The Pensions Regulator has scrapped a plan to list auto-enrolment schemes on its website. We in the Pension PlayPen are pleased. We put our views to the Regulator (you can read them here), we can sum them up by saying that “if a job’s worth doing, it’s worth doing well”.

The Regulator agrees saying that it has now dropped the plans over fears the list could not be objective and transparent with our substantial assessment of all listed schemes. This was precisely our point. A bald list of schemes prepared to quote for everything would have presented a charter to every snake oil salesman and seamster who chose to set up a master trust or rent an personal pension licence.

The last time the Regulator tried something like this was for Stakeholder Pensions and that list has not been updated since 2001! So well done the Pension Regulator for listening.

We all agree SMEs and micros need support choosing a pension

I think there is a consensus that we need to find a proper way to support small and micro employers finding their scheme.

We believe this way exists and, I’m pleased to say it has already been used by hundreds of employers up and down the United Kingdom – it is of course http://www.pensionplaypen.com.

In case anyone is in any doubt of the seriousness of our project, we will be meeting with the Pensions Regulator next week to discuss with it what can be done to ensure that employers do not sleepwalk into NEST or any other “default provider” put up by an auto-enrolment adviser.

Do we want a big three?

This is a rather more positive position than that reported in Money Marketing by NOW and The People’s Pension. Their moaning about tPR favouriting NEST is understandable, the DWP owns tPR and it’s put £600m behind NEST but I do not get any sense from the Regulator that they “it will only flag NEST”.

NEST reported in its Insight 15 document that many providers they spoke to looked no further than NEST and, if they did, looked only at People’s and NOW.

This is not a good situation, any more than having a premier league comprising Chelsea , Man City or Man Utd. Currently Legal & General and Standard Life are regularly chosen from http://www.pensionplaypen.com and there is a long list of insurers and mastertrusts that are used less often.

Where would a premier league be without West Ham,Southampton and Swansea?

We suspect that the lack of research by employers is not because they do not want to know what is available to them, but because there is insufficient awareness of “teams lower down the leagues” that are particularly relevant.

If you are a construction company in Northern Ireland , you should not ignore the Workers Pension, if you are a Social Housing organisation, check out Pension Trust’s Smarter Pension and if you are a member of the Federation of Small Business, get the excellent terms they offer on the Scottish Widows GPP.

Many of these propositions might normally be overlooked, but provided you fill in our fact find, you will find your way to these workplace pensions.

Informed choice, comes from knowledge not lists

I was asked by Money Marketing for a comment on the criticism of the Pension Regulator and have made this statement

Nest is not the only fruit and employers who don’t look at alternatives are failing their staff and leaving them exposed to criticism or even litigation, especially if the scheme chosen under performs. NEST acknowledge that employers should document why they chose NEST and there’s no way an employer can do this without reference to other schemes.So employers need to know the choices available to them and in theory a directory is a good idea. But in practice, the directory tPR was proposing could not work. The only criteria for inclusion would have been that the scheme qualified and was open to all employers. This would have been a charter for every snake oil salesman in Britain to legitimise their product on a Government site,Information is not knowledge, knowledge comes when the information is presented in a sensible way that enables employers to make informed choices. The Pension Regulator took the decision that they could not present a directory that was ambitious enough to give employers guidance. Working on the principle that if a job’s worth doing it’s worth doing well, they decided not to do the job at all. We think this was the right decision.

How we shortlist providers

I’ve been asked to provide a statement of how we choose who appears on our shortlists

All the credible providers are researched. Occasionally a provider who meets our criteria will not complete due diligence and chooses to be excluded. Currently two products that meet our criteria for selection are choosing to be excluded (Corporate Vantage and Supertrust).

Sometimes, providers choose to be temporarily excluded. Friendly Pensions is an example of a provider that has asked to be excluded for a quarter as it makes changes to its proposition.

We want http://www.pensionplaypen.com to be inclusive, but respect providers who do not want to be researched and have their products compared.

