This chart says something pretty interesting.

This chart says something pretty interesting.

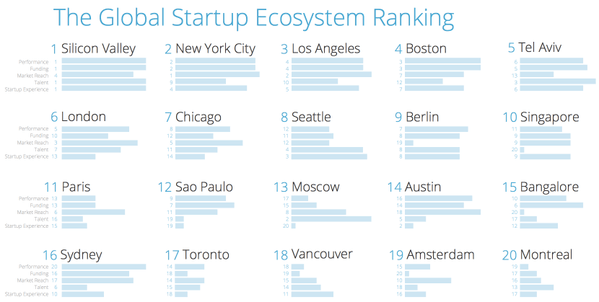

It tells us that London is the top place in Europe for Financial Technology, it tells us that in terms of performance and market reach, we’re doing great but that we lag in Funding and especially in the support we give start-ups.

As an underfunded FinTech start up operating in London, this resonates! But I’m not moaning, if it was easy then everyone would be doing it. The table demonstrates to me that the hot-housing of FinTech in the UK is coming from within the major financial institutions- organisations such as Barclays and Santander, who regularly pick up awards.

Part of the problem for UK start-ups is that they are considered disruptive precisely because of this incubator culture that is being imposed by the large financial institutions. One of the criticisms that is thrown at Pension PlayPen is that we have no “scalability”.

I take this to mean that we are not financed by a PWC or a Goldman Sachs or a Santander, we are outside rather than inside the mainstream financial community. I consider our independence from institutional money, our strength. And if David Cameron wants to progress the UK FinTech proposition, he needs to encourage more independents like Pension PlayPen.

The reason is clear from the table, without start-ups and without the support start-ups need, the FinTech revolution will lack the entrepreneurial zeal that characterises all major steps in economic progress. Most critically, it is only through entrepreneurial zeal that the state of present woes can be challenged. Nowhere is this more obvious than in pensions.

The recent outcry against the penalties that may be incurred from policyholders switching to exercise the pension freedoms is primarily a FinTech problem. There is no obligation on life companies to invest to migrate legacy pensions to modern systems that can pay people as they like and the life companies resist employing the brilliant technicians who could make this happen- for fear they might disrupt the revenue projections baked into long-term business plans.

So Cameron and Altmann and Osborne’s problem is that there is no-one able to challenge those who say it cannot be done, because the entrepreneurs are silenced.

Take Nick Ayton – formerly of Friendly Pensions (now of Gen Life) a serial entrepreneur sidelined by the major players for asking precisely the questions of the life companies and master trust providers that should be asked.

Take Blake Dempster– another entrepreneur whose vivid vision for pension freedoms is stifled by disdain for his enthusiasm.

Take Tim Jones, former CEO of NEST who is setting out to change the way we pay each other. He is doing so from the outside but who is listening and promoting? It seems to me that resistance to change increases in proportion to what those facing change have to lose. Nowhere is this more obvious than in financial services.

There are exceptions, and where those exceptions occur, they should be highlighted and applauded. I am seeing genuine interest in helping and promoting innovation in financial technology from Legal & General, NOW and Peoples Pensions. Their willingness to work with entrepreneurial start-ups like pensionsync, EAse, efileready and Pension Playpen is in marked contrast to the dog in the manger attitudes adopted by the Scottish Life companies and especially NEST.

My challenge to those life companies not working with FinTech entrepreneurs is this. What is your business plan for the next three years and how do you expect to deliver to the million and a half micro-employers through your historic distribution channels.

My challenge to NEST is to integrate with the Friends of Auto-Enrolment, adopt PAPDIS and start recognising what Cameron, Osborne and Altmann have recognised, that Britain’s FinTech industry keeps us ahead of the curve. Tata Consultancy and an in-house team can only take you so far. Anyone reading this, this beautiful Sunday morning, should be uplifted and not depressed.

For I see a huge change in the attitude of Government to this issue. The Financial Advice Market Review is evidence that Government now gets FinTech as a means of delivering low-cost financial advice to the millions who have never bought advice before. The attitude of the Pension Regulator to Pension PlayPen and otherFinTech start-ups and the openness of institutions such as the ICAEW, ICAS, ICB and many others to the new technology paradigm , tells me that things are going to change (and are changing).

That change will come from proper support to the FinTech start up sector and change in pensions will be accelerated by putting confidence in my company and those other FinTech start-ups delivering in our sector.

Andy Walker – PlayPen Technology Guru – points the finger!

Hi Henry,

Thank you for an interesting article. Much rings true. As a savings and pensions technology company we are constantly surprised at the interest from the rest of Europe – and maybe this article explains why. What is the origin of the graphic?