Auto-enrolment is like Flanders in 1914. Those wishing to see universal adoption of workplace pensions within Britain’s employment structure are digging in for an onslaught that has barely begun.

Our Ypres’ and Passchendaeles’ are yet to come. We are still in the phoney war.

The latest update from the Pension Regulator on the progress of the grand plan to enrol 11m of us into workplace pensions makes interesting reading both for what it tells us, and what it cannot tell us.

What it cannot tell us, but we need to know, is how many of the April 2014 stagers have now declared their compliance. Unofficially, we believe the number is 93.6% but this has not been officially release. TPR are sanguine as they know a large proportion of the missing numbers relate to employers with multiple payrolls, who may have declared overall compliance and not itemised compliance per payroll. They also think that some employers enrolled employees into Local Government Schemes and have not been verified by providers.

It is to the Regulator’s great credit that it is facing the challenges of information candidly and sharing its numbers as best it can. There may be shortcomings in its intelligence but they are minor.

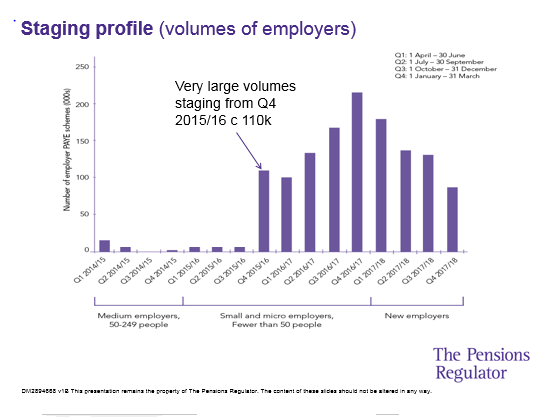

I am encouraged by the Regulator’s willingness to involve itself in the nitty-gritty of data transfer and help the market to get through the capacity crunch signalled by the alarming purple lines that dominate the staging horizon from the end of next year.

The Regulatory framework that governs workplace pensions is in a mess.

I am not happy with the Regulatory position on the pensions into which these 1.3m employers and 11m employees will be invested.

While we may remain compliant in terms of the administrative process, are the pensions into which we are investing improving?

The answer is that we do not know and in terms of Regulation, advisory capacity and employer empowerment, we seem to have hardly dug in at all.

For example, we do not know how many of the workplace pension schemes established to date are compliant against the minimum standards to be implemented in 2015.

More alarmingly, we don’t seem to have a regulatory framework in place that can give tell us what compliance (let alone best practice) looks like.

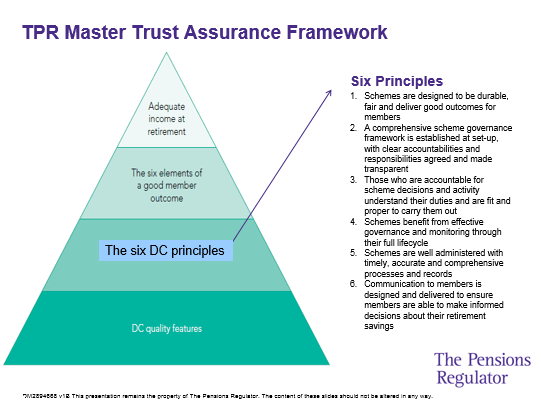

There is here a Regulator problem (more than just a regulatory problem). The voluntary framework that governs occupational master trusts (which are increasingly becoming the preponderant workplace pension) appears to be changing. Here is the vision as outlined by tPR earlier in the year

Here is the triangle as it was presented to Friends of Auto Enrolment on Thursday of last week.

Anyone trying to make sense of the Pension Regulator’s position with reference to these diagrams is in for some difficult hours of study! I have to put my hands up and admit defeat!

It’s not all bad..

On a positive note, it is good to see the idea of member outcomes being re-introduced at the top of the mix and its good to see the Pension Regulator reminding us what makes for good DC outcomes

But the rest is hapless

Behind these six elements are the woolly “principles” and behind them the 31 characteristics by which no adviser can educate nor any employer choose or review a scheme.

The ICAEW’s MAF document has much that is good about it, but it has not been designed to integrate with the workplace pension system going forward. It is not joined up to the DWP’s minimum standards (see below) and is inconsistent with the IGC proposals. It is a bit of a white elephant.

So where is all this leading?

It seems that voluntary compliance against this uber-complicated governance structure has become an end in itself. If I’m right, then the MAF will become no more than an upgraded version of PQM , at best a pensions equivalent of IS 9001,

This statement that appeared in the Regulator’ slide-deck suggests that two years and 4.4m people into auto-enrolment, we are only at base camp and that many of the mountaineers are climbing another mountain!

