The very brilliant Mark Polson has written a very brilliant article which can be found on Financial Adviser’s website. The gist is that what we have is not fit for purpose and we’d better off concentrating on existing products than chasing silver bullets.

Which is what I think. I am more than happy to devote my time to helping people save money into pension plans that work properly than chasing rainbows. Pension innovation is usually a euphemism for finding new ways to make intermediaries money and is generally not helpful.

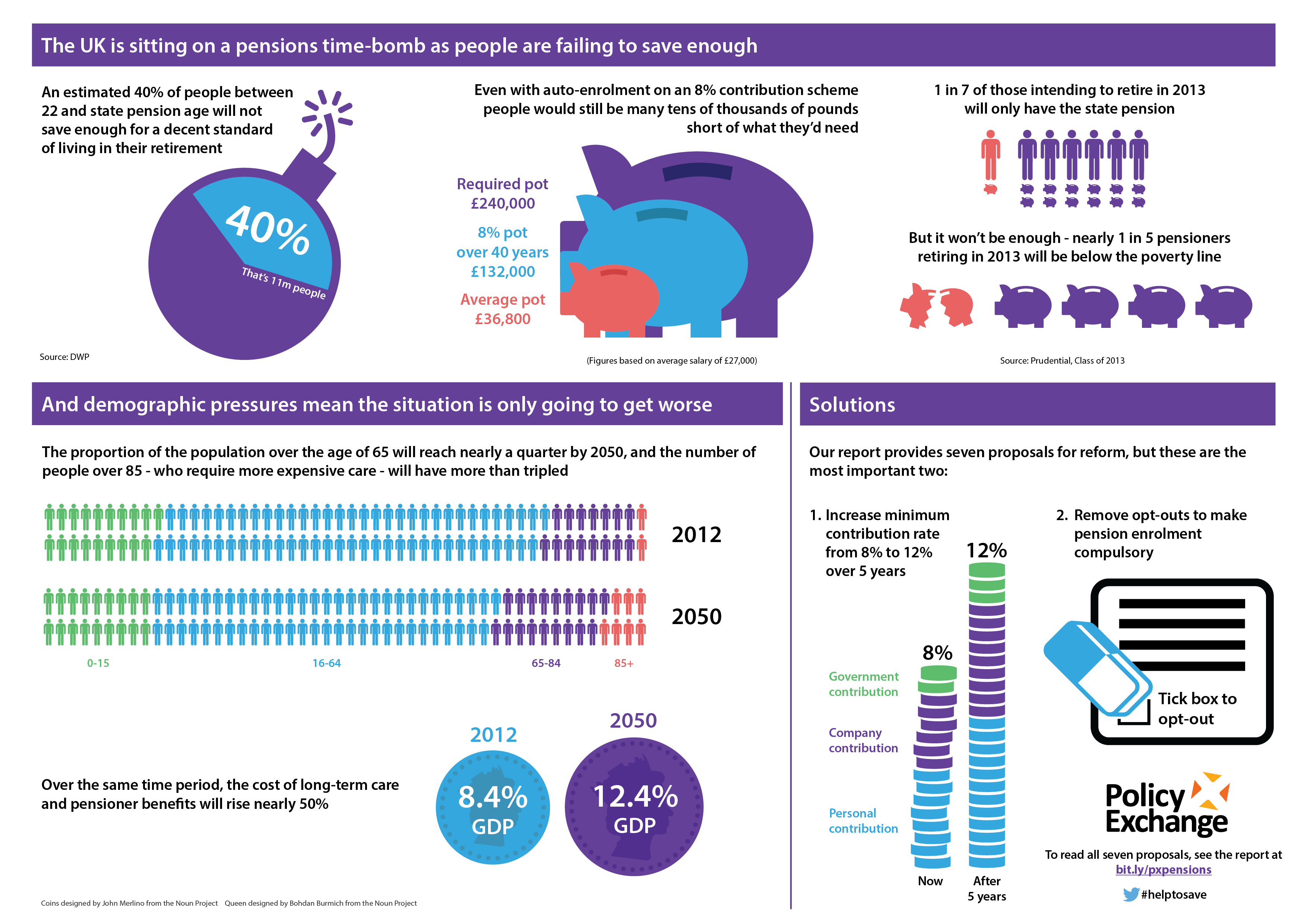

Amidst all the noise around the charge cap, two pensions reports have arrived in the past two weeks. One is full of unhelpful innovation and the other focusses on getting us to do what we do badly-better.

