I think the question needs to be asked as MaPS’s seminar entitled”Creating a UK Financial Wellbeing Movement” presumed that the 170 people who joined its webinar were as one with MaPS’ vision – launched on 21 January 2020 which can be read here: https://maps.org.uk/wellbeing

The Money and Pensions Service tells us it has

“spent the last 12 months working with partners across the UK to develop a national strategy on financial wellbeing: creating a roadmap for how different individuals and organisations can work together over the next decade to help millions make the most of their money and pensions”.

They tell us that

MaPS is now looking at the strategy’s priority areas in detail, creating specific delivery plans, and setting milestones for our ten-year journey towards better financial wellbeing. We are forming a movement bringing together individuals and organisations who want to put financial wellbeing at the heart of their purpose.

and promises that their webinar would dive into the detail of the strategy: identifying how we will all work over the next decade to bring benefits for individuals, their communities and wider society.

Why MaPS matters to me

MaPS is taking the resource for this work from the pensions industry and ultimately from the savers and borrowers whose behaviours it is hoping to influence.

So this strategy is the property not just of MaPS and its “arms length” owner – the DWP, but each and every one of us.

My comments are from me as a particular stakeholder in MaPS as I want to plug into its strategies, especially the problems we are facing with personal debt, our lack of planning for retirement income and for the issues we have with declining health in old age.

I am not clear from this webinar, that the structure MaPS are putting in place achieves the aims it is setting out for itself and I think it’s worth laying down my challenge now, rather than complaining in 2030 – when I’ll be 69 – when it will be too late.

MaPS make it clear that it is not London centric but will be active accross the UK

I would like to see evidence of MaPs’ footprint beyond its Holborn Circus HQ. It looks very London centric to me.

The delivery of the activation phase from launch to 2020 is subject to the current situation with Coronavirus. I would question how this can be delivered.

The delivery of the mobilisation and activation of the strategy depends on the engagement of a “wide range of organisations and sectors”. What are they and how can they activate the strategy. The challenge is to evidence the engagement of third parties – especially connected third parties (eg beyond Government) .

If these are the ten year goals of the Financial Wellbeing project then we need to understand what part of the achievement of these goals is attributable to MaPS and what to private organisations. What has to happen is that MaPS – rather than taking the credit for the private sector’s efforts, supports those efforts by incentivising them. By this I mean making MaPS resource available to those who help people save, borrow and plan for the future. My challenge to MaPs is to show how it will be providing (rather than just marshalling) the resource needed to hit these targets

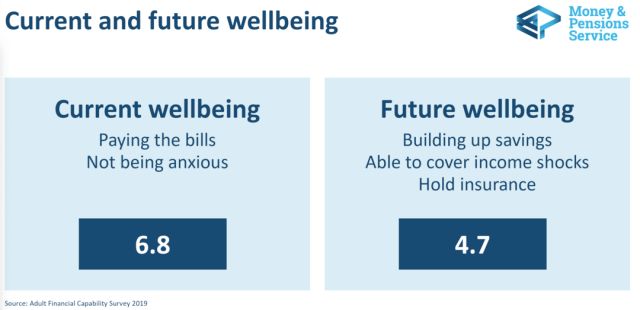

I rather doubt the current wellbeing score is “in date”, I suspect it is now lower than the future wellbeing score -which is the point – future wellbeing is harder to attain but more durable.

this complicated model ignores the impermanence of wellbeing – resilience is not the same thing as wellbeing – it is what we are currently calling on. The depths of our resilience are being tested – resilience is not part of this model (and needs to be).

I should point out at this point that the 170 of us who wanted to feedback had no opportunity to do so as the “hands up” sign was not responded to, the audience was muted and (on my browser at least) the capacity to use the question box illustrated , only worked if you could find a turn-on switch on the GotoWeb dashboard.

As an example, I was unable to ask what an index could do to enable “others” to monitor their customers or beneficiaries – can MaPS explain?

This slide shows what an outlier poor mental health is. It properly illustrates how important resilience is, I fear that the mental health issues prompted by the current pandemic and the lockdown – are going to be an immediate issue for MAPS. Jus how much resource can MAPS put towards a public imagine their future wellbeing slipping through their fingers?

The income shocks currently being experienced by the UK population are substantial and it will be interesting to see if – once we have weathered this storm, we become more cautious and set more money aside. My experience with the pension freedoms is that people are reluctant to entrust their money to long term products (like annuities) where they don’t have access to their cash. Is the current crisis going to increase the value of liquidity rathe than the prudence of insurance? What is the need for saving?

