Jeff Prestridge is on the final lap of a marathon career.

If you are a subscriber to Daily Mail’s Money Mail but though I write article for them , I have no access so this tight-typed article is the nearest I can get to a readable version of Jeff’s denouement!

Indeed I can get you no nearer the wisdom of Stuart kirk in the FT, but it is the same as Jeff’s. It seems tough when you’re faced with a crisis , but in hindsight – only two crisis’ hurt Stuart.

Words of a pastor that echo Derek’s ; fit for a Sunday morning after Easter

The following beautiful comments from Derek Scott are worth reading several times

The Scots would say “nae wise” of someone acting without sense — which fits much of today’s investment orthodoxy.

PensionsOldie, meanwhile, shows what real wisdom looks like: steady, high single-digit returns earned with patience, not adrenaline.

Prudent trustees once managed investments sensibly for income and stability.

Then came the accountants, actuaries, bankers, and regulators — my own former profession among them — who turned “prudence” into paperwork.

“De-risking” became a gospel of caution, assuming unmet income requirements could be replaced later with new capital.

A strange kind of prudence that values process over outcome.

True prudence — foresight and good judgement — has been lost in a shuffle between compliance documentation and fanciful modelling.

We call it safety, but it’s often cowardice.

Modern Portfolio Theory sealed the deal. Clever maths, yes — but its advocates turned “risk” into statistics and forgot about context, behaviour, and purpose.

Diversification and risk-adjusted returns became ritual, not reason.

We’ve risk-adjusted ourselves into mediocrity.

Real prudence demands courage: the willingness to act wisely, not hide behind models and red tape. That’s what the old prudent trustees understood — and what most of us seem to have forgotten in this age of “risk management.”

Here are the equally sagacious thought of Pensions Oldie, another Scottish accountant I’ll be bound!

The problem throughout the UK investment culture, whether that be in pensions (occupational or personal), ISAs, or other long term savings vehicles is that risks (usually short term) are over-emphasised compared to the opportunities.

The most outrageous case is the demise of DB pensions where the legislative and regulatory background is entirely focused on failure and ignores the potential contribution that investment returns will make over the longer term. If you told employer sponsors in 2021 that they could expect to achieve an investment return of between 6% and 8% p.a. over 5, 10, or 15 years (which is what has consistently been achieved by an appropriately invested fund), they would say “but the Pensions Regulator expects us to lose 2% p.a. over the duration of the liabilities and is forcing us to divert resources from our productive enterprises”.

I am off to invest my £20K annual ISA allowance, where my self select stocks and shares ISA has achieved a net investment return of 7.9% p.a. over the past 29 years and my other ISA fund using an asset manager has achieved 7.6% p.a. over 24 years. My passively invested in equities SIPP has achieved a net investment return of 9.47% over 10 years, partly due to minimal management charges (currently 0.23% p.a.). All measures are to the 31st March 2026 and reflect the headline making market conditions at that date.

I am fortunate because of my background and experience I am able to perform these calculations for myself and I am able to devote some time each day to the management of my investments (which is almost entirely on a buy and maintain basis). I do pity the novice investor faced with the barrage of risk disclosures blinding them to the opportunities of long term investing.

Both comments are in reaction to a blog I posted on “de-risking and prudence“. There are other fine comments there besides.

There is something wrong about this. Insurers should not gloat that they will be investing what is currently our pension fund money.

The insurance companies expect £550bn of our money to insure and reinsure promises already secured in pension schemes. This time our security will be from insurance and reinsurance contracts. The benefit shareholders of insurance companies receive is not going to pensioners or to sponsors who have overpaid into defined benefit pensions.

This advertisement is for a happy group of insurers and their asset managers, but it is not for ordinary people or even the sponsors and trustees of their pension schemes. They are on the outside of a buy-out that will I fear, leave many of us short-changed.

I am not the only one who finds this attitude of insurers to taking over pension funds wrong. Here is a man who has worked in pensions for the best part of 60 years and should know what is happening to our pension system.

They may be paying out the same amount – but not to the same people. Do you want your pension fund paid to you and your sponsoring employer or the shareholders of insurance companies?

The closure of these schemes was not necessary. The demands on sponsors unnecessary and the surpluses these schemes hold will simply be transferred to insurers and reinsurers to satisfy an end game devised by the insurers, the regulators and the consultants.

Necessarily, the transfer of £550 bn of money put aside by pensioners, to pay pensions is a triumph for the insurance industry, which they are sharing with asset managers. But it shuts out the members and sponsors of the pension schemes.

