Now is the time to really do some thinking about what people currently do, are likely to do and would ideally want to do with their money in later years. I would hazard to guess that we will get some simple answers;

- feel secure that there will be money to pay bills

- try to keep as much from HMRC as possible

- avoid sleepless nights worrying about stock-markets

- pre-plan for catastrophies- dementia, inability to die etc

No two people are going to be alike and words like “security” and “pre-plan” will change from person to person and as people progress through their later years.

But even with all this diversity, we must still endeavour to keep things simple. We must create a single default solution for “everyman” – for the “pension plowman”.

Most of all we need to sit down and think, before we frighten people with new ideas and new responsibilites. To scare and frighten people into thinking that what they have needs change, that they need to be spending hours on their pension funds or thousands on advice is plain barmy. These are precisely the behaviours that give financial services salespeople a bad name.

We have the door open to “restoring confidence in pensions”, for heavens sake, let’s not slam it shut before people have had a chance to look around

This post first appeared in http://www.pensionplaypen.com

Henry, good comment. I think the community is still digesting the implications of all this and there are many wrinkles still emerging. I’ll be posting my own thoughts shortly. But at core, this signifies a shift in thinking, that the consumer has responsibility for their own outcomes, that is at odds with current regulator attitudes. It will be interesting to see how this is resolved. The consumer will now have to “man up”, learn, digest and think. Yes, there will be those who make mistakes, sometimes serious mistakes, but under this doctrine, it’s down to them.