ReAssure, after a short delay, have published their 2019/20 IGC report which you can read here

It’s a betwixt and between document as at the time of publication, ReAssure is in the process of being acquired by Phoenix and in the process of acquiring a substantial legacy book of business from Legal and General. The workplace pension book of Old Mutual is being acquired from Old Mutual and we understand that ReAssure’s IGC will assume responsibility for both books. That – and the backdrop of the global pandemic has clearly made publication difficult.

Tone and structure

The report sets out to engage members and bemoans the lack of engagement between ReAssure and its customers. But it’s hard to see how the IGCs call to action will excite policyholders

In your annual pension statement you will find information from me, regarding the new low-cost funds and alternative product options ReAssure have made available. We strongly encourage you to engage with these communications. By taking action you can reduce your charges to as low as 0.65% p.a.

The trouble is that “0.65% pa” has little to excite the ReAssure customer, who most probably took out a policy with Crown Life, Windsor Life, General Portfolio or Alico many years ago and did so because of a financial salesman’s effective salesmanship.

Frankly, customers who entered into contracts with these companies are unlikely to have a high degree of financial literacy and will need a little more to excite them than what’s on show in this report.

Take as an example David. David is 61 and wants to retire at 75.

Take as an example David. David is 61 and wants to retire at 75.

I do not know anyone who at age 61 wants to retire at 75.

David is an actuarially made up person who serves to show that over 14 years he can save £2,700 by avoiding charges in his Crown Director’s Investment Programme.

How can ReAssure or its IGC expect people to engage with Dave’s aspirations – when ReAssure choose a freak to engage with?

If Dave is an example of someone who’d pay less money, John is someone put forward as getting “value”.

The problem for the 48 year old John is reading a graph which makes no sense at all. It purports to show the Global Equity Index Tracker 2019 Performance and in case you were wondering what those tiny numbers at the bottom of the chart are, here’s a blow up

![]()

John’s £1,000 has gone up to £1,571.17 (net of investment fees), but John is probably invested in something like the Crown Director’s Investment Program where the investment fees are supplemented by all kind of other charges. So John’s £1,571,17 could be substantially less. And the big reveal that John has got 9.46% interest each year is so meaningless that – were this to be considered a financial promotion – it would get the compliance office fired.

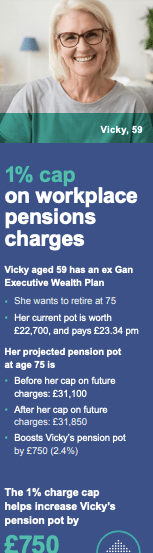

Finally, let’s look at Vicky, she may be married to David because she is the other person I have ever encountered who is in her fifties and planning on retiring at 75.

The whole report is suffused with this kind of actuarially inspired nonsense. Spurious accuracy in numbers, spurious intentions and spurious people. Frankly this is the old mutton dressed up as lamb.

So when we come to read of the IGCs disappointment in its policyholder’s failure to pick up on these offers – we can only shake our heads in despair.We remain disappointed that response rates to the lower-cost fund options have remained low. ReAssure have made contact with a small sample of members who were sent our targeted communications. This verified these had been received and helped us and ReAssure to review and refine messaging.

With messaging like the examples above, the failure is not the policyholder’s but ReAssure’s and ultimately the IGCs.

The tone and structure of the Chair’s Statement looks good , but it isn’t – it’s actually pretty rubbish. I thoroughly agree with the IGCs determination to encourage people to seek value, but the messaging has to be effective and this isn’t. I give the report an amber for its tone, it sets out to encourage engagement, but repelled me as soon as I did engage.

Effectiveness

The moves made by ReAssure to reduce charges to 0.65% pa (despite their mis-promotion) are good news for policy holders. But to stay with ReAssure , policyholders need more than the same old same old. What they are being offered is ReAssure Now, which is a mobile application that includes a host of features which sound like cars with safety builds and steering wheels included.

If you are one of the lucky ones whose policy can be accessed on ReAssure Now then you will be able to

View your policy information – current values, payments in and details of any cover provided.

• View projected values at retirement.

• Access letters and documents in an electronic format.

• Get in touch with ReAssure by secure message.

• Review personal information, and let ReAssure know if you need to make changes.

But if aren’t so lucky , you can register your interest on http://www.reassure.co.uk/interested which will click you through to

Frankly, the incompetence and antediluvian nature of the functionality on offer in the report suggests to me that ReAssureNow is no more than window-dressing to assuage the understandable annoyance of savers whose hopes of a decent workplace pension took a knock when HSBC Life was consigned to “legacy” a couple of years after opening.

Effective engagement does not look like this and if the promotion of ReAssure as an engaging organisation is based on my experience of ReAssureNow, I’m out. I give the report an amber but did enjoy Venetia Trayhurn’s account of her day out in Telford (p12).

Value for Money Assessment

If you’ve got this far, you won’t be surprised that I didn’t think much of the 83% rating the IGC gave ReAssure as a VFM score.

The combination of good service, comparative returns, reasonable charges and customer choice, have delivered Value for Money. Where challenge has been raised, ReAssure have committed to actions. The IGC would like to see greater levels of customer engagement with their pension, and will continue to work with ReAssure to see what more can be done to help customers.

My scepticism is based on my loss of confidence in the report’s tone and my scepticism following my investigation of ReassureNow.

The investment section of the report indicates a lack of strenuous thought about how ordinary people live their lives

Your Annual Statement details the funds that you have selected to invest in. If this is not one of the 5 funds listed below, you can view all funds on the Reassure fund centre: http://www.reassure.co.uk/fundcentre.

This shows current fund prices, investment objectives, past performance data and information about charges.

Because ReAssure workplace pensions don’t offer defaults, policyholders need direction and , in the absence of advice, investment pathways.

At some length, the report talks about the investment pathway process to be monitored by the IGCs next year. These are default pathways – for those who don’t take advice. So why isn’t ReAssure doing the same for savers?

The 5.5/6 score for investments simply doesn’t stack up. Hanging this rating on this statement is simply not good enough – in keeping with much of the rest of the report , it simply doesn’t engage with how ordinary people think about value.

When comparing the funds to their ABI sectors, 69.35% of the funds (or 76.3% of the IGC assets under management) have outperformed their respective ABI sectors throughout 2019, meaning that the rest of the market faced returns that were more negative.

Actually what ordinary people tell IGCs they are concerned about is what comes out of their pensions compared with what goes in. Simply throwing percentages at the problem is not going to solve it. People want to know how they have done and how they’ve done relative to others.

This report does nothing to help them in this, indeed it so befuddles its readers that they are likely to leave it less – rather than more -engaged. The Value for Money assessment for ReAssure is the worst I’ve read this year and I give it a red.