We have seen in recent cases, pension funds opting to carry on investing for their members and to return money to sponsors. We have seen a pension fund swapping sponsor to improve the scheme’s covenant and ensure money goes to members and sponsors.

We have yet to have the secondary legislation to see pension superfunds take hold but when we do, we can reasonably expect an alternative for employers wishing to walk away from the cost of sponsoring pensions. Here cost savings will be created by consolidation without handing the profits to insurers.

I hope that in the next decade we will , as Andrew Young suggests, see much of the money that would have gone to insurers go to pensioners as pensions and sponsors relieved of obligations as they would with buy-out by swapping sponsors and transferring obligations to pension superfunds.

The money in our pensions is not the insurer’s by right.

Photo of Richard Tice by Laurie Noble, licensed under CC BY 3.0

Richard Tice is someone who attracts those who believe Reform can make Britain great again through being tough on those who cheat the system.

He has served as Deputy Leader of Reform UK since 2024 and as the Reform UK Business, Trade and Energy spokesperson since February 2026.

This is Dan Neidle’s account of Richard Tice’s company’s behaviour. I was asked to meet Richard Tice, we never met.

Dan Neidle, the author of the article below and founder of Tax Policy Associates, is a member of the Labour Party. Tax Policy Associates has no political affiliation. Its previous reports suggesting politicians failed to pay the tax due investigated Angela Rayner, Keir Starmer, Ian Lavery and Nadhim Zahawi.

Richard Tice’s property company failed to pay £120,000 in tax

The deputy leader of Reform UK, Richard Tice, owns a property company – Quidnet REIT Limited. From 2020 to 2022 it paid around £600,000 of dividends to Mr Tice and his offshore trust. Quidnet was required by law to withhold approximately £120,000 of tax from those dividends and pay it to HMRC. But we believe it’s clear from the company’s accounts and public filings that Quidnet did not pay this tax.

Mr Tice has refused to answer the question directly, instead saying that he paid income tax on the dividends. That’s not an answer: the company was legally required to pay tax; the law doesn’t permit REITs to opt to defer their tax obligations.

The issue was first identified by Gabriel Pogrund of The Sunday Times – his report is here. Since the paper went to press we have conducted further analysis of the two last dividends, and so the figures in this report are higher than those reported in The Sunday Times.

Quidnet REIT

Quidnet REIT Limited is a property company controlled by Richard Tice, the deputy leader of Reform UK.

From 10 August 2018 to 9 August 2021. Quidnet was a REIT: an investment fund that invests in real estate. A company wishing to become a REIT has to apply to HMRC; the consequence is that the company then becomes exempt from corporation tax on its property rental business, but its investors are (broadly speaking) taxed as if they held the real estate directly. The logic is that a REIT is an investment fund, and the usual principle is that funds don’t pay tax; their investors do.

However, Mr Tice’s REIT was unusual: throughout its life, it was almost entirely owned by him and entities connected to him.

REITs are usually required to be widely held by different investors – they’re supposed to be genuine investment funds, not tax planning vehicles. The rules provide for a three year grace period in which REITs can become compliant but, as The Sunday Timespreviously reported, Quidnet REIT Ltd never attracted more than a small number of outside investors. Quidnet therefore ceased to be a REIT on 9 August 2021.

It’s unclear if real efforts were made to find outside investors – if they were not then we would regard this as aggressive tax avoidance which probably does not work technically.1 However this article is not about tax avoidance. It’s about what appears to be a simple failure by Richard Tice’s company to pay the tax that was due.

The tax Quidnet failed to pay

As a UK REIT, Quidnet was required to distribute at least 90% of its tax-exempt property rental profits to shareholders as “Property Income Distributions” (PIDs). This is essentially the quid pro quo for the REIT tax exemption – you have to pay profits to your shareholders, and the expectation is that (unless they’re exempt) they’ll be taxed on those profits.

But HMRC isn’t content to just wait for the shareholders to pay tax. That could be over a year from the date the profits were made. There’s also a risk that the investors would simply fail to pay tax on the dividends they receive. So, just as an employer is required to withhold PAYE tax when paying wages to its employees, a REIT is required to withhold basic rate income tax (20%) from its dividends, and pay it to HMRC. Dividends paid to UK pension funds (such as SIPPs) and UK companies are exempt from this withholding requirement. The Assura plc REIT has published a helpful summary of the rules.

Quidnet paid around £600,000 in REIT dividends to Mr Tice and his offshore trust2 – the RJS Tice Family Settlement.

