I’m not in the business of picking fights with the Pension Regulator- it isn’t a clever strategy at the best of times, and now is not the best of times for pensions.

I’m not in the business of picking fights with the Pension Regulator- it isn’t a clever strategy at the best of times, and now is not the best of times for pensions.

A couple of weeks ago I blogged about pension liberation fraud and had a go at the Regulator for “threatening trustees with a big stick (the blog was republished in Professional Pension on July 4th).

Thankfully, what I and the audience at NAPF South Eastern Group’s Summer Seminar on 19th June is not the Regulator’s policy (it was simply a couple of lawyers pointing out that in some situations, trustees may be required to still pay the pension even though the transfer value needed to pay the pension had been transferred out).

THANK GOODNESS FOR THAT

Nevertheless, it’s a useful learning point for tPR, that people do actually listen to what is said at humble little NAPF meetings and when a statement is made by an officer of the Regulator, it is generally taken as the Regulator’s view.

Sorry Regulator but that “never” is wrong and until your article, what I and others heard at the seminar was our understanding of your position!

So I stand by my blog but am pleased that we now have clarification on the issue!

On a couple of minor points

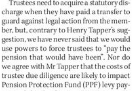

The Regulatorand disagrees with me that the cost of trustee due diligence could impact the PPF (see clip above).

My reasoning is this

- Unless the costs of the extra due-diligence to prevent liberation are born by a third-party, it is clear that they will be born by the trustee of the sponsoring employer!

- The costs add to the funding burden and where they cannot be borne – will transfer to the PPF

However, I am prepared to accept that the quantum of the impact will be relatively small and the real issue is the wider burden on trustees and employers.

On a seperate point, I stand corrected; the HMRC do not (as the Regulator points out) charge fees for Registering an occupational scheme – perhaps they should- the fees could be used to pay for proper due diligence to stop the setting up of fake schemes,

On the wider issue of trustee and employer duties;

There is a predisposition among Regulators to create rules; whether these rules create duties on trustees ( as looked to be the case with pension liberation) or on employers (as with auto-enrolment), these duties cost.

It is fair for trustees and employers to push back when the cost falls unreasonably upon them. In the case of pension liberation fraud, the tone of the Regulator’s article that can be read in full here http://viewer.zmags.com/publication/f86597af#/f86597af/12 , is positive.

I am pleased that my article has created this positive response not just because it reduces the burden on trustees (or at least corrects the Regulator’s position) but also because it demonstrates we have a Regulator that listens and is mindful not just of its rules, but the burden those rules can create.

The Regulator, as I have pointed out in previous blogs, is one of the most engaged governmental agencies I have come across (NEST gives it a good run for its money); it gets key messages out by twitter, it runs a brilliant linked in site (which accommodates my often challenging views) and it has an excellent array of speakers who give interest to the majority of pension events I attend.

Without this open dialogue, we would not have the necessary tension between those who create rules and those who have to meet their costs.

THANK GOODNESS WE HAVE THIS OPEN GOVERNMENT

This blog first appeared at https://www.pensionplaypen.com/top-thinking/show/91/thank-goodness-for-that.html