We should be grateful to Nathan Long and Hargreaves Lansdown for continuing to research what’s actually happening with the self-employed. It’s long been remarked that there are many types of self-employment ranging from the professional partnerships to those just getting by in the gig economy.

Their findings are interested and quite different from what I had expected. Rather than lobby for greater incentives to save into pensions, their report calls for an improvement in the lifetime ISA rules to make the Lifetime ISA , the retirement savings vehicle of choice, for those wary of personal pensions.

The logic behind this is that self-employed people lack the liquidity to tie up money in pensions, they need their retirement savings as a last resort financing vehicle as they go along. This hand to mouth approach may not play with pension purists, but Hargreaves Lansdown reckon that “access” trumps the fiscal advantages of tying money up.

High quality research

The research on financial resilience among the self-employed , is of a very high standard. Oxford Economics research the problem at a household rather than an individual level ( a much better way of thinking about personal financing).

They conclude that the self-employed are increasingly older workers, something that is counter-intuitive as we think of them as gig workers flying the streets on electric bikes.

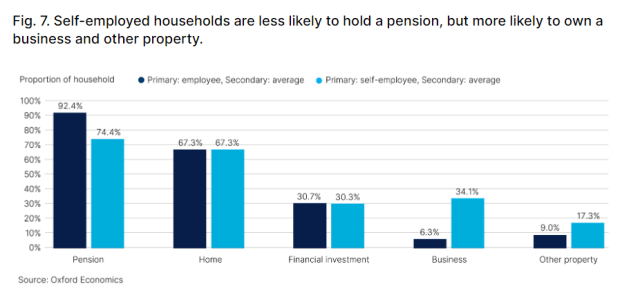

Most self-employed live in households where other household member(s) are employed. This is an important insight, the support of the employed member may be in retirement where the self-employed is dependent, but is this recognised, the numbers beg questions about whether such future dependencies are recognised

The split between employed and self-employed has pronounced implications for household incomes while work is going on

but using the Oxford measure of economics, the more reliant households are on self-employed earnings, the less resilient they are to financial shocks.

The workplace pension (and benefits) overlooked and undervalued?

As you’d expect, the self-employed are more likely to want to invest and make their money work for them, but in all other respects they show less financial gumption. In terms of putting money aside for themselves and their families they are generally feckless and (to a household) a financial menace.

They do have agility in how they create income in retirement

But these strategies aren’t very good at providing liquid cash (you can’t buy a sausage with a brick)

So the self-employed typically fall behind when it comes to financial security in later life

They miss out on the two big ticket items and too often find themselves renting on too small an income – when they retire.

The report goes on to show that most self-employed are basic rate tax-payers who do not get the fiscal advantage of pension savers available to higher rate tax payers. The report suggests that what spare cash that could be saved, would be better saved in Lifetime ISAs than pensions but it also points out that lifetime ISAs aren’t available to the ageing self-employed ( fig 1 whos there are many of them).

Hargreaves conclusion is counter-intuitive but important. It argues that the lifetime self-employed show different behaviours to employed people and need their own targeted savings products that meet their entrepreneurial needs. They have the money to save.

Hargreaves Lansdown’s call to action is to the Treasury. It is simple and logical and in the absence of any meaningful work from the DWP on self-employed pensions, these recommendations are a step in the right direction. Hargreaves Lansdown suggests;-

- Increasing the age that anyone can open and pay into a LISA until age 55.

- Reduce the penalty for any self-employed LISA holders accessing before age 60 to 20%. This acts to recover the government bonus but ensures those needing to withdraw early are not additionally penalised.