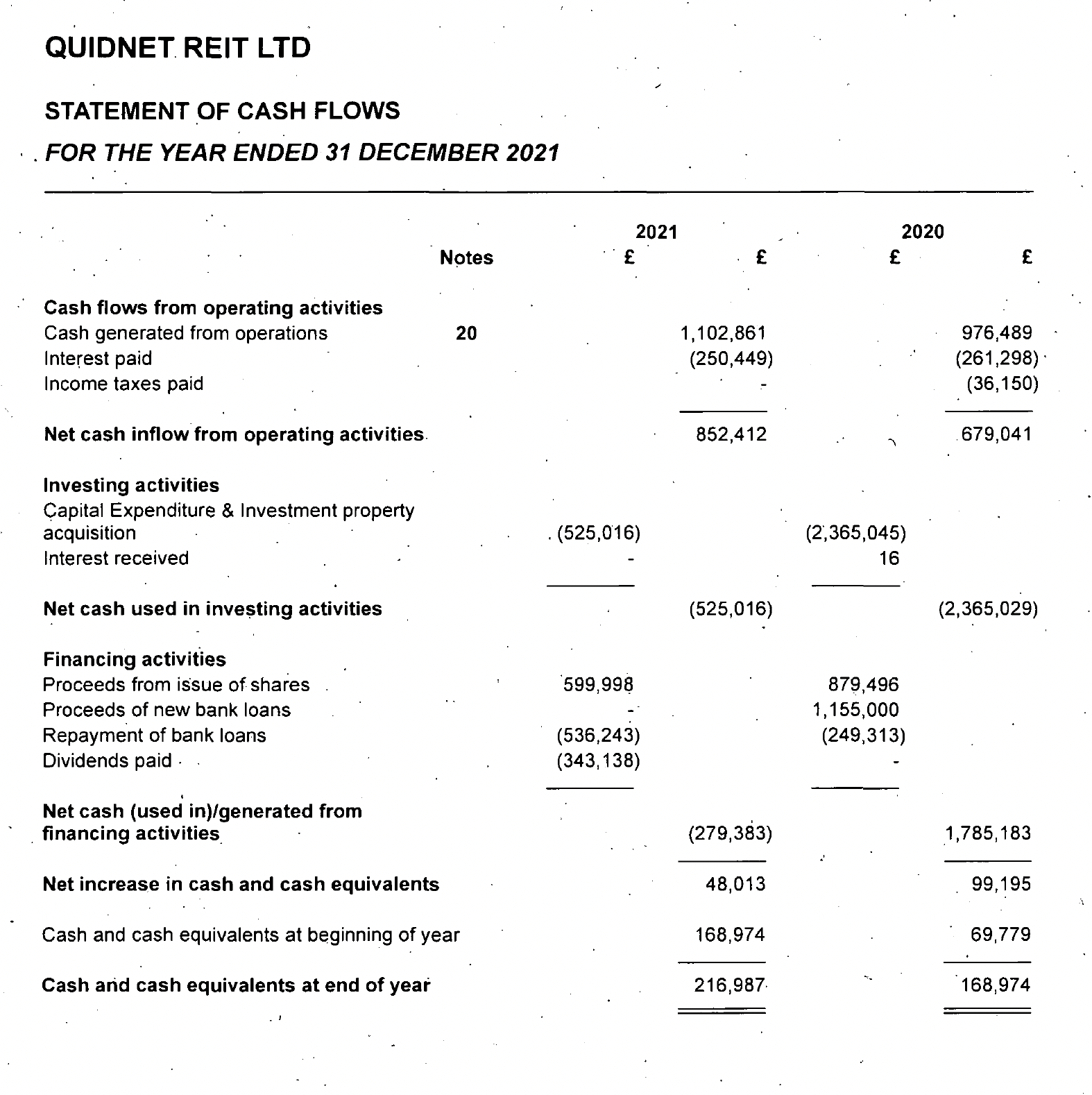

Quidnet should have withheld around £120,000 of income tax from these dividends, and paid it to HMRC. There is, however, no sign of this in the company’s cash flow statement – the tax should have been there (either under tax or dividends), and it isn’t:3

The “methodology” section below goes through a detailed analysis of how, even aside from the accounting treatment, we can be confident that the company failed to withhold around £120,000 of tax.

The obligation for a REIT to withhold tax is well understood and (absent very unusual circumstances) we expect HMRC would say that the failure to withhold tax was careless. On that basis, HMRC would have six years to make an assessment and collect the tax plus interest and penalties of up to 30%, but probably 15% in practice.4

Richard Tice’s response

We wrote to Mr Tice seeking comment for this story. We received a response which failed to engage with the substance of the matter. Here’s our initial request, the response from Mr Tice’s lawyer, and our reply.

