https://readymag.com/p14287617

I am pleased to see Hymans Robertson publishing data from a number of master trusts that puts the member’s experience to the fore. They have produced a framework for understanding the impact of default investment strategies that they claim makes for

enhanced scheme governance, informed investment decisions, improved member engagement and, ultimately, better member outcomes.

What is important is that anyone gets access to this information, including members. Most members will struggle to draw too many conclusions about long-term value as the survey only covers the period leading up to and through the current pandemic. But the charts show that with a couple of exceptions (National Pension Trust and Aon) , most trusts are radically reducing risk for members in what Hymans call the “consolidation and pre-retirement phases”.

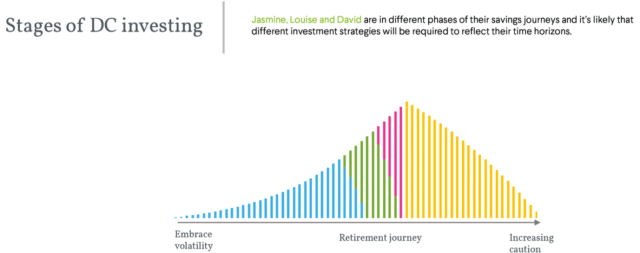

This is graphically demonstrated by a chart that will be familiar to anyone who has been involved in DB liability modelling

The retirement journey is seen as a steady series of valuations (what members see on their annual statements, with each year better than the next till a peak is reached , after which the fund reduces in an equally smooth way to zero, the end of life. This is a “journey” as imagined with a number of assumptions based on a very conventional view of work and retirement.

It also paints a picture of an ordered retreat from an ambition to grow assets (the blue line), to a more cautious approach (the green lines are about consolidation) to a point where a member is de-risked and ready to start drawing income.

In the midst of life we are in death

The common book of prayer introduces us to the phrase “in the midst of life we are in death”.

It seems very odd to me that with life expectancy into the eighties, we are consolidating for the “endgame” in our forties.

Maybe actuaries read the 1559 book of Common Prayer, which reminds us that in the midst of life we are in death.

Despite the demographic changes we have seen in the 80 post war years, the concept of de-risking ahead of “retirement” with retirement being defined by a scheme retirement age determined by the scheme funder/provider.

It would be interesting to see how these “retirement ages” differ from scheme to scheme- some will assume state retirement age at 67, others a younger age. Some schemes start consolidating 10 years before the scheme retirement age , some sooner. The pre-retirement phase, where money is shifted into bonds and cash is similarly arbitrary. But one thing that almost all master trusts have in common is a view that from retirement on , you should be invested with “increasing caution”.

This orthodoxy is grounded not in “member experience” but in a consensus that people in their sixties are not able to take much volatility in the value of their investments and need to be locked down in low yielding assets with limited scope for growth. This is a concept that is founded in DB cashflow modelling but which bears very little relevance to the average persons real life experience.

Real life experience

I am 60 and working. We know that most people in their sixties are still working, the ONS working lives studies tell us so

So the idea that we are dependent on pensions from this notional retirement age should be challenged. People’s retirement income is mainly determined by the state pension, DB pensions (including annuities) and work. Investments provide more income than personal pensions (the source of income from drawdown- illustrated by the pink wedge)

The pink wedge is tiny for men and a slither for women, it is not the source of retirement income that we like to think it is. That’s because DC pots are not yet very big but also because the default investment strategies of most DC pension schemes pre-pack savers for pot-encashment into bank accounts, cash ISAs and debt repayment.

Hymans master trust fund review is confusing about this. This comment is on the chart below it showing the incomes achieved by the providers surveyed in terms of the impact on pensions

Note, the language at this stage is about risks to “pensions”

But scroll on a little and we are asked to think about what members actually do.

Investment strategy in this phase should be aligned to members’ likely decisions at retirement. Reducing risk should be the norm, particularly as most people currently withdraw their DC pot as cash.

Again, our projections illustrate a range of investment approaches being implemented by providers. While the shorter horizon and more conservative investment strategies mean the range of potential member outcomes is generally narrower than in other phases, there is evidence that members in this phase may be assuming very different and potentially inappropriate levels of risk.

This is worth some push back. Firstly, Hymans are modelling a pot that at outset was £200k, these don’t get “drawn as cash”. Secondly, Hymans are using some conversion rate which turns a pot into a pension (not stated). Thirdly it is quite clear that the happiest members will be those in the National Pension Trust and Aon, who have taken the most risk. Hymans use the adjective “inappropriate”, presumably about these two trusts.