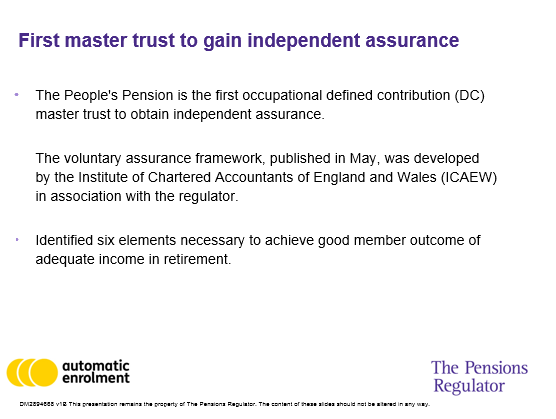

Good for Peoples Pension, but what does this say to the person in a Standard Life GPP?

This framework is too late, too complicated and totally fails to help those of us trying to advise, to do our job. How can we engage, educate and empower in such an environment

This a voluntary code looks set to become a marketing badge rather than the DNA by which a pension scheme is run.

By contrast, the FCA’s IGC proposals , which adopt “value for money” as the central theme, are understandable, meaningful and mandatory.

I cannot see how a voluntary code for master trusts and a compulsory code for contract based plans sits within an overall framework based on the Pensions Acts and the DWP’s Minimum Standards. In a world where every company has, by law to have a workplace pension plan, such widely differing governance systems for GPPs and master trusts only serves to confuse.

Is this MAF any practical help today or from April 2015 ?

From April 2015 we are being asked to apply the DWP’s minimum standards with reference to the master trust assurance framework and I cannot see how we can. Two out of the three leading master trusts have charging structures that are openly non-compliant with the 0.75% charge cap (NEST and NOW), others such as Friendly Pensions have followed suit.

The skill and knowledge needed to properly understand the costs that members meet from the Net Asset Value of their fund isn’t addressed by the ICAEW’s MAF, indeed any reading of the MAF and the IGC consultation would not suggest that their two authors had ever met.

In conclusion…!

All of which supports my earlier call for us to merge at least the DC divisions of these two Regulators.

So much for Regulation on workplace pensions -what about advice?

Coming back to the state of auto-enrolment, which of course is a different issue than the state of workplace pensions, the Pension Regulator’s enforcement team have some interesting research on who smaller employers are going to turn to for help on the staging of their workplace pensions.

The obvious conclusion is that accountants are increasingly going to hold the keys to auto-enrolment. The 74% of micros who claim accountants as their gurus are almost all going to be looking for a one stop shop for both auto-enrolment and payroll services. Infact the 78% figure is simply a reflection that most micros outsource payroll and HR to a business services manager who effectively runs the back office. So how ready are the accountants?

Most accountants are intending to offer the administrative services, but when we look more closely at the services offered or planned to be offered by accountants we discover that they are mechanistic and relate to the integration of HR and Payroll systems and compliance with regulations.

When it comes to the more pension related activities which touch on member outcomes 60% of accountants have no intention of getting involved.

All of which leads me to believe that the problems we will have with auto-enrolment are only being partially addressed.

With the regulation of workplace pensions being split between two regulators with radically different governance frameworks, with IFAs showing little appetite to involve themselves in the business of choosing or reviewing a pension, who will be “expert”?

{kind=link}

So who is going to advise?

The Regulator would like advice on pensions to only be given by those with skill and knowledge (though no definition of what makes for a skilled or knowledgeable person has been put forward).

We know that this advice – so long as it is confined to business to business conversations is unregulated

In theory anyone can advise, but without any clear direction from the Regulator , no reward from the workplace pension providers and no incentive on employers to take advice, it is no wonder that the advisory market for SMEs and Micros looks as shrivelled as a salted snail.

And are we any closer to empowering our employers?

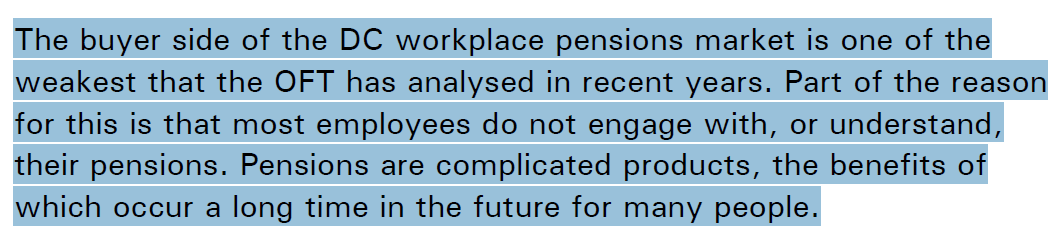

With such confusing information on what makes for a good pension and such vagueness as to who should be offering advice, it is likely that the OFT’s observation that

will continue to apply.

Until we can find a way to get Regulators to engage, advisers to educate and small employers empowered to make good decisions on behalf of their staff, the “buyer side of the DC workplace pensions market will remain auto-enrolment’s weakest link.

Despite these headwinds, we at http://www.pensionplaypen.com remain confidant that a way forward will be found, we just wish we didn’t make life so difficult for ourselves.

Mind you, by comparison to the strife of our forefathers, we can count ourselves very lucky. I am confidant that by 2018 , as we did by 1918, we will win this (not so bloody) war!

Our trenches are imaginary, our struggles mental and the stakes we play with a whole lot lower, so we remain playful!