Tice, the Boston & Skegness MP, implied the failure amounted to a “technicality” and appeared to suggest it did not matter as he ultimately paid income tax on the dividends he received. He said: “I have paid all tax at the highest rate on all dividends received. HMRC has been paid in full.”

And then, shortly after we published this report, on X:

Mr Tice’s certainty that the correct overall amount of tax was paid is inconsistent with his solicitor’s complaint that Mr Tice hasn’t had time to refer the point to his accountants. And Mr Tice also doesn’t mention the Jersey trust – it’s unclear if the trust paid UK tax at all.

But the more important point is that, regardless of what tax was paid by Mr Tice and his trust, REITs and their investors have no choice how and when tax is paid. The law requires that a REIT withhold tax from its dividends immediately. It would be much more convenient for its shareholders if they could skip the withholding and wait to pay all the tax until they file their own tax return, up to 21 months later. The law, however, does not permit this. The law is also straightforward and, in our experience, well understood in the REIT industry.

It’s important to add that this was not tax evasion – a criminal offence – because there’s no reason to believe Quidnet’s directors or employees acted dishonestly – in our view that would be far-fetched. It was also not tax avoidance – an attempt to exploit a loophole. It was much more simple than that: Quidnet mistakenly failed to pay the tax required by law, and is now required to pay it.

Methodology

Many of the dividends in question were either paid by issuing new shares, or satisfied by issuing new shares. New shares are tracked in company records, and this gives us a second independent confirmation that there was a failure to withhold tax as required by law (in addition to the cashflow statement in the accounts).

The shareholdings

At the start of the period in question (July 2019), Quidnet had seven shareholders. Dividends paid to UK companies and pension funds are exempt from REIT withholding, leaving two shareholders subject to withholding tax on Quidnet’s dividends:

Richard Tice personally — 824,100 shares (15.36% of the total)

His Jersey trust — 1,033,598 shares (19.26% of the total)

Together they held 34.62% of the company’s 5,366,193 ordinary shares.5

The dividends

There were three types of dividends paid by Quidnet, and the 20% withholding tax rule applies to them all in a slightly different way:

Simple cash dividends

Tax is simply deducted at 20%. So, for example, if a dividend of £100 is declared to an individual REIT shareholder, then £20 should be withheld by the REIT and remitted to HMRC, and £80 paid to the shareholder:

Scrip dividends

Instead of paying a dividend in cash, a company can pay a “scrip” dividend by issuing new shares to the shareholders.

A scrip dividend is subject to withholding in the same way as a cash dividend. So, for example, if a dividend of £100 is declared to an individual shareholder, and satisfied by issuing 100 shares worth £1 each, then the REIT should withhold 20 shares, issue 80 shares to the shareholder and pay £20 to HMRC.7

For an example of how this is usually done in practice, see the bottom of page 3 of this document from LondonMetric Property Plc, and the worked example on the following page.

Dividend reinvestment plan

A company can declare a normal cash dividend but then satisfy it by issuing shares to investors, sometimes at the investors’ option (in which case it is often called a “dividend reinvestment plan” or DRIP). The end result looks the same as a scrip dividend, but legally it’s just a cash dividend followed by a share subscription. So, for example:

There’s an example here of how this is usually done – “the net dividend after tax is effectively reinvested by acquiring additional shares in the Company” (our emphasis).

The following paragraphs look in detail at the dividends paid out of REIT profits, and therefore subject to the withholding rules.

Dividend 1: FY2019 final (March 2020)

On 16 March 2020, the board declared a dividend of £684,055 for the year ended 31 December 2019. On the same day, it resolved to issue 423,040 new shares at £1.617 per share.8

The value of the shares issued — 423,040 × £1.617 = £684,055.68 – matches the gross dividend.9 This wasn’t a scrip dividend, but a cash dividend – satisfied in shares, with zero cash paid out.

If Quidnet had properly withheld 20% tax, it should have issued approximately 29,300 fewer shares and remitted around £47,364 to HMRC.10 Instead, shares were issued for the full gross value of the dividend – that provides independent confirmation (in addition to the accounts) that there was a failure to pay the correct tax.11

We can conclude that no tax was withheld from the £237,000 of dividends paid to Mr Tice and his trust, and £47,400 of tax was underpaid.

Dividend 2: H1 2020 interim (September 2020)

On 25 August 2020, Quidnet declared an interim dividend of 5p per ordinary share, to be paid on 21 September 2020 “by issuing shares at the new NAV per share of 155.1 pence”.

