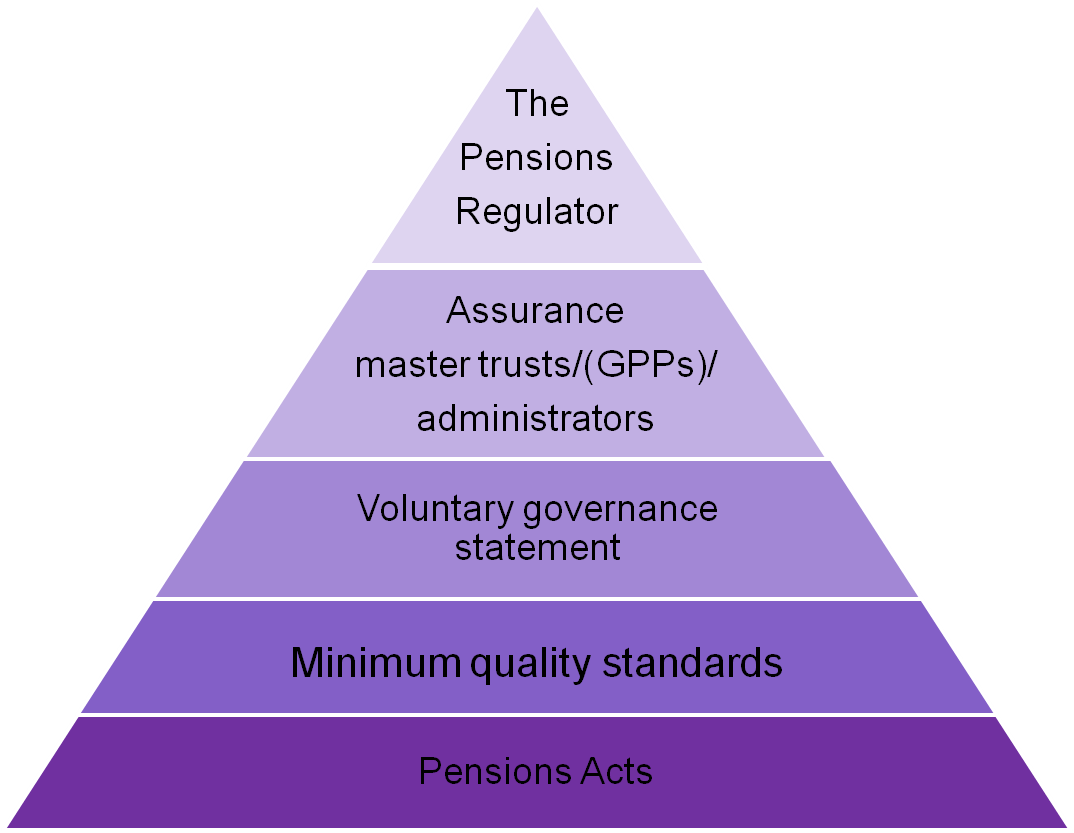

There is an important debate to be had on the regulation of master trusts.

That debate is about how we prevent poor standards invading what is currently a very well run part of workplace pensions. Until the past two weeks, I felt that we were moving towards an outcomes based system where the market would decide which trusts worked and which didn’t. And then the accountants came along and made what was simple, as clear as mud If you don’t know what I’m talking about, read the appendices of the ICAEWs draft “Assurance Reporting on Master Trusts”. I could ask you to read the whole document but even the accountants agree that the main body is no more than box-ticking. I have already written about this arguing that though it’s a joyless document, it served some purpose as showing us what a risk-based approach would look like

Feelings hardening against this risk-based approach

Since I wrote , I’ve had a couple of conversations that suggest that what I had thought might be a quiet regulatory cup-de-sac, is potentially a six lane motorway with traffic flowing in opposite directions Going one way is a body of opinion that says that the prescriptive risk-based approach in this draft Framework is regulation for regulation’s sake and that the law should lay down how master trustees (and others) should behave, and that the law should decide when such organisations are not acting in the interests of members. Going the other is the Pension Regualtor and Institute of Chartered Accountants’ approach. The direction of travel is well articulated by Andrew Riley in a comment on a thread within the Pension Play Pen Linked In group.

I was on the working party for governance standard by the ICAEW and tPR. I believe it does the good job of ‘putting flesh ‘ on the bones of the DC quality features for master trusts to check against. You are right though that it does not do everything as its scope was to focus is on demonstrating existing controls have been well-designed and with recent changes an update will be needed for 2015 and DWP etc. papers. Those should be added in in the judgement of the Reporting Accountant and I would expect to see that put in place. Where there has been no framework previously it provides one for master trusts, but it did not aim to cover other aspects like outcomes. Appendix 1 with table 1 and 2 is I agree the interesting bit to read for non-ICAEW folk. As an AAF 02/07 technical release we have to put in all the other pages (pity us!) to show how it meets international standards ISAE 3000 on assurance controls reporting. Let’s see what master trusts can do to show they are up to scratch.

Well I have to disagree, the 31 Quality Features (nee characteristics) were never any use to measure governance, nor the six principles. You have fleshed up the wrong bones!

