There appear to be two versions of the Treasury’s costings of these new found freedoms we’ll be getting post April 2015.

The first were published at the time of the budget and (with the proviso that the Treasury don’t know how people will actually behave) deliver savings that rise from £320m in 2015 to £1.2bn. per year after 2017. One quick look at the tax planning opportunities available from the new Pensions Freedoms led to a dismissal in my head of the treasury’s assumptions , do they think that the Great British Public are so stupid as to pay that much extra tax?

The second aren’t published but exist They’re the ones based on a reasonable expectation of GB taxpayer going on Money Saving Expert and working out how to draw down up to but not above their marginal tax-rates. We suggest these figures are not so optimistic (from HMRC’s perspective)

I produce an extract of a letter from the Government’s Information Rights Unit to Gregg McClymont (with the Shadow Minister’s kind permission). Gregg had asked to see the new figures so he could make his own assessment (as you do when you are the minister in opposition).

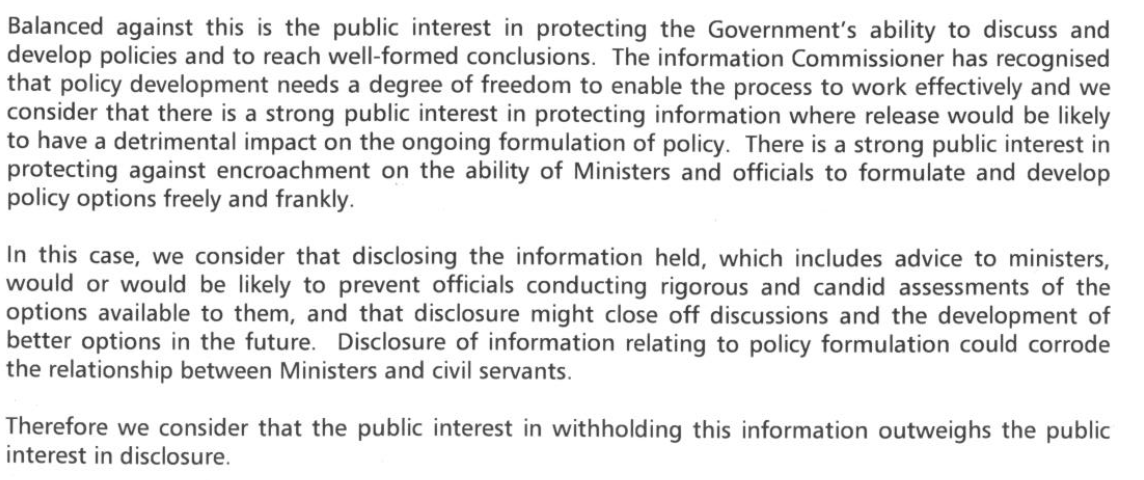

The letter trots out the standard argument for allowing people (including Shadow Ministers) to know what’s going on (especially when they are being asked for their views by way of a public consultation) but concludes that..

It is worrying that a public consultation is going on without full access to the Treasury’s costings.

It is also worrying that Government Ministers feel they cannot create policy without exclusive access to the information the public are trying to consult on.

It is most worrying of all that the information in the public domain which is the information on which the public are consulting is not the information on which the Ministers are forming their policy.

In this most ” Sir Humphrey” of letters, John Sparrow of the Information Rights Unit, tells the Shadow Pensions Minister that

“disclosure of information relating to policy formulation could corrode the relationship between Ministers and Civil Servants”

It is hard not to agree with John Greenwood, writing in today’s Telegraph that the

“Government finds itself on the horns of a dilemma,. It will have to reduce some of the perks and attractions associated with pension savings if it is to continue to offer over-55s freedom to spend their pension pots as they wish”

What everybody is speculating about (publicly) is the loss of tax-reliefs including curtailment of tax free lump sums, higher rate contribution relief and extensions of the restrictions on pension capital (lifetime allowance).

What nobody is talking about (publicly) is what the long-term cost to the country will be if a substantial wedge of our pension savings is blown on Lamborghini like fripperies in the early years of people’s retirements.

Somebody has to pick up the bill for long-term care and for the dependencies of extreme old age. If it is not the pensioner- it must be the taxpayer; an inter-gernerational transfer that may not play so well on generation Y and beyond.

Clearly these are the kind of debates that are being had behind the doors of the Treasury (which John Sparrow is at this moment locking).

I’ll shut up now , I think I can hear someone at the door….(they are wearing black leather costs and carrying guns).

Here is the stuff that we – the public – are being fed. Be aware this is not be the same as the information on which decisions are being taken by Ministers (taken from the budget costings published on this link

Post-behavioural costing

The costing depends upon an estimate of the number of people who make use of the additional flexibility. This leads to an increase in income tax received in early years as individuals will now pay tax on the withdrawals from their pension pot. Because more people make withdrawals there will then be reduced income tax on annuity pension payments in later years.

The proportion of pension pot holders who choose to make early withdrawals is forecast by estimating whether an individual would have a preference for present income over later income.

This preference is estimated using information on individuals’ current financial positions using data from the Wealth and Assets Survey. It is affected by their indebtedness and the returns available on investments outside the implied returns of annuities. Other factors which may influence take-up include individuals’ preference for liquidity and their tendency to stick to default options, which affect take-up in opposite directions.

It is estimated that around 30% of people in defined contribution schemes will decide to drawdown their pension at a faster rate than via an annuity.

Over the first 4 years of the scorecard period it is also assumed that there are additional

withdrawals from the stock of pensioners currently within capped drawdown. This further

increases income tax received over this period. Adjustments are also made for the higher costs of pensions tax relief to reflect the increased attractiveness of pension savings for some individuals.Post-behavioural Exchequer impact (£m)

2014-15 2015-16 2016-17 2017-18 2018-19

Exchequer impact -5 +320 +600 +910 +1,220By allowing individuals to flexibly withdraw from their pension pot, this measure results in

increased income tax receipts in each year until 2030. After that, a small reduction in tax receipts of around £300 million a year is expected in steady state.This is small in comparison to the impact of all the government changes on pensions, designed to ensure pensions provision is sustainable with an aging population (notably the increase in State Pension age), which means by 2030 the government is saving around £17 billion a year in 2013-14 terms compared to previous policy.

Areas of uncertainty

The main uncertainty in this costing is the number of individuals who will withdraw additional wealth when their pension pot is crystallised.

Thanks to Jo Cumbo of the Financial Times who drew my attention to the dodgy dossier that Gregg was denied access to.

I haven’t read her version of the story but I’m sure it is brilliant (though you need to be a subscriber) it can be found here. m.ft.com/cms/125210c4-e7fe-11e3-9af8-00144feabdc0.html?catid=109 …

This article first appeared in http://www.pensionplaypen.com