The Scottish Widows IGC

Anna Bradley is back as Scottish Widows IGC chair and she couldn’t have chosen a worse time to get the job. She’s reporting on 2022, a year when not only was the performance of Scottish Widow’s workplace pension funds and investment pathways awful, but so was the service it gave its customer.

Anna Bradley is a fierce consumerist who will side with the saver over the consumer. She has nearly got her old job back, as much of her work is on the old Zurich workplace pension which Scottish Widows took over in 2017 and have made a bit of a mess of. Scottish Widows have made a hash of almost all its pension book and she has to politely tell them (and their savers) just that.

I think she has done a remarkable job in producing a report that is an enjoyable and interesting read, that doesn’t hide from the problems but offers a way forward. The policyholders she is writing to deserve this report.

The Scottish Widows Complaint Forum

I visited the Scottish Widows Complaint Forum on Facebook. I doubt any of its 1117 members consider Scottish Widows is giving them value for money and the steady stream of media attention to the (lack of) service customers are getting , suggests they are right.

Scottish Widows know they have a problem and monitor the site – putting out fires as they can and knowing full well that the membership includes journalists from several major newspapers. It is in this context that Anne Bradley has to deliver the news that

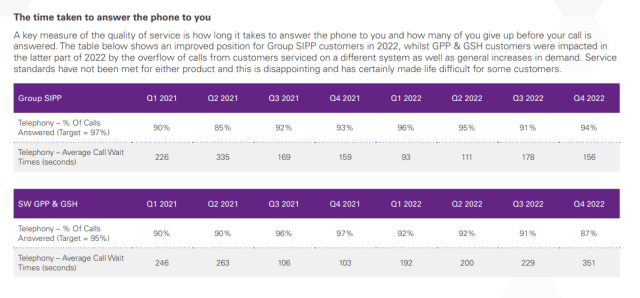

The IGC recognises an improvement in service quality over

the last two years. However, in late 2022 the telephone

service was affected by an overflow of calls from customers

with modern style products serviced on a different system as

well as general increases in demand. Some customers of

modern style products have been affected by this, but in

relatively small numbers.There is a programme in place to improve performance and we are monitoring it closely. The IGC would like to see more consistency and stability in service levels across products, along with reassurance that the service standards compare well with other companies and meet customer expectations.

An additional problem for Bradley is that she is publishing this report ten months after the period it is reporting on. Much of what she wants to happen – is happening – but you cannot report on that till 2024. The timeframes of those complaining is “days” not “years”.

At the heart of the service problem that Widows and its IGC face is that customers are less prepared to manage their pensions themselves, not prepared to use chatbots but want help on the phone. This is particularly the case when it comes to accessing their pots to pay bills, something frowned on by many in pensions. They call Scottish Widows on the telephone and by the end of last year were waiting between 3 and 6 minutes depending on whether they were in “modern or older” policies.

These are unacceptable waiting times for a world class financial services company but they are what happens when you swallow your kool aid. Scottish Widows is about digital communications, dashboards and apps, these have been developed but it looks like the help ordinary people need to do simple things, like get their money out, has been downgraded.

The Scottish Widows complaint resonates with complaints about simple things going wrong. These are the three most recent posts

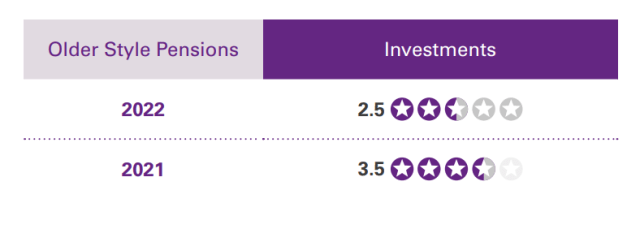

Under the marking system established by Bradley, “modern style” workplace pensions get the following ratings

The 3* service rating means the IGC thinks service “Provides the same VfM as most

competitors”. Older style pensions are marked worse

The 2* service means the IGC thinks Scottish Widows “Needs to improve VfM in some areas to match competitors”.

The 2* service means the IGC thinks Scottish Widows “Needs to improve VfM in some areas to match competitors”.

It is not unusual for large organisations to get service wrong, it is unusual for large organisations to have Anna Bradley and a very strong committee , there to put things right. The problem is recognised to a degree but knowing Bradley as I do, she will be as shocked by the reports coming from policyholders as everyone else.

The Scottish Widows investment problem

The issues identified with service might be more manageable if matters hadn’t gone awry on investments.

