The Phoenix IGC has had a good year and its 40 page report shows how a well chaired, well funded IGC can produce a document that is both authoritative and readable.

Congratulations to its chair – David Hare – who will become the chair of the combined IGC for Phoenix and Standard Life (now owned by Phoenix) from June of this year.

Over its four reports Phoenix has consistently upheld the purpose of IGCs – it has shown itself to be solely for policyholders and has not sought to puff up its paymasters or play to the regulator. It has incorporated already the policyholders of Abbey Life and we expect next year that the Phoenix IGC will become one of the most important IGCs out there.

This year’s report.

Tone

As with previous years -this report is clearly written and looks the work of one hand – it is consistent in tone and full of personal conviction. So it reads like a long letter, rather than a corporate report.

Sometimes the frustration of the IGC can be heard; but the even-temper suggests that the conversation between IGC and provider is both firm and amicable. Take this example from the transactions costs section of the report

We knew that Phoenix needed to get the information from its investment

managers and that it has been pressing to receive it. We also expected it to take

some time to get all of the information because Phoenix and its fund managers

had to put in new processes to collect and report it to us. Finally we know that

a number of other companies reliant on receiving information from investment

managers are in a similar position to Phoenix, but we will be looking for

significant improvements during 2019.

That leaves those doing the investment reporting on a final warning. This is precisely how to operate and communicate effectively. The message outbound – to policyholders is the message inbound (to Phoenix and its fund managers).

This is a very well written report and I give it a green for its tone

Value for Money reporting

Phoenix IGC has landed on a balanced scorecard approach which marks reports out of 110. This year Phoenix got a 92% score which is reflected in the red orange and green ratings.

I like the methodology (it is the same approach as used by pension playpen) and I like the transparency of approach that allows us to follow how that 92% emerged.

As regards the key issues that drive member outcomes, the report is thorough. It properly demonstrates the range of returns from the various life company pension unit linked fund defaults it covers

And it compares them with the returns from with-profits funds.

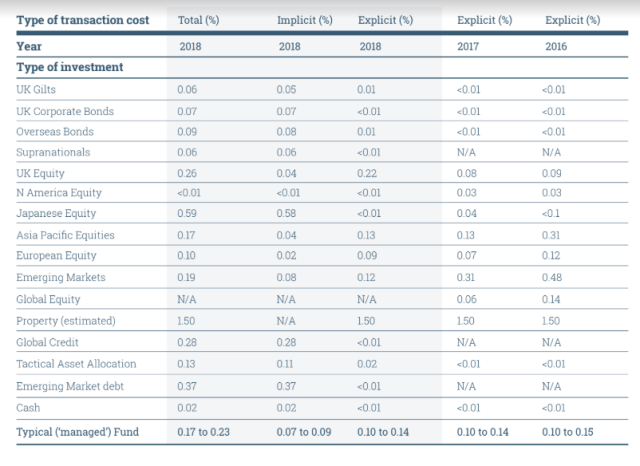

When it comes to transaction costs, the subject is dealt with expertly and firmly (see quote above)

This is the most comprehensive reporting on transaction costs I have yet seen. Despite information being incomplete, the IGC has gone a very long way to helping me understand where extra costs are being incurred and this table should be read by all investment consultants and referred to in recommendations.

In case the reader is in any doubt, the IGC follows up by showing how such costs impact on fund returns

I am happy with the way that Phoenix’s IGC is conducting its value for money reporting and give it a green

How effective?

Generally, the IGC is showing it’s getting its way in fighting for members. It is proud that it’s got Phoenix to drop exit penalties on small pots (<£5000) for people over 55. The report is on the ball with regards Phoenix’s at retirement options and there is much to like about the efforts Phoenix are making to help their customers spend their money with them or pass customer on to Hub Financial Services (part of Just group).

The report is sensitive to the work done by Phoenix on vulnerable customers and commends Phoenix for its work stopping scammers (£30m since 2013)

If I have a problem, it is with the benchmarks that are used. This is particularly the case in terms of transfers. Not everyone takes as rosy a view of Phoenix’s services as the IGC. Pension Bee’s Robin Hood Rating for Phoenix’s transfers does not match the IGCs.

Phoenix picked up two unwanted Robin Hood awards last year – they were voted worst provider for exit fees and won a special award for one exit fee that was 96% of the pot!

My concern (or Amber as the report would have it) is that VFM reporting is too selective and does not focus on the areas where Phoenix are still weak. Transfer values for the under 55s can be terrible and there is a cliff edge between those who keep their policies to 55 and those who don’t.

It’s also worrying that Phoenix’s complaints include these two

In response to a call from a customer that they wished to take their money out of their pension pot, the call handler failed to advise the customer to fill in a risk assessment questionnaire, which resulted in a delay.

The customer was looking to encash their pension, but there was a delay of seven weeks in notifying the customer that the claim form was incomplete, resulting in a delay in the customer receiving their money

Mistakes happen and it’s good that the report picks up on these bloopers, but what is worrying is that customers wanting their money back have to complete a risk assessment and are still filling in paper forms (digital claims cannot be left incomplete).

Behind the curve on ESG

The report is a little deferential to Phoenix’s work on ESG.

We consider that Phoenix’s approach to Environmental, Social and

Governance matters continues to be of a high standard and are pleased

that the investment managers used by Phoenix are required to follow this.

This doesn’t sound very engaged to me and I am not convinced that the IGC has really got responsible investing yet. Certainly Share Action’s reporting on Phoenix does not suggest that the IGC should be quite this sanguine.

The IGC weren’t happy last year that I thought them less effective than they could have been. I am afraid that overall I am going to give them a half green and half amber rating this year.

Part of the problem with being an IGC is you aren’t going to please all of the people all of the time and in my view, the IGC have pulled one or two punches!

In conclusion

Phoenix’s IGC’s report is not just the first, but it’s likely to be one of the best. This is important as next year Phoenix IGC will be reporting on Standard Life as well.

The numbers of people in Phoenix workplace pensions is quite small (100,000) and is decreasing). Only 8,000 pay into workplace pensions. But the IGC report is really helpful in understanding Phoenix’s behaviour to its much larger group of non workplace customers, people who signed up for personal pensions with a wide variety of providers.

It is really good that this report is so well written, so thorough and pretty effective.

How many will read it? I don’t know. I have it in PDF downloadable from the IGC’s (excellent) home page. The link is here

If I had a suggestion for David Hare and the team he builds from June, it is to find ways to get this report to all Phoenix policyholders and to do that digitally.

This report deserves to be read. It may be solely for policyholders – but bystanders like me can get a lot from it too.

Pingback: This new year – let’s know what pensions cost. | The Vision of the Pension Playpen