This blog’s been prompted by a meeting with the egg-heads at Cass Business School who are investigating what can be done to make the default investment options better.

This blog’s been prompted by a meeting with the egg-heads at Cass Business School who are investigating what can be done to make the default investment options better.

I’m pleased they are getting stuck in. At the moment, what “action” there is in this space, is being taken by NEST and NOW who are resourced to put theory into practice , by the leading firms of investment consultants who have taken to managing the options themselves (tactical asset allocation overlays) and by the insurers who are tweaking pure equity strategies into what they call multi-strategy funds.

There is a fundamental dynamic at work here, as funds under management increase, so does the time and money devoted to managing these funds. And funds under management will increase because DB plans are now closed for new entrants (in the private sector) and because 11m more people will be saving into DC plans because of auto-enrolment.

I haven’t time or expertise to analyse whether the money that NOW or NEST are pouring into the investment management of their funds will pay off. I ‘ll point out that as an investor in their defaults you are currently getting a “free ride”. In the case of NEST, the costs are picked up in the DWP loan (which is supposedly to be repaid by policy holders). In NOW’s case, you are piggybacking on the success of the parent ATP’s asset grab in Denmark.

In the case of the consultants who are operating defaults of their own, the cost of the management is passed on to the member of the scheme being advised by the consultant, which is fine as long as there is scale. But this doesn’t sit so easily with the vast bulk of employers who cannot afford the underlying service. There are governance issues here , as always with Fiduciary Management and the “vertically integrated model“.

At an operational level, the slow but inevitable move away from lifestyle and into target dated funds is under way, the operational inefficiencies and risks of lifestyle are not tolerable in a world where we take fund governance seriously.

The true cost of portfolio management is about to be revealed. Better disclosure, better understanding and better practice are needed if we are to properly measure the operational efficiency of our fund managers. At the moment we can but guess, for which reasons , most consultants stick with what they know and understand, the passive approach.

But all in the passive garden is not rosy. Recent attempts by some insurers to move from using insured pooled funds to “wrapped OEICs” demonstrates how little they thought we knew about tax.

Thanks to good consulting from LCP and Towers Wason, the insurers trying it on were headed off. That I knew nothing of this till PJ Zoulias and co talked me through the issue, demonstrates how diligent experts can protect us from the unknown (un)knowns.

We need more diligent experts!

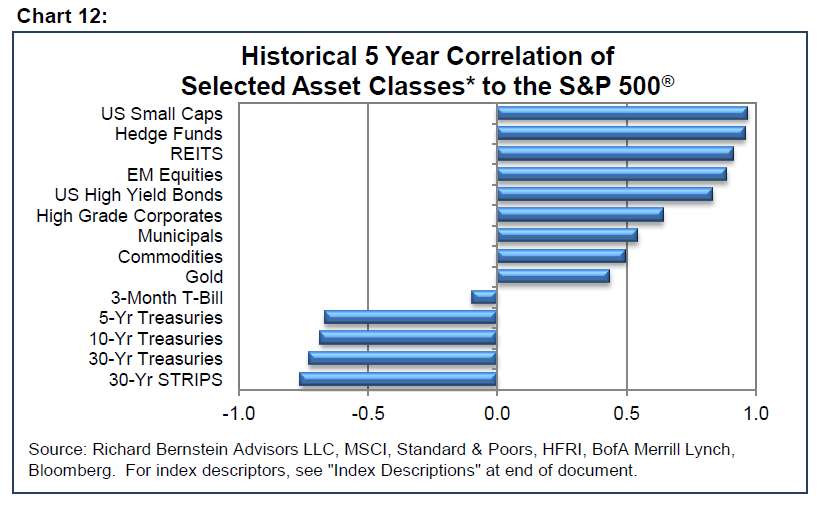

Which gets me to the grist of my blog. The current “big idea” in investment consulting is that the “only free lunch to be had from the markets is through diversification”. This is not a new idea, it underpins the idea of the balanced or managed fund that we’ve lived with since the early 1980s. But the “new balanced” approach is deemed superior as it calls on multiple strategies that can include such cuties as private equity, infrastructure, commodities and various other alternative strategies which we can bundle together and call “hedge funds”. These multi-strategy funds that call themselves Diversifed Growth Funds (DGFs) are fine in theory, but they’re so massively expensive to run that they struggle, net of fees , to deliver any value and can -very easily – destroy value. Certainly not a “free” lunch!

A cheaper and more efficient way of getting the free lunch is achieved by what experts call a “derivatives-based approach”. Here , rather than physically investing in funds that get you the diversification, you can flit between asset classes using derivatives to get you “exposure”. This sounds sexy (especially to the exhibitionist in you!) and it certainly has come up with the goods. The Standard Life GARS fund which leads the charge here, has delivered since launch. Nonetheless, the cost of this approach is still high and its it hasn’t historically been easy to see what it really costs or what is really happening. Like the old with-profits approach, it leaves a lot on trust.

In contrast, Legal & General investment management have, for some time now, been running a very cheap and transparent fund which co-mingles many of its passively managed funds (which get invested in more esoteric areas) with its core range of equity and bond funds. There is a little bit of management between the asset classes but not much. That’s because you don’t pay much for this diversified approach than you would for a passive equity fund. This approach is often referred to as “diversified beta”.