In 2022, Scottish Widows revamped default fund went badly wrong. The problems were put down to the fund being over-invested in UK stock markets, bets taken on currency went wrong and there seems to have been little gong right to compensate

The IGC again looks to what’s happened in 2023 to sugar-coat the message but the message is not good. There has been little value add from being with Scottish Widows in terms of investment returns

And a loss of value from being in older pensions

The VFM scores take into account more than just what happened last year – they smooth out the lows with the highs, but the message is clear enough, Scottish Widows are struggling to be seen as more than average.

It is only when you dive into the weeds of the report that you find just how badly things went wrong for policyholders. These are the numbers for the “modern” policies, the ones considered “average”

Even giving the funds a 55 bp head start on charges (why?) , last year’s performance was well over 3% down on Widows peers. You have to go back before the revamp of funds to see much value being created.

Theis fund aims to beat inflation. The flagship investment fund in the Scottish Widows range failed to meet its inflation target (CPI +3%) and fell short by a staggering 25%, that means that if you add inflation +3% and compare it with what actually happened, the fund lost 25% of its value in a year.

But that is not all. Moving on to the investment pathways , things are even worse. Scottish Widows took a view that to preserve people’s cash, they would invest for the short terms in shares. This resulted in the cash preservation fund falling 13.9% in a year (investment pathway 4). Cash would have provided around 4% positive.

But Investment pathway 2 takes the (dog) biscuit). It lost savers about to buy an annuity 35% in a year. This (unlike the cash disaster) is explained away – I suspect by the Scottish Widows investment team as the language is rather more technical than the rest of the report

This fund is mainly invested in Government bonds and the price of these bonds has a significant impact on the price of buying an

annuity or guaranteed income. So although there was a sharp fall in the value of Government bonds in 2022, buying an annuity became cheaper. This meant that whilst customers invested in this pathway saw the total value of their investment fall, the level of income of annuity they could buy was broadly unchanged.

The fact is , that had these pathways been in cash, savers would have been between 17% and 40% better off.

There is little better news for those who stayed invested, they lost more in PP4 than if they’d stayed in PP2 but again they had a less onerous target. And again all these scores are calculated using a 0.1% investment charge.

We are told that

Scottish Widows remain comfortable with its approach, but it is

planning to review the investment approach for each of the four

investment pathways to make sure it is delivering what is needed. This work will be finished in the second half of 2023, and we look forward to reviewing any proposals that might follow

The IGC may feel the work could not be concluded a moment too soon.

Scottish Widows charges

You might have thought from reading the investment section, that Scottish Widows customers pay 0.1% of the value of their fund in charges. They don’t. Helpfully, the IGC break down the charges by the deals negotiated by Scottish Widows by participating employers in their GPP GSIPP and the GSP (Group Stakeholder Plan)

The charges paid are of course much higher. However they are lower than the average workplace pension provider and I won’t quibble with the 4* rating given modern charging structures, in troth – the older policies do well to offer 3* VFM. Compared with their peers, Scottish Widows is charging a little less. But it is not charging 0.1% ( I will be writing to Anna Bradley to understand why the 0.1% investment charge is used.

My assessment of the Scottish Widows 2023 IGC report

I have focussed on the Value for Money assessment carried out by the IGC. I think that it broadly sets out what happened in 2022 and suggests what policyholders probably know, that 2022 was an “annus horribilis” for investment and charges. No doubt progress was made in communications and ESG but these aren’t key areas for VFM assessments (important as they are). It is a horrible job to bear bad news to policyholders and to do so in a way that does not inflame an already difficult position. I think the report does ok and I give the VFM assessment an amber – frankly, taking 2022 in isolation, investment * ratings should have been on the floor with service not far behind.

In terms of effectiveness, I don’t suppose for a minute that Anne Bradley is complacent that Scottish Widows will put things right on their own. The report is always straining to tell us of progress in 2023 and I hope there is. We will have to wait till next year to hear how much. But I sense that Bradley is making a difference and I will give the IGC a green for intent and effectiveness

The best of the report is the way it sets out to engage the readers. The report carries a glossary for residual jargon , but for the most part – it is not needed. The style of the report is approachable, at some time almost folksy. The report is well laid out and thankfully free of pictures proving the IGC and provider know what Diversity and Inclusion is. I liked reading it and give it a green for tone and content.

I hope that the Facebook Complaint Forum read the report and comment on it to the IGC, who ask for feedback to be sent to

Mailbox. contacttheigc@scottishwidows.co.uk

This just confirms that Scottish widows is not fir for purpose .. whilst other pension providers have investment managers who have been proactive in changing strategies to counter the challenges of the last three years, SW has changed NOTHING which has cost people thousands of pounds … We pay for our pensions to be managed in responsible way however returns prove SW/Lloyd’s now treat customers as cash cows ..