The announcement stated that “Shareholders are to receive 1 share for every 31.02 ordinary shares held”. A TISE announcement on 18 September 2020 confirmed that 186,627 shares settled the scrip dividend.12

This was a true scrip dividend. The conversion ratio is uniform for all shareholders — every holder gets 1 new share per 31.02 held, regardless of their tax status. If 20% had been withheld from non-exempt shareholders, the effective dividend would be 4p (not 5p) per share, and at an NAV of 155.1p this gives a ratio of 4/155.1 = one share for every 38.78 shares held.

Richard Tice received 28,661 shares worth about £44k. The trust received 35,947 shares worth about £56k. Both should have been subject to 20% withholding tax, but there’s no sign of that in the figures.13

We conclude that no tax was withheld from the c£100,000 of scrip dividends paid to Mr Tice and his trust, and around £20,000 of tax was underpaid.

Dividend 3: FY2020 final (April 2021)

On 17 March 2021, Quidnet declared a final dividend of 6p per ordinary share for the year ended 31 December 2020, with shareholders having the option14 to apply the dividend to subscribe for ordinary shares.

By cross-referencing the share register15, we can determine that Richard Tice personally took this dividend in cash, receiving £55,000 cash, and the trust took the dividend in shares, receiving 40,145 shares worth £64,000.1617

Once again, the full gross dividend was distributed with no apparent deduction for withholding tax.18 The trust received about £64,000 shares from which £13,000 should have been withheld and Mr Tice received about £55,000 cash from which £11,000 should have been withheld. And again, there’s no sign of any tax being withheld in the company’s cash flow statement for 2021.

We conclude that no tax was withheld from the c£119,000 of dividends paid to Mr Tice and his trust, and so about £24,000 of tax was underpaid.

Dividend 4: H1 FY 2021 (August 2021)

On 17 August 2021, Quidnet announced its interim results for the six months to 30 June 2021, and declared a further cash dividend of 5.5p per share, payable on 23 August 2021. Quidnet ceased to be a REIT on 9 August 2021. However this dividend was paid out of profits made when Quidnet was a REIT, and so we expect was fully subject to the REIT withholding tax rules.

To satisfy some of this dividend, filings show the company issued 132,212 new shares in late August at the newly reported net asset value of £1.613 per share.

Because we have the exact share counts from the July 2021 confirmation statement, we can calculate precisely what was owed and how it was paid. The trust held 1,191,173 shares, entitling it to a gross dividend of £65,515 (1,191,173 × 5.5p). If we divide the trust’s £65,515 gross dividend by the £1.613 share price, it equates to an allocation of 40,611 shares. Confirmation statements show the trust’s shareholding increasing by precisely that amount.19 This confirms the trust elected to take its entire 5.5p dividend as scrip, and that the shares were issued for the full gross amount, with no shares withheld for tax.

At that time, Richard Tice held 917,728 shares, entitling him to a gross dividend of £50,475 (917,728 × 5.5p). His shareholding remained unchanged after this; confirming he took his £50,475 dividend entirely in cash. Just as with the previous dividends, there is no evidence the company operated the required 20% tax deduction on this cash payment.

We conclude that no tax was withheld from the c£116,000 of dividends paid to Mr Tice and his trust, and so about £23,000 of tax was underpaid.

Dividend 5: FY 2021 final (10 May 2022)

On 10 May 2022, Quidnet announced a final cash dividend of 5.3p per ordinary share. This covered the period from 1 July 2021 to 31 December 2021. Quidnet was only a REIT for a small amount of that time. In principle the rules require withholding to be applied to such amount of that dividend as attributable to profits made during the REIT period. We have no way to determine that, so will instead estimate the amount using a simple pro-rata calculation, i.e on the basis that Quidnet was only a REIT for 40/184ths of H2 2021.

On that basis, we estimate that the REIT rules applied to approximately £10,00020 of dividends paid to Mr Tice (received in cash) and £14,00021 of dividends paid to the trust. That’s a total of £24,000 – but there’s no sign of any income tax deducted in the accounts.22 It follows that £4,800 was underpaid.

Dan Neidle, the founder of Tax Policy Associates, is a member of the Labour Party. Tax Policy Associates has no political affiliation. Our previous reports suggesting politicians failed to pay the tax due investigated Angela Rayner, Keir Starmer, Ian Lavery and Nadhim Zahawi.

Many thanks to Gabriel Pogrund of the Sunday Times, who discovered this story, and to K and M for the REIT and accounting analysis that underpins this report.

