Based on the data and analysis in this report, the IGC

concludes that Vanguard is offering good VFM to its

investment pathway investors. We have not discovered

any other provider offering better value.

So concludes the 2022 IGC report from Vanguard’s IGC Chair Lawrence Churchill. This bold claim is based on the following analysis.

In drawing this conclusion, the IGC acknowledges the

stressed market conditions experienced during the

year, which affected all index-fund asset managers.

However, longer term performance continues to deliver

real returns. Vanguard’s cost and charges are also

lower than most competitors while the quality of their

services are at least on a par. Indeed, communications

sent to clients about the challenges they may face when

investing in difficult conditions resonated well and may

have prevented many from making poor decisions and

locking in losses

Vanurad’s IGC was set up in 2020 because Vanguard’s SIPP offers non-advised investment pathways, Vanguard does not offer workplace pensions, to commit to an IGC, rather than the junior GAA, was a statement of intent by Vanguard to go above and beyond. By appointing Laurance Churchill, who had done an outstanding job as IGC Chair for the Prudential, Vanguard showed actions speak louder than words.

This is another excellent report that shows that Vanguard’s savers (and in this case spenders) are in safe hands.

It’s not easy to find the report but you can access it directly via this link. Note that though I am reviewing it in August, Lawrence published the report in July and it is, to my knowledge , the first IGC report to have been posted.

A bigger bus

At the end of 2022, Vanguard had 156 investment pathway clients compared with its

overall UK investor base at the time of over 400,000. In previous years , Churchill has joked that he could get his pathway clients on a London Bus, numbers have grown but they show that self investing customers are not looking for guidance on how to spend their money. At the end of 2021 their were only 65 pathway followers

As the report notes , the DWP decided to exclude investment pathways from the VFM Framework. In its recent report on them, Hymans Robertson found only two providers who had more than 1000 savers spending using them.

While it is fair to say the policy intent is reasonable, the practical application of the policy is currently a failure.

But that does not mean the work of Churchill and his team should be ignored. The numbers using pathways is small but the 400,000 Vanguard savers have much higher than the estimated £30,000 average pot, do they behave differently than other providers’ customers?

So what does the report find out?

Pathway 1: I have no plans to touch my money in the next 5 years.

Pathway 2: I plan to use my money to set up a guaranteed income (annuity) within the next 5 years.

Pawthway 3: I plan to start taking my money as a long term income within the next 5 years.

Pathway 4: I plan to take out all my money within the next 5 years

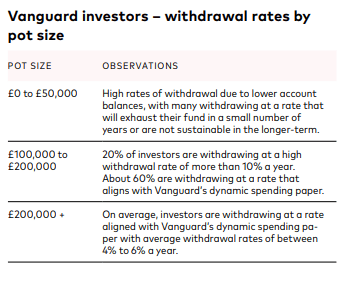

The bigger the pot, the more likely it is to be rolled up, the smaller the pot, the more likely to be cashed out. The majority of people look to their pot to provide them with a long -term income. Sample numbers may be small but they are consistent with wider trends.

Vanguard reports that 60% of these 400,000 savers regularly use its website for fund monitoring purposes. This is well above monitoring by those in workplace pensions. It is interesting to note that despite the quality of communications that the IGC reports on finding from Vantage, that investment pathway take up is so low. We must conclude that either the pathways aren’t suitable for highly aware savers or that pathways aren’t catching on full-stop.

Vanguard against the rest.

The Vanguard IGC includes (as Exhibit 2!) a very limited chart on returns of investment pathways since October 2020 (when they were launched).

I was disappointed to see so few competitor funds being compared. It is hard to make comparisons when fund charges are often subsidised by platform and account fees , so we can’t really compare what those in the various fund options were “getting” , only what the fund managers were showing as their performance.

While I could link some funds to some competitors, some of the choices seemed random, the chart didn’t give an investor much confidence that Vanguard’s TDF product was being fully benchmarked.

I hope that in future years, the IGC will be able to get better actual information on investors achieved returns. This analysis slightly tarnishes the statement from the Chair that he has not discovered any other provider offering better value.

Vanguard however are cheapest

The IGC may not have spent much time on “value” but they spent a lot of time looking at costs and charges

It is of course a lot easier to compare costs to value , and there is incentive to do so when the suspicion is that Vanguard will show well (it shows very well).

I think that for SIPP customers, the cost and charges story is what they want to hear but what we really need to see is a comparison of VFM and the weak performance reporting doesn’t mean I can give the IGC report much more than an amber.

An effective report?

There are several mentions in the report of the IGC exploring individual decisions (especially where outliers).

In short , the IGC is asking the right questions and the sections on ESG and Vulnerable Customers show a great deal of deep thinking about balancing the needs of the customers (who seem neither vulnerable or much bothered by ESG) with the needs of the regulator, to pay both issues attention. Personally, I find the idea of an ESG and non ESG version of an investment pathway , silly. You either hold convictions or you don’t and Vanguard (as the IGC has admitted) hold low-conviction with ESG management. The IGC is as effective as we can reasonably hope it to be and I give it a green for effectiveness

A well written report

The report is well structured and – despite lengthy appendices’, weighs in at a manageable 20 pages. Having reviewed Churchill reports for 7 years, I am used to a high standard and this maintains it. This report gets a green for the quality of its tone and writing.

Price is not value.

Try did the return preserve or exceed the buying power of the total pot?

The excess over inflation is the real value