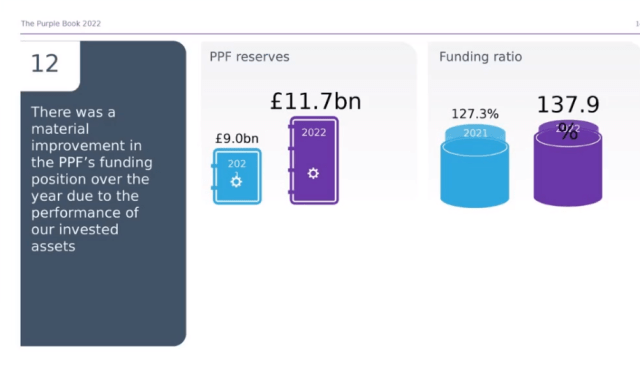

The PPF has published its Purple book – rolled out to an audience of 250 anonymous aficionados at a Pension Expert event this week. It revealed DB schemes in rude health with reserves well up and a funding ration at an impressive 138%. It’s good to see this growth coming from the valuations of investments as well as from inflows from the levy (we want the PPF’s money to work as hard as the PPF does).

The PPF now considers itself “maturing” and this means a reduction in levies from a peak of £600m and past last year’s £400m to a relatively small £200m – which will be charged to schemes in 2023. The PPF will continue to be an investment for UK plc. as a result, it should be judged on whether it is giving all stakeholders value for money, balancing the need to pay members with the needs of employers to afford to fund schemes outside the PPF

It might regard itself as a victim of its own success, with pressure building to increase benefits , reduce or eliminate the levy and find ways to distribute the surplus. But none of these decisions are going to be taken anytime soon.

It is recognising that its success brings its own challenges but it continues to be cautious, recognising that the next black swan may not be in sight but may be close by.

This analysis suggests that the PPF recognises that this shift from growth to run-off requires strategic decisions to be taken, not all of which are self-determinating, the wider public – through Government – will help determine how the PPF is run.

The primary reason for the improved financials is indicated here, assets are down but liabilities are down more (some 30%). Scheme deficits are down from £61bn to £5bn. At the end of October with only 14% of Britain’s 5132 DB schemes in deficit. These are staggering improvements in a 6 months period and come despite the scheme having to post £1.6bn collateral to secure its hedge through its LDI portfolio.

Despite war and pestilence, claims on the PPF have been very low 2022, pension funds aren’t losing their sponsors as they used to and this may well be because the financial strain of the schemes on sponsor’s P/L and balance sheet is also reducing. Whether this situation will hold is questionable, if yields fall back as inflationary pressures reduce, it will be interesting to see if schemes outside the PPF remain as resilient.

The PPF’s assessment of the corporate DB market’s overall asset allocations makes for depressing reading. Despite a call from Government to help Britain build back better, there is precious little opportunity for DB schemes to invest in productive assets, the majority of funds are in bonds and cash-backed derivatives (LDI) (impact in yellow)

The distribution of schemes that the PPF analyse is heavily skewed to small schemes (the long tail).

However the majority of the assets (and hence the resource) is with larger schemes. Despite a lot of noise about consolidation, there appears to have been no particular consolidation among smaller schemes, indeed it is the schemes with over 10,000 members which has seen the largest proportionate fall in numbers.

If there is a rush to full buy-out and master-trust consolidation, it isn’t evidenced yet!

Are small schemes poorly governed?

This chart expresses the commonly held view that in terms of a scheme’s asset and liability management big is beautiful in the DB world

The Pensions Regulator regularly claims that small schemes are a governance problem and is now pinning much of the blame on what went wrong with LDI was because of poor governance among small schemes.

This despite a commonly held belief that small schemes did not get involved with LDI. A view expressed in the second session of the recent WPC oral evidence hearing.

This table, from a reliable industry source suggests that around half of small schemes were exposed to the problems of pooled leveraged LDI

![]()

As at 31st March , these small schemes had the best funding ratios of any group of schemes analysed

We will have to wait till next year to know what damage the potential blow up within many LDI strategies has done to these excellent funding ratios. Lisa McCrory (PPF CFO) told yesterday’s audience

“We fully expect there has been some disruption to asset allocations on the back of the gilt turmoil in September. We know some schemes may have reduced their hedge or had to sell some of their assets to meet collateral calls, and as a result the asset allocations may have moved,”

No one knows what is happening to all hedging positions, but this looks like a particularly acute problem for small schemes in pooled funds.

It seems harsh on small schemes to blame them for poor governance when their schemes look so well funded . It looks doubly harsh to blame their poor governance for the LDI crisis when no-one can tell us what has happened within the pooled funds.

It strikes me that small schemes would have been better off not involving themselves in LDI pooled funds. Why did they invest and where were the warnings from the regulator? It would be a sad irony if next year’s purple book included insolvencies created by the collapse of LDI positions taken out by schemes who had used LDI as a risk-management tool.

Questions about the levy

These small schemes are also paying a higher levy per member than larger schemes as much of the levy is scheme based.

If small schemes are generally well funded, paying a proportionately higher level of the levy as they pay the same scheme based levy as larger schemes.

Is the PPF levy still necessary?

The levy came down in 2022 and will come down again next year.

But many will argue that even at £200m next year , the levy is unnecessary. The PPF know that it is a lot harder to put the levy up than down and , by its structure, it is a sop to larger schemes who get some comfort from knowing that small schemes “pay their way” through the scheme based element. Nonetheless , the PPF sound at their weakest when justifying its ongoing relevance.

Making its money work as hard as it does

The PPF is a well run confident organisation with a clear purpose and milestones which they pass ahead of time. It has a duty to its members and will have for many decades to come. The PPF works hard for us, but does the money it manages?

From what we heard yesterday, the PPF expects to be around for a long time and be managing a large amount of money on behalf of its members.

Although this is the first year ever when there are less schemes accruing DB than those closed for future accrual, there are still a number of DB plans which continue to welcome new members ensuring a need for those members to be protected into the next century.

In the meantime, there is much that the PPF can do. With nearly £40bn under management and a membership of nearly 300,000 , the PPF is one of the largest in the land. Should it continue to adopt a conservative gilt and bond based investment strategy or should it involve itself in investing in productive capital , especially the UK assets that Government bemoans are regularly bought by overseas pension funds?

Its asset management and operations are managed by in-house teams and it is notorioulsy wary of spending money on external advisers. As such it is an exemplum for other large schemes. The PPF looks to me extremely well placed to invest more ambitiously in future.

With its ongoing levy, with a funding ratio of 138% and with claims well under control, my one criticism of the PPF is that it is being too cautious.

If it wants to avoid criticism that it is becoming a fat cat, it should put its money to work, a little harder. My conclusion is that if the PPF’s billions worked as hard as its management , it would be an even better scheme. It isn’t over funded, it is under-invested.

Thanks to the PPF for yesterday’s excellent presentation.