Just how much risk is being taken can be seen from the preceding chart

It is as if Hymans are pointing to all the providers with 10% + volatility and accusing them of cheating.

But if you are getting 10% + returns , do you really mind if your provider took a lot of risk? Well you might if you were wanting to cash out, but let’s remember, this is modelling on people with £200,000 looking at their annual income to come from their pot.

And whether you have a big or small pot, you are reaching this artificial retirement date with a life expectation of another 25 years. Why is risk taking “inappropriate” for someone in their sixties?

So are we judging member outcomes correctly?

I think we need to be clear about what a member considers a good outcome. If we are preparing members for cashing out their pots, then I can see that delivering with a high degree of certainty means lots of de-risking and that a lower outcome might be “appropriate”. But if members are looking for a pension from their workplace pension, then de-risking to an “increasingly cautious” fund at retirement, makes no sense.

It is as if we are giving up on pensions and accepting that people only want cash. But we know from a number of surveys that when people are asked what they want from a workplace pension , they describe something remarkably like an annuity.

I do not think we should be censuring the providers who are to the right hand side of the box above. Even those like Smart, Mercer and Lifesight – which haven’t seen their bets pay off, have at least been ambitious.

The failure of some master trusts is that they do not offer continuation options through retirement which enable defaults to pay income through drawdown. This means that money has to be encashed to be sent off to the SIPP that can do the income thing. This explains a strategy which targets as little risk as possible. But this is simply giving up on pensions and cannot be applauded.

For defaults targeting a point at which people start drawing on their pensions (in whatever way), we should not be targeting cash but growth. Because if you de risk to the point that many providers on the left of the chart are doing, you are signposting to members that in the midst of their retirement journey, they should be ready for death!

A better way than de-risking

As you can see, Hymans get themselves tangled up between those with big pots who think in terms of “pensions” and those with little pots who think of pots as “cash”. Treating those who want pensions as wanting cash is bad for those with big pots and the reverse is also true. Some master trusts – Aon and National Pension Trust for instance, seem to be saying to members, “stay invested and draw a pension”, others like NOW and Workers Pension are saying “cash out”. But NOW is Now Pensions

NOW PENSIONS!

And Workers is a Pension Trust (and inside Cushon).

If master trusts are to maintain the word “pension” in their title, then they should be aspiring to pay pensions, not accepting that they will pay cash. That means taking a long term view on investment and risk and not assuming that in the middle of the retirement journey – the investment strategy rolls up like a shrivelled snail and growth and volatility are killed off. That is DB thinking and what’s more “closed” DB thinking. Neither pensions or life deserve to be de-risked half-way through.

What is the average pension pot for someone who is age 60 and earns £25,000 per annum. In the last 6 years of AE, probably he was working for 2 companies and has two pots of £7,000 each!

What could someone with these two pots could think of? Nothing more than encashing them before State pension age and starting that deferred DB scheme!

How many £200,000 pension pots are there from auto-enrolment? I can tell you very, very few!

I very much agree with your thrust here Henry. I believe so called ‘Lifestyling’ just does not fit modern lifestyles and that pension default funds are out of date. Selling higher return assets in your 50s, when you could still have a 25 or 30 year investment horizon for much of your fund, makes little sense to me. And encouraging people to keep investing into their 60s makes sense unless they know an exact date that they plan to stop working and have no other pensions to draw on. Those who are still 55 or so do not necessarily need to abandon return-seeking assets and for a fund to automatically do this for them, without bothering to even ask about any plans for retierment or annuity purchase and so on, seems sub-optimal in the current world. I understand that others disagree and they may consider this proposal recklessly adventurous, but I think a strong case can be mad3e that current lifestyle default funds may be recklessly cautious. Especially with inflation and interest rates more likely to be higher than lower

I couldn’t agree more, Henry. Pension providers tend to forget the State Pension’s (and DB benefits) impact on many members’ risk profiles. We also know that many people retire later than schemes assume and so de-risking starts too soon. And for many, drawdown is potentially a better option, so keeping some risk on the table is entirely appropriate.

To Eugene’s point, the weight of DC wealth is still with the higher earners. Lots of reasons for this but mainly their capacity to save and the incentives to save are geared at those on £50k+. Ant and Ros’ point to the legacy of DB thinking in our DC system. DB has been strangled by the desire to guarantee things (something that pension freedoms released us from). But we haven’t yet been able to agree an alternative. We still think in terms of “cash” or “pension” but have yet to build a reliable alternative to the annuity.