Our view is that what extra you pay is worth it, and in as much as it makes a cheap passive approach only slightly more expensive, it is a credible alternative to global equity growth funds. It looks like this approach is being replicated by other insurers on the basis that if all the sheep in the field look the same, you won’t be able to pick anyone out for slaughter.

If the diversified beta strategy (inside a TGF not a lifestyle option) is at the cutting edge (accepting that the GARS approach does not sit within the TKU of most schemes), then what’s happening on the other side of the knife?

My guess is that in two or three years time, we will be talking about alternative passive indices, in particular RAFI and TOBAM but also some more that emerge (Terry Smith is rumoured to be interested in this idea).

What’s this, it’s the idea that you can diversify not by spreading your money across many asset classes and using market timing devices to get added value, but by using better means of passive investment within a given market – typically equities. The idea is based on an analysis of key equity indices such as the FTSE where the index is constructed around market capitalisation. To put it simply, those companies which are worth the most get the most investment , this creates market distortions (bubbles) which are effectively bets. As with most bets it is the booky not the punter who wins. In this case, the booky is the market and the punter is the investor.

To take the bet out of investment, firms such as TOBAM look to recreate the market on a more fundamental basis, not using finger in the air economics but complex mathematical models (much loved by actuaries!). They ague that the purity of their investment gives more opportunity for the “equity premium” to emerge. In layman’s terms – they think they are offering us the free lunch at a fraction of the cost of the GARS approach, more effectively than the diversified beta approach and a whole lot more efficiently than the fully active DGF approach.

This is how the market looks on this day 25/02/13. I don’t have a crystal ball but I would say this is the agenda for the foreseeable. What I’m encouraged by is that we are at last setting out the terms of reference for what makes for better DC defaults and from these terms should emerge better information, better measurement, better governance, better returns and ultimately better pensions. When people see the jigsaw being put together , we may even get better public confidence in workplace pension schemes – something devoutly to be hoped for!

Related articles

- Poor execution – a pigsty – not a playpen (henrytapper.com)

- Bothered about your pension wealth? (henrytapper.com)

- Taking meaningful investment choices off the shelf (henrytapper.com)

- Vertical disintegration (henrytapper.com)

- Diagnosing the real cost of DC (henrytapper.com)

Henry

This is an interesting blog. There are a couple of issues in my mind. First, you quote the “only free lunch to be had from the markets is through diversification”. But it is not really a free lunch at all. Even the derivatives based approach has costs, not just charges but potentially in the cost of explaining to trustees and members how this works. Unfortunately derivatives still have a strong bad smell and explaining that it is the application rather than the product is a difficult sell.

I am a fan of diversified beta; particularly exposure to asset classes such as infrastructure but again explaining it to your average punter is an expensive business. I liked your comments on TOBAM but the issue of using complex mathematical models do not have a good history. Was there not some form of long term growth fund run by a Nobel economist or two that caused more than a ripple in global markets a few years ago?

Herein lies the rub. I agree that having confidence in workplace pensions would be fantastic, but my view is it has a very low probability. There is a lack of trust in both pensions and financial products that is unlikely to be rebuilt in our lifetime. The continuing financial services scandals such as LIBOR fixing and over the next few years the very poor performance of endowment policies is not going to change that perception any time soon.

The customers want a guaranteed risk free return sufficient to meet their retirement ambitions. Such an animal does not exist nor is likely to exist anytime soon if at all. You know better than I do the projections on long term asset class returns. The vast majority of those in the workplace, in SME’s are doomed not to achieve their retirement ambitions, if they ever seriously get round to saving for them, which from recent evidence is unlikely.

Should your projections on new forms of investment be correct, and I very much hope they are, the beneficiaries will be those who have the capital and knowledge to invest in the time, effort and savings regime necessary to build up a “decent” retirement pot; that is if the Government (of whatever political colour) does not continue its short-sighted approach on pension savings and try to kick the pension football in to the long grass out of sight until it becomes some else’s problem. For everyone else the prospect of working until death is a very real possibility.

Thanks Ian, I hope I make it clear that the better ways to diversify don’t involve solutions that cost too much are unintelligible or simply don’t work!

“But all in the passive garden is not rosy. Recent attempts by some insurers to move from using insured pooled funds to “wrapped OEICs” demonstrates how little they thought we knew about tax.

Thanks to good consulting from LCP and Towers Wason, the insurers trying it on were headed off.”

You got any further info on that? – I’d be glad to know….

Maybe we could take a lesson from Greece

Pingback: “Three into two won’t go”- NO EXIT at Playpen lunch! | The Vision of the Pension Plowman

Pingback: We should measure pension fees as “risk” | The Vision of the Pension Plowman

Pingback: Should we measure pension fees as “risk”? | The Vision of the Pension Plowman

Pingback: DC4Good; ABdc and the Pension Trust get it. | The Vision of the Pension Plowman

Pingback: PlayPen votes for target date funds in action-packed lunch | The Vision of the Pension Plowman