Footnotes

Either because of the specific anti-avoidance rule in the REIT legislation or because of the general anti-abuse rule (GAAR). This announcement suggests that there may have been an attempt to technically meet the requirements, notwithstanding that the shareholders were all connected to Mr Tice, rather than an actual attempt to find genuine outside investors ↩︎

The cash flow statement does show £36,150 of “Income taxes paid” but that’s too small to be the tax that should have been withheld; we expect it was another item (the most common cause of REITs having a tax liability is failure to distribute 90% of their property rental profits, but there are several other ways tax can arise). Withholding tax could also be included in the “dividends paid” line, but the figures here are the same as the cash dividends (and so zero in 2020); there is no sign here either of any tax. ↩︎

If that results in double taxation, then it is possible (but far from certain) that HMRC would in practice not collect the tax (as that would result in economic double taxation); we expect that HMRC would still apply penalties (probably 15% given this would likely be a “prompted” disclosure). ↩︎

The remaining shareholders were RJS Tice Family SIPP (36.04%), and NJG Tribe SIPP (1.75%) and three UK companies: Tisun One Ltd (9.21%), Tisun Two Ltd (9.19%), Tisun Three Ltd (9.19%). ↩︎

The shareholder then gets a credit for the tax withheld, so overall the right amount of tax is paid, and the withholding tax is really just an advance payment. ↩︎

The authority for this is s973(3A) ITA 2007, which says applies the usual rule that the cash value of a scrip dividend is treated as its “amount” for tax purposes. So when we apply the withholding rules, instead of withholding some shares and giving them to HMRC, the requirement is to hold a cash amount. That is by contradistinction with the “funding bond” rules, which (in a different context to a REIT) can require securities to be withheld and handed over to HMRC. ↩︎

These and other corporate announcements can be found on the Channel Islands stock exchange (The International Stock Exchange) website. ↩︎

If 20% had been withheld from the non-exempt shareholders (Tice 15.36% + Settlement 19.26% = 34.62% of the total), only ~393,700 shares should have been issued instead of 423,040. The difference of ~29,300 shares at £1.617 = ~£47,400. ↩︎

We can go further by reconciling share figures from the confirmation statements filed with Companies House, i.e. starting with share ownership figures in the July 2019 confirmation statement and adding in the shares that would have been received if tax had not been withheld; that equals the holdings we see in later confirmation statements. This confirms that Mr Tice and the trust received the gross number of shares – more on that below in the footnote to the second dividend. ↩︎

A further 567,051 shares were issued as new equity to fund a property acquisition. ↩︎

Perhaps the announcement was just sloppily worded and in fact tax was withheld and Mr Tice and the trust received 80% of the stated numbers? We can eliminate that possibility by looking at the change in Mr Tice’s shareholding from the July 2019 confirmation (when he held 824,100 shares) to the July 2021 confirmation (when he held 917,728 shares). That’s a difference of 93,628: exactly equal to the 64,967 shares he received for dividend 1 plus the 28,661 shares he received for dividend 2. So it’s clear that the shares were issued without any withholding. ↩︎

The announcement says that the option to subscribe was offered to shareholders who were directors or employees of the company; we believe this was loose wording and that Mr Tice’s trust also had this opportunity. Our reconciliation of share subscriptions shows that the trust did in fact subscribe for the shares. ↩︎

Because his July 2021 shareholding of 917,728 is exactly explained by his original 824,100 shares plus the two 2020 pro-rata scrip allotments (64,967 + 28,661 = 917,728). He therefore received no new shares from this dividend. ↩︎

The RJS Tice Family Settlement’s holding increased by approximately 40,145 shares between the end of the H1 2020 interim dividend and the July 2021 confirmation statement — precisely matching scrip at the £1.602 issue price; i.e. no shares/tax were withheld. ↩︎

There is a small amount “missing” here. The trust had compounded its holdings to roughly 1,151,028 shares by this point, so a 6p per share dividend means it was actually entitled to a gross dividend of around £69,060. This implies the trust either took the remaining ~£4,760 in cash or there is a source of error we are missing. That’s not clear – so we will conservatively assume there was no cash dividend. ↩︎

The scrip shares (140,304 × £1.602 = £224,767) plus the cash (£168,246) total £393,013 — almost the same as the gross dividend of 6p × 6,542,911 shares = £392,575. ↩︎

It looks like Quidnet failed to file correct confirmation statements for 2022 and 2023, as they show no changes in shareholdings, but the July 2024 confirmation statement shows the trust holding 1,231,784 shares – i.e. a difference of 40,611 shares. ↩︎

Mr Tice’s holdings at this point were 917,728 shares. So 917,728 x 5.3p x 40/184 = £10,574. ↩︎

The trust’s holding at this point was 1,231,784 shares. So 1,231,784 x 5.3p x 40/184 = £14,192. ↩︎

The cashflow statement on page 14 of the 2022 accounts shows £69,095 of tax paid in 2022. That is almost exactly the same as the £69,098 of corporation tax shown on page 19. We conclude that no tax was deducted from dividends in 2022. ↩︎

When I first went to Aintree six years ago, I wrote a blog called “the day the world turned orange”. I had been caught out by the wonderful world of scouse and I’ve been going back to Aintree every spring since.

