A different way to think about CDC

The ABI should be feeling pretty pleased with itself. Last week, its Director of Policy, Yvonne Braun, told the Work and Pensions committee that it seen off the consolidators. As a result, its members can now choose which overfunded DB scheme to pick off next without let and hindrance.

Now it’s gunning for CDC, commissioning a report from Milliman and Barnett Waddingham designed to muddy the waters and create the kind of confusion in the market that ensures that the hapless saver is denied a pension and gets a spaghetti junction of investment pathways instead.

The ABI are sending its report to Laura Trott and the DWP. Trott should take comfort that this attempt to maintain an unsatisfactory status quo, has been a damp squib.

The Times tows the ABI’s line

The ABI sent me the report and accompanying press release – pointing me to an article in the Times. It was supposed to be an explosive placement, but no other publication gave the ABI’s press release the time of day yesterday – not even the pension trade press.

Patrick Hosking in the Times did his bit. He seemed only too happy to tow the ABI’s line.

New breed of collective pensions offer benefits ‘at much lower level’

Claims about the benefits of a new breed of pension scheme proposed by the government are exaggerated and may not exist at all in some cases, a report has suggested.

Those in the firing line for exaggerating and making things up include the Government Actuary, Aon, WTW and the DWP itself. Casting doubt on their integrity needs more than what’s delivered by the ABI’s commissioned research.

CDC is a pension for the silent majority not a pathway for the well to do.

I shared the report with some of my colleagues, others were sent it by the ABI – feedback was immediate.

Here is a comment on the report from a former adviser to Steve Webb and Ros Altmann, a man who has spent fifty years in pensions , ensuring that ordinary people are well served

My beef is (again) that insurer’s ideas of drawdown for their market are not what low-middle income people will opt for in future when all they have is BSP + say £250k. They will derisk massively and many will underspend.

Here is the view of Adrian Boulding, who leads on CDC at the RSA.

“It is very much an actuary’s viewpoint to say that the rates of return are higher for savers who choose drawdown and die in the early years than those who choose CDC because of the return of fund after death. If the calculation instead was based solely on the income received while the member was alive and able to spend it on themselves they would find a higher rate of return for CDC.

“Which tells me that what’s key in deciding which retirement income vehicle is right for you is to determine first what your needs in retirement are. And different needs will drive you to different choices.”

We may have differing needs but we have a common purpose

Tom Mcphail makes the point that we need a clearly defined purpose

Thinking about the triple lock today.

The problem with pensions is the whole system has no defining purpose. A system without a clearly articulated defining purpose trends naturally towards complexity and inefficiency.

Can I call this ‘McPhail’s first law of pensions’?— Tom McPhail (@PensionsMonkey) September 12, 2023

I agree with Tom that a defining purpose is needed. But there is a plan behind our pension system and the Mansion House Reforms part of it. It is a simple plan based around consolidation, value for money and the delivery of pensions not “pension pots”.

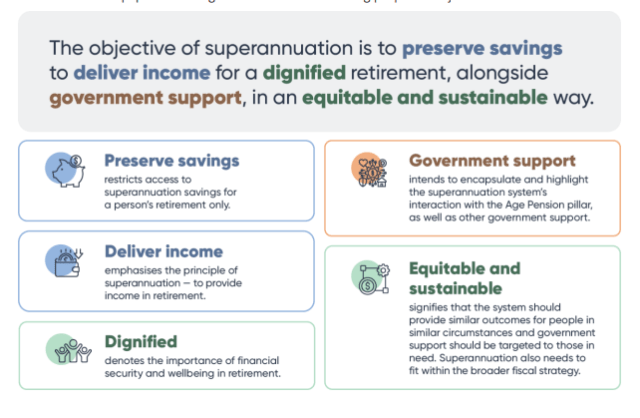

The needs of most people are well articulated by the Australian Treasury’s objective for its superannuation system.

We share a common purpose with Australian savers, we are all looking to solve the nastiest hardest problem in finance.

CDC makes pensions out of workplace pensions and brings DB and DC together in a way that people can understand. CDC makes sense of pensions. Multiple pathways get people lost.

The ABI would make financial advisers of us all

What follows is from the ABI’s press release that accompanied the paper. It conveniently forgets that for decades , the only option that a trustee could put to a member was an annuity. I can’t remember the insurers complaining about that.

While there could be a place for CDCs in the market, they’re not going to work for everyone. No one can predict how long an individual may live, or the returns someone might get on their investment. And it’s not realistic to put one number on just how much CDCs could deliver for savers when there are so many variables and unknowns.

In some scenarios, CDCs could perform better – for example, for those who live longer. However, individual defined contribution and income drawdown or annuities could result in better outcomes for others. That’s why DWP’s decumulation policy needs to include a duty for pension schemes to offer their members a range of options to achieve a sustainable income.