Pension PlayPen’s worries with all this

Our fundamental worry is that over-prescriptive regulation could kill a golden goose. This would not be the first time that we lost a system of pensions that worked well in favour of nailing every risk. Those of us who remember occupational pensions in the pre “87” environment will remember (for all their faults) that companies wanted to offer them and people pretty were comfortable to be members as a condition of work. The introduction of compulsory this that and the other ending in the mark to market valuation of assets and liabilites turned what had been a pleasure into an obligation. The path the Master trust Assurance Framework could take us to the same place, albeit on a different route. From Andrew’s comments, it seems that the judgement of the Reporting Accountant will determine whether a master trust is acting in the interests of its members. Whoever this reporting accountant is will deliver a verdict on the master trust based on the metrics in Appendix I and II of the document. We can expect a v2.0 of this document as soon as we know what changes are in store for us in 2015 and presumably a v2.1 in 2016. So we are due an awful lot of paper which clearly Regulators like. In fact we all want less paper and less Regulation! I had never heard of ISAE 3000 till I read Andrew’s post and am sure I am no happier for knowing of its impact. Certainly we can do without most of the body of the document which is self-referential and probably only of interest to the working party (and ISAE 3000).

The Pension PlayPen alternative

As many people know, we have a built a means of assessing master trusts based on outcomes that simply concerns itself with 6 metrics “value for money”, “investments”, “at retirement service”, “durability”. “member support services” and “auto enrolment support to HR and Payroll”. These are the six areas that will differentiate good from bad master trusts going forward. What’s more, they allow employers to compare master trusts with contract based alternatives and assess the suitability of both within a single balanced scorecard. We don’t concern ourselves with the details of member record keeping or the complexities of fund administration, securing assets or of the internal controls within the trust. Sure these are important in themselves , but they are matters for each master trust to deal with themselves. There needs to be oversight not this system of mircro-scrutiny.

Where the Regulator has gone wrong

I have worried about tPR DC regulation since it abandoned the “6 DC outcomes” approach in 2011 in favour of the muddled 6 DC principles and the chaotic 31 characteristics, I am afraid that while this paper endorses the tPR approach it does very little to put public faith in Master trusts. Nor does it work with the existing standards to which many master trusts already comply In the Pension PlayPen’s response to the DWP command paper, we suggest that pension administration standards already have a clear assurance framework through Margaret Snowden’s PASA. The Pensions Quality Mark has its own standard to which Mastertrusts can be accredited. Nor does it work with other regulators- most notably the FCA In April NOW pensions voluntarily signed up to FCA so that it could market its investment approach to and through third party platforms. We are not suggesting that Master trusts need in themselves to be regulated by the FCA, but we need to understand that with IGCs in place the GPP and the master trust look increasingly similar. So neither the ICAEW or the Pension Regulator can ring-fence the regulation of master trusts. Besides, much of the decision making on the choice of master trusts will be taking place with no prior knowledge of pensions. These workplace pensions will be marketed in what was previously a retail space. Nor does it give ordinary people any help with the decisions they have to take Whatever goes on at retirement will either have to signpost or compete with retail alternatives (individual drawdown and annuity). Does this Assurance Framework provide any comfort to members struggling to take decisions prior to , at or after retirement? Nor does it help small or micro employers understand what makes for a good master trust. For SMEs and micros (the vast majority of employers taking decisions), something simpler and easier to understand is needed. Does it begin to address the problems employers have establishing whether the master trust can work with their payroll administrators and HR function to help stage and manage auto-enrolment? Does it begin to address the problems employers have with legacy pension schemes? Does it consider the roll of master trusts as aggregators of legacy workplace pension schemes (and failing master trusts)?

So what will it do for master trusts?

Speaking to the CEO of one of the big three DC master trusts last week, I got the impression that a series of simple laws that outlined the obligations of master trusts was preferable to a system of guidance, audit and enforcement that makes a mountain where a molehill would have done. It will kill off many smaller master trusts, but it’s a sledgehammer to crack a nut. L&G estimate that the cost of auditing this will close down all but those master trusts with large pre-existing revenue streams. Even for the large schemes, it will reduce the scope to deliver better services or reduce costs for existing services. I am sure that tPR will not weep buckets about this but I think there are better ways of achieving consolidation than handing a large cheque to the accounting industry. The requirements within the DWP Command Paper (along with the obligations on Trustees from the Treasury Command Paper) will sort out the sheep from the goats in any event. The Master trust will do little that wasn’t already done, but it will do much unnecessary harm.

The debate continues

One good thing that has come about from the ICAEW/TPR proposals is that we can now have this debate. Well done you -Andrew! BUT – I don’t want workplace pensions handed over to the accountants . I wish we’d never handed them the keys to our DB system. I don’t say this as an actuary (I am not an actuary), I say this as a DC punter who has a commercial and personal interest in restoring confidence in workplace pensions. I understand that David Harris will be speaking on this subject at workplace savings live next week. The approach being adopted in the UK does not appear to have worked in other countries. I have yet to find one industry commentator who actually endorses the Master trust Assurance Framework. If the ICAEW and tPR cannot convince me that the future of master trusts is safe in their hands, I very much doubt they can do much for the vast majority for whom this Assurance Framework is a complete irrelevance. Let’s hope that we can use a day at Edgbaston (next Wednesday) to get this matter properly debated.