We do not currently include the GPPs offered by advisers which dress up existing products in their clothing (examples CBS’ version of Scottish Widows GPP) or Aon’s version of Blackrock’s GPP).

We don’t currently include those mastertrusts set up for advisers to market their own investment styles.

And we will never include any workplace pension that does not provide us with all the information we need to complete due diligence.

There is good reason for these exclusions. Choice has to be meaningful. Where the underlying governance, administration and at retirement processes are identical, we think the tweaking of investment options and member communications is little more than re-branding and we will not offer variants on a core proposition merely to put advisers into play.

Transparency in all things.

http://www.pensionplaypen.com does not claim to be a definitive directory, but it offers a wider range of choice than any other service.

We are happy to share with the Regulator not just the methodology, but our fundamental research and the underlying ratings which we give providers.While much of this research is not ours- but the property of First Actuarial, we will share, with First Actuarial’s permission, our ratings with providers.

We publish a range of guides and research documents at https://www.pensionplaypen.com/guides which tell our customers how we do this.

We also publish our guide to how we apply our research which can be found here

Our directory is properly formulated and properly maintained, it is as inclusive as we can make it and we aim to ensure that an employer using our service (or the adviser) can present all meaningful choices that are available to it.

Meaningful choice at the right price

The current retail price for using our “choose a pension” service is £499 (+vat). This includes the support of either ourselves, or where we are working in partnership with an adviser such as First Actuarial, Alexander House or Abacus – our partners.

Where support is not provided, we have considerably less overhead, there may be scope to reduce our price where a client is self sufficient or where our service is embedded in a a holistic auto-enrolment service.

For employers, unused to having to pay upfront for financial services products – any price is initially a barrier (this is the pernicious legacy of a commission system that kidded employers that advice was for free).

However, as the numbers of employers choosing a pension increases and the capacity to introduce self-service increases, we believe that we will be able to reduce the cost of using our service substantially.

But auto-enrolment costs

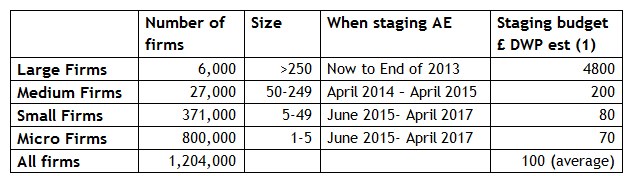

The DWP and tPR have generally done a great job so far. Perhaps my one serious gripe is the publication early in the process of these numbers

The original cost assessments for staging auto-enrolment produced in 2012 by the DWP (above), created a false expectation not just to the Treasury but to their own civil servants that AE was pretty well for free.

It is not possible to set up the complex processes needed to implement and manage auto-enrolment, let alone research and select a proper workplace pension within these budgets.

Next steps for the Pension Regulator

When we meet the Regulator next week, we will be calling on them to research the actual costs of auto-enrolment , both in terms of internal management time and in the purchasing of outsourced services.

In particular, we would like tPR to work with us to scope what employers should be doing to choose a workplace pension. Once scoped, we’d like tPR to cost that process within a range of options , ranging from the belts and braces approach adopted by larger employers employing a manual process to the bare minimum acceptable standard (let’s say a properly researched view of the market culminating in a reason why letter made available to staff and employee representatives).

I challenge tPR to find any service that can put meaningful choice to an employer and document that choice and the decision taken, for less than five hundred pounds.

No short cut to best practice

I think we will look back at tPR’s decision as a tipping point in our progress towards national enrolment.

By rejecting the easy option of a Directory, tPR has put “informed choice” back on the agenda of smaller employers. But it is not enough for tPR to just wash its hands of pensions (it is the Pension Regulator), tPR must now insist on SMEs and micros choosing a pension for staff- or if delegating this responsibility to an adviser, having that choice made in an informed way.

The alternative will be for up to a million companies having workplace pensions which they know nothing about and many millions of staff investing in schemes that might as well have been purchased in a car-boot sale.

There is no short-cut to best practice.