The behavioural trope employed by the ABI plays on our fear of change. CDC is not just characterised as “new” but “variable” and “unknown”. Compared with the annuity or income drawdown options that a generation of DC savers has grown up with, CDC has to struggle to find its place in the market – like superfunds and DB master trusts and the other products that the ABI and its membership cannot control.

The ABI would have us choose our investment pathway into retirement like a magazine off a newsagent’s shelf. In this analogy CDC would be on the top shelf and sealed in a cellophane bag.

The ABI is but a short step from requiring CDC to be a regulated product only purchased with financial advice. Pensions should not be so complicated, choices should not need us to become financial experts. Many of us struggle with percentages and need things to be done for us.

What has the ABI got against CDC?

The aversion to CDC which is so obvious from the ABI’s press release, manifests itself in a strange wealth warning

We warn that Government predictions for Collective Defined Contribution (CDC) pensions give an incomplete picture of potential returns, given the diversity across members and the financial conditions they experience.

Insurers have for centuries offered annuities on a one size fits all basis. Their current business is buying out DB plans without any knowledge of the millions of pensioners who rely on them for a wage for life.

It is even stranger because the Milliman Barnett Waddingham report suggests that the insurance industry is well placed to deliver collective pensions for the DC potholder.

Insurers are well placed to offer CDC, with insurers being capable of providing both trust based and contract-based schemes. This experience and knowledge extends beyond the accumulation stage of DC pensions. Insurers have been delivering decumulation products and solutions to both the corporate and individual markets for many years, and one may argue that retirement income sits more naturally with insurers than with a (then-former) employer.

We can only guess at why insurers dislike CDC, but they do. They promote bulk annuities as collective solutions when it suits them , but require savers to take personal decisions about later life which are often beyond them.

The Milliman modelling

Now let’s turn to the justification for the ABI’s warnings.

There is considerable modelling within the report. It starts by reviewing what it calls historical claims for CDC. These claims show that CDC is likely to deliver between 25% (GAD) and 70% (WTW) outcomes than annuities. The DWP reckon that CDC would on average produce 22% better returns than were people left to follow individual strategies.

There is likely to be a lower gap between the annuity and CDC outcome if the model uses today’s annuity rates, (decided by today’s interest rates). The Times’ accusation that previous models exaggerated the benefits of CDC is as ludicrous as the statement that CDC offers lower benefits. The benefits of a CDC plan are not dependent on interest rates, the benefits of an annuity are, the lower the annuity rate the greater the differential between the two but CDC has the fundamental advantage of linking its benefits to the long term returns achievable from investment. It is as Milliman says.

CDC frequently gives better member outcomes than IDC annuitisation, both in terms of average income replacement ratio and rate of return for the member, albeit at a much lower level than the previous studies indicated.

Models are only models, whatever model has been used over a number of years shows that the pooling of investment and mortality risk , combined with a simple and effective means of distributing returns, leads to better overall outcomes.

Milliman reports

The longer a member survives, the greater the differential as CDC’s longer exposure to growth assets drives benefit increases.

This isn’t surprising. CDC carries an upside if assets perform better than expected and a downside if they perform worse than expected. It is always possible than an annuitant will do better than a CDC pensioner.

But now we get to drawdown . The Milliman report states

The drawdown comparison shows a different picture – the return of fund when a member dies means that member rates of return are often higher than for CDC when the member dies at younger ages.

As Adrian points out, this is actuary-talk.The residual value of a CDC or drawdown is of no interest to a person who is dead. A CDC can be set up to pay a residual pension, introducing another variable and the happiness (utility) it brings depends on the emotional support it provides the pensioner and the household.

The Milliman modelling serves only to muddy the waters. This suits the ABI very well and gives the Times a chance to have a go, but ultimately the story is a simple one, graphically explained by Milliman and Barnett Waddingham.

CDC – choice architecture and the default option for spending your pot

The ABI are right in saying that a CDC pension should not be a product entered into through inertia.

A CDC insures against living too long (as annuities do) and there is a price to pay for that insurance. If you know you are going to die young, do not buy an annuity and do not enter into a CDC plan. You do not share the common purpose of the population – you want to leave your retirement savings to your heirs and to have flexibility to spend your pot as you see fit. Choose drawdown.

But that is not why most wealthy people aren’t spending their pension pot. The wealthy avoid crystallising their DC pensions for tax reasons. Absurdly, the taxation system incentivises the wealthy with IHT issues to use their pension pot as mitigation. I cannot think of a single piece of tax legislation so at odds with Government policy as the rules governing the inheritance of DC pots.

As it stands, it is fiscally imprudent for the wealthy to annuitise or even hold a pension. Many rich people have taken CETVs from DB schemes because of IHT advantages.