Which is my point. A savings buffer is often at the expense of insurance.

This slide begs another question. Did MaPS really need to spend a year working this out?

The “key question” is immediately answered , 17% of us borrow to pay for essentials

These findings are marginally more interesting but there’s nothing here that should surprise us!

This slide is of use, if we are identifying those with mental health problems as the worst borrowers, we should be very worried about plans to lend such people money to get them through the Coronavirus crisis. indeed , we should be doubly worried about putting people further into debt at such a time of stress.

So how do we solve problems?

I am afraid that much of the solution to these problems involve financial education in schools and in the family home. My worry is that we give up on the current generation and try to find a perfectly behaved future generation.

This is fine so far as it goes but does little to solve the issues of today’s workers.

But I find phrases like “meaningful financial education” hard to get my head around.

Similarly we know that those in later life are have financial issues, but is this where MaPS can make most difference? How can a money and pension service help those who are in physical and cognitive decline. Are they not in the same position as children, increasingly dependent on those of working age?

Guidance makes a difference to those who are trying to turn pots into pensions, but the numbers not taking up the free guidance MAPS offers , suggests that the majority of people are neither taking advice or guidance. How can MaPS work best with the private sector to change that?

What do working age people need to know to plan for their retirement? Someone who has saved £100,000 by January may now have £65,000. Drawdown plans are liable to massive sequential risk in the current client. What can people do in their thirties and fourties to plan for the future other than to save as much as they reasonably can?

If people could have foreseen the Coronavirus, would they have put more into pensions?

Debt is something that millions are going to find themselves in and through no fault of their own. Redundancy looms large for many of us as businesses fail. What is MaPS doing to help?

I will stop there.

I spend a lot of time in hospitals and doctor’s surgeries. I see the NHS dealing with people who are frightened by their mental and physical frailty and I see how they manage that fear.

We need to do the same, managing the root cause of much of the mental anxiety that fills the surgeries.

At this time of crisis , we need to be deploying our resources to meet the immediate needs of our customers and MaPS should be no different

As you will gather from my comments, I find the MaPS strategy too abstract and insufficiently grounded. I would like MaPS operating like a financial NHS and not as a think-tank and co-ordinator of other’s activities.

I wouldn’t agree that MaPS is creating a UK Wellbeing Movement, at best they are revealing and encouraging what we have in place

MaPS says it is open to challenge and I lay down this challenge.

Henry I fully agree with your concluding comment

“I would like MaPS operating like a financial NHS and not as a think-tank and co-ordinator of other’s activities” – please see http://www.ariesinsight.co.uk/webfront/vlogpod16.htm

Thanks for highlighting this, Henry, but I fear your observations are indicative of coming late to the party. MAPS is not a johnny-come-lately outfit. It is the latest incarnation of a movement that has been building since the year 2000, when David Blunkett convened the Financial Literacy Advisory Group (AdFLAG), drawing in a really wide spectrum of organisations, including educationists, third sector organisations, policy groups and the private sector. The FSA went on to be the flagbearer for this group and devised the first Financial Capability Strategy after one of the most detailed pieces of social research this country has ever seen.

Over the years since then, the number of people and organisations has grown and grown. The FSA’s role was handed on to the Money Advice Service, which in turn morphed into the current Money and Pensions Service. It is not a London-centric operation. They have officers across the UK and the organisations that they engage with are similarly widespread.

You warn against MAPS merely taking credit for what the private sector does but, in recent years, it has largely been the work of MAS/MAPS that has fired up the interest of the private sector in looking at the financial capability of its workforces. All this has been done against a backdrop of experimentation and evaluation that would put many academic organisations to shame. Private sector companies have participated in evaluation of their financial education programmes that has rated them less than stellar but they have still been brave enough to post these results online – keep coming back for more.

Is MAPS perfect? Certainly not. They have their flaws and challenges like the rest of us. Successive governments have decided that the campaign for greater financial wellbeing and capability should not be a megalithic NHS-type operation but is best pursued through the vast network of national and local organisations from all sectors that have been largely marshalled together by MAS/MAPS. Your financial NHS is never going to happen in the UK. It’s not our way and I suspect it’s not really your way.

The campaigns over the years to change the relationship of the public with their money is like the classic image of getting an oil tanker to change direction. It is a long haul and I for one am glad that the Money and Pensions Service is in it for the long haul.