Transparent, measurable and comparable? How would LDI pooled funds stack up in a VFM Framework?

Slowly but surely what happened to LDI pooled funds in late September and early October is beginning to emerge.

Katie Martin of the FT has discovered that rather than declare a negative net asset value for a pooled fund, Insight create artificially buoyant fund prices, meeting the cash calls on their clients from shareholder funds rather than calling for collateral from clients. This sits uneasily with the testimony given by Insight’s CEO at the Work and Pensions Committee.

Toby Nangle writes in the FT that the losses sustained by LDI pooled funds over the time of the crisis appear to be in the region of £3bn , taken from his analysis of the anonymised data supplied by actuarial consultancies XPS and Barnett Waddingham

And Robert Buckland says that LDI over the past 20 years has destroyed the UK stock market.

Transparency, measurement and comparability – key to pension VFM.

The joint initiative between DWP, FCA and TPR is designed to empower those who pay money into pension funds to buy better and for those who take the risks of things going wrong to be alive to those risks.

The VFM Framework is designed for DC workplace pensions but its guiding principle of transparency, its emphasis on external measurement and its key deliverable, comparability and competition, can be read across from DC to DB.

Transparency

The problems experienced by pooled LDI funds and their clients – the smaller DB pension schemes are obscure because the practices of those in the market are kept hidden from sight

Marking the funds to market at September 27 rates, close to the lowest point in the crisis, would have generated a grim result. Instead, for that one day, Insight took another path. After the BoE announced its targeted bond-buying rescue scheme at 11am on September 28, which instantly pushed gilts prices higher, it gathered its five-person fund board, which comprised three independent members and others from BNY and Insight.

They decided to mark the books for September 27 higher by disregarding that day’s gilt moves and marking to market around prices that had prevailed in the middle of September 26.

“Markets were dysfunctional,” Insight told the FT. “In such circumstances, the fund board has discretion to apply a fair value adjustment to market prices. A decision of this nature is made in the best interest of all shareholders in a fund.” Industry experts say the price adjustment prevented Insight from making demands for cash of its clients. “NAVs should tell you asset values,” said one. “The injured party is trust in the system.”

But this was not what CEO Abdallah Naupha told the Work and Pensions Committee , nor what Insight told the Financial Times this month (it said that its LDI funds “operated as normal through the dislocation”. )

Measurement

Toby Nangle’s analysis of anonymised data released by consultancy XPS on the quality of service offered by the leading LDI pooled fund providers

Following the FT’s coverage of investment advisers Barnett Waddingham and XPS Pensions’ decision to advise their clients to sell specific but unnamed pooled LDI managers, XPS has picked up the Tolstoyan baton to probe the nature of their individual unhappiness in a note to clients (albeit in mostly tabular form).

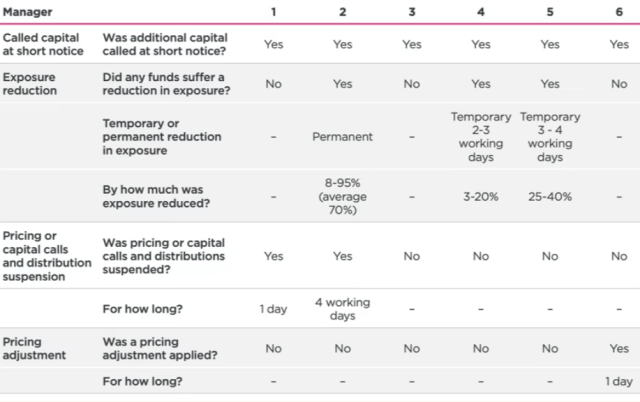

The investment adviser looks at the experience of six of the main pooled LDI managers during the gilt market mayhem. Annoyingly it’s anonymised, which is doubly annoying as pretty much everyone on the inside knows who each of the managers are. But — you know — litigation risk, relationships, blah blah blah.

It seems odd that at a time when fund managers are required to issue value assessments , while TPR is still operating Value for Members and the DWP are consulting on a Value for Money Framework, there is still a need to protect LDI pooled managers from the public eye.

Measurable

The transparency that has clouded the LDI inquest is beginning to lift but we are still a long way from knowing what really happened. We are beginning to sort the sheep from the goats among LLI pooled funds. Though we still can’t stick names to managers we can see that their performance was measured by outcomes.

Nangle’s exegesis is excellent;

One of the triggers for that negative hit to prices is that if you’re a leveraged pooled LDI fund, have already posted all your unencumbered collateral, and can’t suck in new cash fast enough to post it as new collateral (ie, you “called capital at short notice” but not everyone can answer this call).

Then you need to unwind your positions and reduce exposure: ie dump bonds, and fast. XPS reckons that this happened to three of the six pooled LDI managers. For some clients this exposure loss was only temporary (still not great!), but for one it was permanent. One of the managers reduced exposure by an average of 70 per cent. That’s a lot.

Two managers suspended either “pricing or capital calls and distributions” during the melee. This would not have been great if, say, you’re trying to make payments to pensioners, process pension contributions or pump in money to maintain hedges. That sort of thing.

One manager applied a “pricing adjustment”. Just for one day mind. Sounds legit? If this was a minor thing (maybe widening the bid-offer or applying swing-pricing on a pooled fund) it would be too meh to feature on the list. Alternatively it could be a very big deal that raises a whole host of awkward questions.

