Richard Butcher – Chair of the IGC

Last year I gave Old Mutual’s IGC Chair Statement the thumbs down .

This year’s statement is a great improvement. It will be the last from Old Mutual as the book of business looked after by Richard Butcher, Ian Costain, Mark Latimour, Jon Greer and Antony Scammell will be passed to ReAssure.

ReAssure are themselves likely to be consolidated into Phoenix this year – so the book may pass down from scrum half to wing in a matter of months.

I’m pleased that this report is so much better and that the Old Mutual IGC has got its pass away accurately and timely .

Tone , structure and effectiveness

Richard Butcher’s style is straight to the point. He sees his Chair Statement as a call to action to his policyholders. Just how many of the old Skandia Life policyholders will be reading an Old Mutual IGC report is open to question, but there’s no doubting the message. I counted 9 calls to action (as well as a call to contact the ReAssure IGC as part of the handover).

On suitability

On value for money

On being “invested” in cash

On whether you should be in the default

On whether you are in the right Lifestyle strategy

On being entitled to a rebate in charges

On having a “small” pot

On paying unnecessary adviser fees

On scams

On all these matters , the report establishes the right tone and is being most effective. Indeed this is one of the best structured reports I have read.

I very much hope that Old Mutual make a real effort to get the report into the hands of savers because most of these savers need either advice or strong guidance .

I give the report a green for its tone and a green for being effective

Value for money assessment

In previous reports, I have criticised the IGC for producing VFM assessments that were not properly rigorous. The Skandia book of business was priced with little thought for value for the policyholder’s money.

Belatedly, the IGC are now recognising that neither the investment options themselves, nor the charging structure of the contracts – are offering much by way of value for money.

Frankly, I’d go further and would leave a legacy of orange and red – but this is certainly a more realistic assessment than those of previous years.

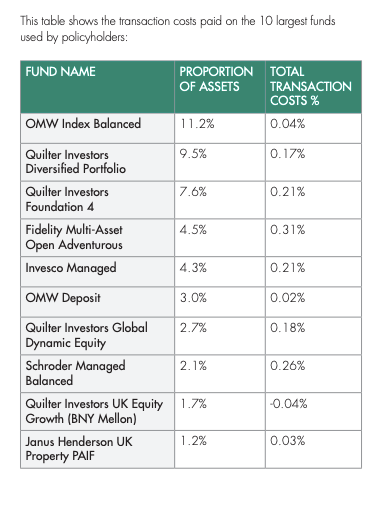

Indicative of just how little attention is being paid to the costs savers are baring is detailed in the breakdown of transaction costs for the core funds savers are using

Richard Butcher knows what good looks like and some of these numbers are too high. Many of the workplace pensions set up by advisers with bespoke defaults are no longer fit for purpose, the book is now in a pretty ropey state and we hope that ReAssure and ultimately Phoenix will turn things round for policyholders.

Though there is clearly a proper level of service being delivered to policyholders (I phoned the helpline this morning and it is open for full office hours – a slightly reduced service), I don’t think that this book of business represents value for money – certainly compared to other workplace pensions.

Skandia and then Old Mutual, have never tried to offer policies within the Auto-Enrolment cap, they never operated stakeholder pensions for the same reason. While the charging structures and investment funds offered within this book may work for wealth managers (who can exert a high degree of control) most policies in this book are now unadvised and languish.

So I really can’t accept the overall estimation of the IGC

Our overall conclusion is that a majority of you get value for money from your Old Mutual Wealth workplace personal pension and that, on average, the value policyholders get has improved. The value you get, however, depends, in part, on you.

As I said last year, it’s not down to policyholder’s to create the value, most have paid advisers from within their funds for the work they are now being told to do themselves. When you’ve paid for fitting , it’s tough to be told the service is DIY.

Where we have concerns about policyholders potentially not receiving value for money, it is generally because a policyholder is not actively engaged in managing their pension and/or an adviser managing their scheme is no longer actively engaged in doing so.

The “it’s not our fault- guv” plea does not wash on this commentator. The VFM assessment gets an amber with a splash or red.