The latest is from Policy Exchange (click here) and has two main recommendations. Firstly that we close off the opt-out button on the Auto-enrolment machine making it the “once you’re in , you’re in” machine and the other that there be an auto-escalation of contributions raising the target savings rate to 12% rather than 8%. Effectively this is what has happened in Australia.

I’m afraid that most of this falls into the “unhelpful innovation” box. Increasing contributions into workplace pensions without improving workplace pensions is like pouring a magnum rather than a bottle of champagne down the drain. Turning off an opt-out to a pension system many do not trust is like shaking a full bottle of champagne till it explodes.

The report also argues that the Government should issue annuity bonds (an idea frequently recommended on this blog as Pension Pounds) and ease the rules on drawdown to solve the annuity crisis. Nothing in the report is wrong but all these ideas involve major government interventions. Force majeure will not solve the pension problem (nor will reports from Hedge Fund Managers like the Policy Exchange’s James Barry). We have seen what happens when Governments try to intervene in the market – we get a debacle like the charge cap consultation.

To give Policy Exchange their due, the report does come with an excellent infographic

The earlier report from the Pension Institute is an altogether better document, because it is the work of people who are not trying to change the world but to make what we have , a little better. The Pension Institute report published on 16th January deals with the consequences of high charges , of trapping people in high charging products and of poor decision making at retirement.

But rather than impose solutions from outside, it calls for us to do better with what we have. To return to Mark’s article, it’s not innovation that’s going to bring down charges, or improve the portability of pensions or even solve the annuity crisis, it’s a re-focussing on doing the things we already do-better.

Take the first of the three – charges. I know and so do the fund managers, that there is a lot of inefficiency in fund management and that most of this is passed on to investors through higher than needed costs to net asset value. Much of this money is simply left on the table and being bagged by the flotsam and jetsum of the City and paid out to same as obscene bonuses. You can moan as much as you like , but unless you put in internal controls and manage those controls, these costs will continue. You need a way to measure what you are paying, benchmark what you are paying and stop paying too much. It’s called governance.

Take the second of the three- the hopeless mess which is the pension transfer market. it is a mess because of misconduct which has led to over-regulation and ultimately to paralysis. For most people, the business of transferring pensions is either too hard or too expensive for them to bother. The answer is not to reinvent the world along the lines of pot follows member, but to revisit each process in a transfer so that individuals can freely move money from place to place using straight through processing. It takes a bank seconds to process money from my account to theirs, why does it take ten days for the Prudential to send money to L&G? Again the answer lies in making what we do better and in the governance of the process to make sure it works and continues working,

Take the third of the three- annuities. Until the late eighties , almost all the pensions paid out in the UK were paid out through pension schemes as scheme pensions. This idea of the guaranteed annuities related only to retirement annuity plans which were generally used by the professional classes who were self-employed and not eligible for a scheme. If you weren’t in a scheme, you probably relied on the old age pension and SERPS.

The annuity problem stems from trying to graft a mass-market solution onto an annuity infrastructure designed for a few rich people. The development of open market annuities resulted from the decline in guaranteed annuity rates and the increase in mass marketed personal pensions. The system we have today relies on an advisory infrastructure that hasn’t existed since the mid eighties and a customer profile which is totally at odds with the type of people now annuitizing. The issue is not to be solved by Government intervention (though we might need a short-term fix so acute is the current crisis). The answer is to be found in the solutions that prevailed before personal pensions came along. Namely that people are paid pensions from properly governed schemes and are not exposed to the shambles which is annuity purchase today.

The drift of my article, which I hope supports Marks, is that we do not need innovation, we need renovation and in some case restitution. The technology to measure and manage the problems we currently face is already in place. It simply is not applied.

The answer to the real problems identified by Mark, by the Policy Exchange and by Harrison and Blake of the Policy Institute lies in doing things better not in doing things new.