Beyond this list, XPS also say that one of the managers had a fund accounting error that screwed up their pricing for a while. So pension scheme clients didn’t have accurate information on which to base decisions. Unhelpful.

Through a series of deductions , Nangle concludes that LDI caused a 0.3% hit to funding levels. Using the PPF’s estimate of scheme liabilities, the loss versus the counterfactual (not using pooled LDI) for pension schemes comes to around £3bn.

Of course , those who have used LDI will point to the gains created by LDI over the 20 or so years it has been around (slightly shorter for LDI pooled funds).

Comparability

Of course most of us aren’t interested in technical arguments about how LDI stabilised the pension liabilities on a sponsor’s balance sheet or how it allowed schemes to circumvent pressures to fund 100% in bonds (with crippling consequences to company cash flows).

Most people – especially most people on Government committees reviewing LDI (Treasury, DWO and the House of Lords) will be asking, has LDI delivered value for money to the pension system and beyond.

Here the debate broadens through Robert Buckland’s essay. Buckland points to UK institutional investors or the demise of the UK stock market

… the biggest drag has been a giant shift in institutional asset allocations. My old clients, domestic pension funds and insurance companies, have dramatically cut their weightings in UK equities. They owned more than half the market in the 1990s. Now they own just 4 per cent.

They flocked to LDI because it offered a panacea for the trauma of the financial crisis and the impact of moving to accounting standards that required liabilities to be measured on a mark to market basis

Asset valuations collapsed. Liabilities rose as bond yields fell. Deficits ballooned. The near-death experience pushed trustees towards liability-driven investment strategies, which promised to match portfolios more closely to fund obligations. That meant selling equities and switching into gilts.

Buckland’s “big-picture” analysis points to a state of affairs that should have those in the Treasury , promoting the use of productive capital through long-term investment, gnashing their teeth.

Ironically, steps to protect pensions from falling into the PPF, have fundamentally reshaped how UK companies finance themselves, LDI’s counterfactual, the heady years of the 1980s and 1990s, have resulted in two decades of UK equity stagnation. Far from progressing , along with other equity markets, the UK stock market has hardly grown in over 20 years.

The corporate finance implications were significant. Companies raised capital in the bond markets, where UK funds were buying, while reducing reliance on the public equity market, where they were selling. The private equity industry got rich by taking the other side of the institutional switch, issuing bonds at low yields to buy cheap assets off the equity market. Private markets grew as public markets shrank.

Did LDI (in its leverage form) deliver value for money?

As with all VFM assessments, if you allow the architects of the product to mark its homework , the answer is yes, one part of LDI blew up in 2022 but one black swan does not negate 20 years of white swans.

But set against the wider tests applied through the VFM Framework , LDI (at least through pooled funds) has failed. It hasn’t been transparent , measurable and we can’t make proper comparisons. It’s net performance must be set against an alternative threshold (how would pension schemes have done if they had continued with the strategies that served them well in previous decades). Buckland’s argument is that LDI has been a net destroyer of value both for DB and for many DC pensions (which themselves have deserted UK equities).

In terms of cost, we have inadequate information but work done by ClearGlass suggests that LLDI in general and pooled funds in particular were extremely expensive to run,

Finally, in terms of quality of service, the table provided us by Toby Nangle suggests that quality was variable. As more comes out about the engineered solution from Insight , more will emerge about what was a reasonable service expectation from trustees and sponsors investing in pooled LDI funds.

Judged against the principles of transparency, measurability and comparability, pooled LDI would fail if it were part of the DWP’s proposed VFM Framework.

If you have in house salesmen of this LDI alchemy who are unregulated, managed and owned by advisers to the funds you have lost objectivity.

The accountancy profession has had this problem of concentration in the big three resulting in call for analysis of the impact on audit standards.

In banking the separation of retail and investment banking solution is being developed but only after the black swans arrived in flocks.

“one black swan does not negate 20 years of white swans.”

The LDI crisis was not a black swan event – it was certain to happen given the scale and structure of the contracts used. But let’s ask if there really were 20 white swans before that.

Many, such as the 100 Group, have claimed that LDI produced strong returns over the period to the end of 2021. None have offered any evidence to support this assertion. However, we examined this proposition in our last blog, and found no evidence to support it for the system as a whole. Quite the opposite, a simple gilt investment did better. https://henrytapper.com/2023/02/06/ldi-investment-or-speculation-keating-and-clacher/

We are also far from convinced that the crisis costs are as little as the £3 billion quoted. We think that the true cost is orders of magnitude higher.

If the USS can lose 20% of asset value in the period under consideration, then the impact is even greater than the £500bn educated guess

The decline in assets, which started the year around £1,820 billion – the various estimates of that figure differ by only about £15 billion. A 20% decline would be £364 billion not even greater than our £500 billion estimate.

Your own educated guesses (it was £400m yesterday) seem to assume no net investment between December 2021 and October 2022.

Perhaps there was “good money after bad” which would increase the level of losses? But that’s simply an uneducated guess on my part.

That is a possibility. We should be able to disentangle these elements once we get the ONS figures as at September 30 (late March) typically though these contributions have been quite small in recent times – around £4 billion per quarter. We now actually think the decline will be in the £500 billion to £600 billion range from that beginning of year £1,800 billion. The use of non LDI assets to meet calls on LDI strategies will be captured by the asset valuation – and we get to see what was made by way of contributions (ordinary and special) – the amounts paid as pensions and the investment income are also there.