I hadn’t had reason to write another blog since then, till yesterday, when I returned from Liverpool at around midnight and promptly watched the whole afternoon again , in the early hours of the morning. To save you that trouble, here’s the Racing Post’s 60 second review of the day.

If you are a fan of racing, and can bear the pain of a horse dying, then here is the Grand National in its 10 minute glorious denouement!

For Stella and me, the weekend will get better – Stella is a netball fan!

I am watching (as I blog) , the Chinese Grand Prix . Last night our train returned with Bournemouth fans going home after a 3-0 defeat to Liverpool. Our train passed Wembley, the scene of Man City’s 3-1 triumph over Tottenham.

Britain is a wonderful place to be a sports fan, but I can honestly say that there in nothing- nothing – that can compare with Aintree in the Sunshine and the smile of Davy Russell as he returns to the winning enclosure!

The Grand National of 2012 will be remembered for good and bad. Detractors will point to the shocking deaths of According to Pete and Synchronised, the shambles of Sychonised’s final minutes played out in the most desperate fashion. Others will remember it for the closest finish ever, the collective delight of the Hales family, Paul Nicholls, (Neptune Collonges‘ trainer) and Darryl Jacob, the jockey.

But for our little party , April 14th will be remembered as the day the world turned orange. Never has so much flesh been bared , in such weather without so much a hint of a moan. Just about everything off to the female population of Liverpool for turning out in numbers and reinventing the parade ring as an impromptu catwalk of block heels, microskirts and fake tan.

I cannot say Aintree is a handsome place, you enter the course from a retail park , the skyline is underwhelming, the flatlands of Merseyside spiked by the odd industrial chimney. There is no natural order in the layout of the stands and rings and it stands no comparison to Cheltenham as a venue.

Yet there was a vibrancy about yesterday that left us breathless. We’d had the bright idea of taking the Orient Express from London which provided the starkest contrast between the aspirations of the few and the reality of the many. Give me the reality of “the many” , a pint of lager and a blue Wicked. Oh and give me the Liverpool Everton semi-final that seemed considerably more interesting than the the processional performances of Sprinter Sacre and Simonsig (a grade one derserves more than four horses and a 1-7 favourite).

With all the shenanigans surrounding Synchronised delaying the final races, many of our party had to slope off before the sixth race to catch our bus back to the train. For those who stayed, our pension background came to the financial rescue. Everyone knows you should lifestyle at the end of the journey. Lifestyle under David Bass duly cruised home at 46 to 1 on the Tote ; long were the celebrations among those of us on the pre-retirement glide path.

So a big thumbs up to Aintree, the wild west of racecourses blessed by the wonderful Coleen Rooney and inspired by the tanning and nail bars of the North West.

I do not even want to understand what drives the orange lovelies to their goose-pimpling exploits but they’re the best thing the Grand National has to offer- and that is saying a hell of a lot!

I take my hat off to them, they took a lot more off for me.

I have been up a few times for the day and am amazed at the bravery of jockeys and horses in this amazing spectacle and race!

Guy, who used to be our pensions minister was a jockey himself and has the photos to prove it (once having been told to keep out of his way by Tony McCabe.

Here is Guy Opperman aboard and racing

I am pleased to see he has lost weight and look forward to him making an amateur racing before too long!

Here he is aboard Lowlander on the way to victory ( I may be a little fanciful but there’s a comment box Guy!)

It is really pleasing to see Labour MPs getting pension people involved in the business of running this company.

I would not have known much about Sarah Edwards; I would not have known much about this group

Pensions and Growth APPG

First Registered: 18/06/2025 • Last updated on: 23/02/2026

To bring together parliamentarians, stakeholders (including employers and unions) and the pensions industry to facilitate discussions on adequate, sustainable retirement income across state, occupational and private pensions. It will also focus on how pension funds may be able to support economic growth and regional economic regeneration through domestic investment.

APPGs and MPs can make a difference!

There is good reason that this blog knows about Sarah Edwards. Not only is she leading a group doing good things with local authority pension schemes (LGPS) but this group is promoting pensions can support economic growth, a theme of this blog and of the people who read it.

