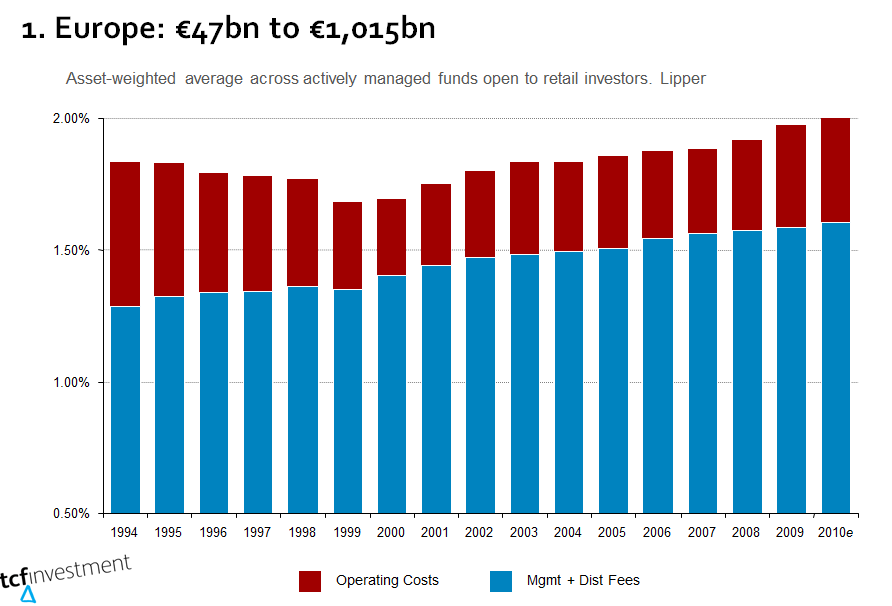

Take a look at this chart provided me yesterday by the excellent Dan Norman

This is what it says

- The percentage of your funds used to provide management and distribution fees by fund managers rose between 1994 and 2010 from 1.3 to 1.5%.

- Although operating costs fell between 1994 and 2000, they have risen against since then and are now climbing back to 1994 levels

- Put together, these fees now reduce the average fund by 2% per year

- With funds growing from €47bn to €1,105 bn over the period, the increase in nominal returns to fund managers has been staggering

- In a low inflation/low growth environment where the total gross return can’t be expected to exceed 6%, fees now take in excess of 30% of the total return.

Regular readers of this blog will know that an actively traded equity fund that doesn’t pay much attention to operating costs can easily run up three times the operating costs quoted by Lipper (above).

We have seen funds where the management and distribution costs exceed 1.5% and incur operating costs which together mean 3% pa is lost from the return. Now half the return is now lost to charges.

Dan likes to quote the Economist

“Imagine a business in which other people hand you their money to look after and pay you handsomely for doing so. Even better, your fees go up every year, even if you are hopeless at the job.”

And this is the way the money goes! Thanks again to Dan and TCF investments.

Well that’s the kind of small print I actually wanted to read.

So while the rest of western industry has been using new technology to cut costs and taking wage and bonus cuts, the financial services has seen operating costs maintained at 1994 levels, management and distribution charges shooting through the roof and the regulators standing by wringing their hands.

Fortunately things are changing. When hedge fund managers can offer a no-win no-fee service to pension funds based on them taking 50% of the funds costs out, you know that the fat has got to ridiculous proportions. The ABI have said it and now the IMA – under Daniel Godfrey is saying it.

The fund management industry has to exercise its fiduciary duty to treat its customers fairly

And that goes for platform and advisory fees from the so-called vertically integrated advisers too. From Hargreaves Lansdowne to Mercer, advisers who take their profits implicitly from assets under their control are going to have shape up.

Gregg McClymont has been quite explicit. It is now Labour Party Policy that if the fund and platform managers do not put their houses in order, a new Labour Government will.

Brave people like Dan Norman, David Pitt-Watson, Terry Smith, Alan Miller, Emmy Labovitch Con Keating (and many more) have extricated themselves from the conflicts of working within the funds industry and we are now finding out what we suspected all along.

Those swanky City offices , fancy cars and fancy salaries, those corporate boxes at Wimbledon and Twickenham were not paid for from thin air. The ridiculous excesses of the fund management industry that are still going strong, have to stop. Operational costs must be declared and reduced. Distribution fees and management charges need to be curbed.

For too long , those who have lived off the fat – the journalists and the trade bodies have stood on the sidelines. Now ,at last, organisations like the NAPF are joining in. A few journalists are being brave enough to bite the hands that fed their sales and marketing teams.

Most of all, those charged with fiduciary responsibilities, including the managers themselves must, as Dan puts it “put themselves in their customers shoes” and start treating them fairly,

Take Our PollRelated articles

- Is this what your savings are paying for? (henrytapper.com)

- No win no fee – one way to clean up asset management (henrytapper.com)

- Who’s been sleeping in my bed? Shocking stuff on stock lending. (henrytapper.com)

- The dam is full – manage the sluices (henrytapper.com)

- Five ways to cut the cost of investing (telegraph.co.uk)

- Isa investing: Why more funds will meet my golden rule (telegraph.co.uk)

- DC4Good; ABdc and the Pension Trust get it. (henrytapper.com)

- Diagnosing the real cost of DC (henrytapper.com)