But the wealthy are few and a CDC plan is for the many. The ABI can rely on the support of the wealth management industry for whom any change in the taxation of pensions wealth would have severe implications. CDC imperils not just flows of money to high margin wealth products (which are often insured) but the precarious status of this regressive tax anomaly.

The ABI are fearful that CDC pensions might become as much a default for the many as annuities were. They say it might become a honeytrap for the financially unaware (as annuities were). They imply that you could find yourself getting paid a CDC pension by accident.

A CDC pension is not however a honeytrap, it is a choice. You can only get paid a pension if you offer your bank details and though it can be the promoted solution , getting paid a CDC pension requires a decision from the pot-holder. Unlike the pre-freedoms system, opt-outs into other pathways are a right not a privilege.

This entirely negates the main thrust of the ABI (and of constituent organisations such as Aegon and Standard Life who argue the same thing). They say that CDC should not be promoted as a default decumulator – “default” is the wrong word. CDC is a natural outcome of a workplace pension and could be promoted as the expected pathway by fiduciaries.

It can and should be promoted with conviction where a fiduciary has the guts to do so. Individuals should know that other options are available to them, but they do not need to explore them. We have to have freedoms from freedoms.

CDC is an investment that insures against living too long. It is a wage for life, if you want a capital reservoir, choose drawdown, if you want guarantees – buy an annuity.

CDC gives pensions a common collective purpose

The concept of a pension as giving dignity to those in retirement by providing a lifetime income has been turned around by the ABI so that we must give priority to those whose retirement situation is so rosy, or life expectancy so short, that they have no need to worry about living too long.

We know that people underestimate their longevity and until we had pension freedoms, the insurance industry reminded us of just that. Now the ABI are basing a nation’s retirement strategy on diversity of needs. It’s refusal to promote CDC as anything more than a minority interest is a mis-statement of CDC’s purpose and a dis-service to ordinary people.

Adrian’s wry comment about actuaries has authenticity, he is a member of that profession. But he can see what the report cannot see, that ordinary people need to maximise income when alive and aren’t that bothered by “residuals”. The person on the Clapham Omnibus has been bamboozled by pension freedoms, this initiative shows the ABI are happy for things to stay that way.

Many moons ago, a former PPF executive (insurer background) told me how much insurers hated DB – you would never ‘write them if you had the choice, that it was a financial anachronism that should be confined to history, and insurers would only take them on if very fully funded with the risks all but eliminated. And so it has come to pass….

UK Regulation this century has been of the insurers, for the insurers. That is wrong, and the mindset must change – it needs to revert to being for the members, in retirement.

The insurers may hate DB as a concept but they love it in practice. Look how many DB insurance staff schemes there are (I’m a pensioner of one myself). They were among the better funded, and before “trapped surpluses” became a thing, they were considered a potential financing vehicle for the sponsor.

Yes, I can understand why management of insurer schemes would ensure their own funds were amongst the better funded.

I am preparing the Accounts for an open DB scheme and I note that over the past 4 years there has only been one elective transfer value paid to a DC arrangement (i.e., ignoring pension splitting on divorce etc.) out of 82 new leavers from active with deferred benefits and and another existing 101 deferred members plus 31 retirements.

To me that seems to suggest the vast majority pension scheme members wish the security of pension income over the freedoms offered by the 2014 Finance Act.

There have also been no auto-enrolment opt-outs.

There could be a number of reasons for this Peter, 1. High discount rates depressing transfer values, 2. Lack of advisers offering advice on transfers 3. Reluctance of members to pay fees upfront (after abolition of conditional charging) 4. Members value their pensions

I thought about those factors. but the 4 year period covered was was 1st April 2019 to 31st March 2013 so for the first 3 years TVs were historically high.

I have no knowledge about the availability of IFA advice on DB transfers except to know that its is difficult to obtain, and the impact of upfront fees. We do provide a transfer value quote as part of our standard “retirement” pack.

I believe members do value their pensions – certainly all the feedback suggests this.

Money purchase AVCs are also offered and used by a significant proportion of “mature” members to provide the tax free lump sum at retirement, leaving the [partially] income protected annual pension intact and this may be part of the reason.

It sounds like they have both a good pension management team and a sensible membership

In a previous report by Milliman in 2017, the insurers said that consumer friendly pensions are “impossible… especially at a low cost”. Impossible for a bloated insurer most certainly.

In this case the ABI won’t ever be happy with CDC’s until they find a way to make it generate comparable profits for themselves as they earn with annuities. At that point, the ABI CDCs will probably be relegated as a sales decoy for promoting annuities.

“Insurers are well placed to offer CDC, with insurers being capable of providing both trust based and contract-based schemes.”

What they don’t realise is that banks (major sellers of insured annuities) are also equally capable of structuring CDCs (or Tontines as we call them) and once the banks wake up to this, regular consumers and you Henry are finally going to have a decent alternative.