I am pleased that Darren and Nico have answered the questions that have been put to them but slightly disappointed that more challenging questions have not been asked. Here are the questioners who have been answered in one go though released over two weekends.

You can follow the second salvos from the usual list which explains just how lengthy a process it is! 12 people asked questions and Darren and Nico took two hours and thirty seven minutes to answer them. I count myself as resilient to listening 157 minutes to get an answer to my question!

It is of course important that debate happens and there is no clearer exposition of the views of a part of the pensions industry than this podcast. I find it a good way of making journeys less tedious , doing the shopping to and watching football games (without the commentary).

Richard Smith has posted some commentary on “post 155” which I enjoyed.

There is one thing that a podcast has going for it , that cannot be had from written material and that is guaranteed authenticity. What we get over the two and a half hours is unedited and unbelievably fluent. There is no sense of the AI which spoils most of what goes onto social media at the moment.

I have not let an AI chatbot onto this blog, though I do get a spellcheck that does a little correcting! I suspect that what people want when listening or reading others is “authenticity”.

I am amazed when all kinds of people turn up at events to deliver keynotes and see this as an opportunity to read what they and a group of cronies have written in advance. We most certainly don’t get that from the two lads and nor do we from Richard Smith.

Perhaps I can plug what he has coming up, by way of a rival podcast to VFM. I am sure it will be authentic and perhaps a little more concise than what I review from Nico and Darren!

Guy Opperman has been an intermediary between the civil service and those getting their knickers in a twist about the Pension Schemes Bill. Thanks Guy.

It’s a valuable service that brings order and sense to the ping pong between the House of Lords amendments and the final version of the Bill that becomes an Act some time in May.

The Lords have been thrown some meat to chew on and this will assuage the feeling of being ignored without changing the large number of changes to pensions that will be enacted. For the Lords , read the pensions industry and in particular the ABI and Pensions UK lobby.

Read Guy Opperman again

Big Commons majorities mean the Labour government can do what it likes. On the issue of mandation expect a minor government amendment to appease the Lords a bit. I would be surprised if anything else the Lords has passed is agreed

In a recent “VFM podcast”, Nico Aspinall said the Government should “kill VFM” which I agree with. VFM started out as a simple way of getting people to engage with pension saving (as happens in Australia). It has been through a number of consultations and become a way for the FCA and TPR to exert control on the consolidation of DC workplace pensions.

Torsten Bell has better things to do than worry about VFM which is obsolete in its intent. The world he wants is one where workplace pensions do the job SERPS were supposed to do for millions of people who otherwise would need a state pension the Treasury cannot afford. Auto-enrolment gave him the mechanism to deliver a pension system and we will remember the Pension Schemes “Act” as a means to consolidate DB and DC pensions and to give space for a more sensible way forward for a return to genuine pension saving.

I have enjoyed the intermediation of Guy Opperman in recent weeks. The Pensions UK and ABI lobby had got as loud as it could through capturing parts of the Lords to demand some say in politics but it has fallen short of anything effective as we have a strong government (at least in this area). I haven’t heard anybody say it , so I will. I thought the Pensions Bill was largely right when it arrived. While it has short changed some who deserved better (Pre 97 pensioners) and will need a lot of secondary legislation on DC decumulation, DB superfunds and the mess of DC (VFM, small pots and GPPs), the Pension Schemes Bill is one of the big wins of this Government and takes us back to pensions.

I am not very polite to politicians because they have thick skins and have fought their fights in a tougher debating chamber than this blog! Steve Webb does amazing things for the consumer in the media and on TV with Martin Lewis. Guy is looking like he’ll shape up as an intermediary with the pension and insurance lobby. They are the two former pension ministers we’ve had since the first Pension Commission that will be remembered. We have another in charge now. I doubt Torsten Bell will stay a pensions minister for long but he has lasted longer than many thought he would and he will see his Bill enacted.

In the meantime, there are important matters for us worker ants to get on with. While the retail market plays in the sandpit with the FCA, the institutional action is with the TPR. The Treasury and DWP are as one with a pensions minister who is liked in both. We should take advantage of a benign time for pensions and make a difference.

Thanks to Guy Opperman for bringing some sense through intermediation!

The Grand National of 2012 will be remembered for good and bad

The Grand National of 2012 will be remembered for good and bad It’s something to remember back to distant off Grand Nationals but another to have a photo of your Dad riding in it!

It’s something to remember back to distant off Grand Nationals but another to have a photo of your Dad riding in it!

{kind=link}