A Response to the DWP

Consultation on

Illiquid Investments and Performance Fees

Dr Con Keating

Chair, EFFAS Bond Commission

April 2021

It would not be surprising if the DWP were swamped by responses to this consultation from the ‘alternative investments’ industry and their lobbyists. I hope that you will recognise these as vested interests. I am writing this as Chair of the Bond Commission of the European Federation of Financial Analysts Societies. My response is grounded in my more than fifty years of experience managing investment portfolios institutionally.

There is nothing intrinsically objectionable to the purchase of illiquid securities by ‘pension’ funds. Strictly speaking DC funds are merely tax-advantaged savings accumulation arrangements. The draft of the new Code of Practice outlines the current position on investment decision-making:

“Governing bodies of trust-based pension schemes with 100 members or more must invest in a way that ensures security, quality, reasonable liquidity and profitability for the scheme as a whole. … The law also requires these governing bodies to invest scheme assets predominantly in regulated markets. Unless there are exceptional circumstances, governing bodies should ensure no more than a fifth of scheme investments are held in assets not traded on regulated markets.” However, it appears that many large DB schemes have allocations materially above this 20% limit; for example in their 2018 valuation, USS report that 23.7% of the assets of their implemented portfolio are invested in “Private Markets”.

There are though some further significant concerns. The first of these is that such assets may prove extremely difficult to realise in response to demands from the holders of fund units. We have seen this occur recurrently with respect to conventional property funds in times of market and economic stress. Denying immediate access (“gating”) to the value of a unit-holder’s claim may serve to reduce ‘fire-sale’ losses of value, but that is far from guaranteed. The classic recent exemplar is the liquidation of the Woodford funds.

There is in general a problem with the valuation of illiquid instruments. They are marked to model, not marked to market; the result of this is that their valuations will appear far less volatile than their market traded counterparts. In the case of property, it is common to see wide variation between the performance of a property company’s net asset value, a modelled value, and its market price. The net asset value (model) of Land Securities fell by 9% in the six months to March 2020 while the share price (market) declined by 35%[1]. As volatility is the most widely used measure of risk, this allows the unscrupulous to present, and the uninformed to consider illiquid investments as being less ‘risky’ than their traded counterparts.

Portfolios of illiquid investments may often be ‘hollowed out’ by these methods of valuation. With private equity, the successful investments within a fund may be realised by sale at values which are at or above their modelled values, while the ‘lemons’ continue to lie within the fund and tend to increase in number with the passage of time. These ‘lemons’ may, ultimately, only be realised at a small fraction of their modelled value. In the meantime, the private equity manager has reported and collected fees on a strong performance.

The valuation problem is much less acute for bonds and debt securities, provided there is clear and timely disclosure of financial condition by the issuer. The debt financings for infrastructure projects should fall into this class of illiquid investments.

There is no natural linkage between illiquid investments and performance fees. In fifty years of investment in (commercial, industrial and residential) property, I have never even been asked to pay a performance fee to a manager. Similarly, I have never encountered performance fees for illiquid untraded debt securities. They are certainly not necessary features of infrastructure project financing.

If there is a case for performance based managerial fees, these should be a matter of contract between the entity and those managers, not related to the performance of investments in those entities.

This brings me to a current concern. As a result of quantitative easing, the price of liquidity is currently at or close to an all-time low. One result of this has been that the investment banks have cut their inventories of traded debt securities by well over 90%, as the creation of this credit has not been sufficiently well-compensated for them[2]. The chase for yield by pension funds and insurance companies has spread widely across the different classes of investments, driving prices up and future returns down. Given that it is likely that we will eventually return to market conditions where liquidity is appropriately priced, the idea that pension funds should be buying illiquid instruments now is clearly misguided.

Performance fees are largely confined to ‘alternative’ investments. Hedge funds are typically no more than investment strategies operating in liquid securities markets. The lock-up periods associated with these have no relation with the liquidity of their investments, which are overwhelmingly traded securities. By accepting these lock-ups, the investor should be expecting to receive more than when investing in a UCITs-type mutual fund. There was evidence early in the development of hedge funds that there were excess returns to investors, though when corrected for the leverage involved these returns were little different from unlevered market allocations. As strategies operating on market securities, we should not expect an excess return from hedge funds.

The most popular early form of private equity, the leveraged buy-out fund, also showed strong excess returns. However, it was subsequently shown that the majority of this outperformance came about from the disenfranchisement of the prior debtholders. As this led to stronger bond and debt covenants in corporate financings, this source of performance has been eliminated. This brings us to private equity. There is a considerable body of academic and practitioner research[3] which shows that there are no material gains from private equity above those of listed equity markets. Indeed, there is evidence of substantial failure, as may be gauged by the table below, which shows the experience of a major US DB fund (LA County) with many billions of PE investments. The benchmark is the Russell 3000 index.

| Realised | Benchmark | |

| One Year | 13.71 | 21.47 |

| Three years | 12.64 | 14.89 |

| Five Years | 11.81 | 15.86 |

| Ten Years | 12.44 | 14.42 |

This experience marries well with the observation here in the UK that the total costs, that is ad valorem and performance fees, associated with private equity are typically in the range of 3% – 5% p.a.

There are sound theoretical reasons to expect the returns to leveraged buy-out funds and private equity, more generally, to be lower than those of listed equity. These funds are typically buying liquid securities, and in doing so, paying the liquidity cost of the market at that point in time and in addition, they are paying a ‘control’ premium. If their exit is by way of a public sale, they may expect to receive the liquidity premium at that time, though they will have borne the costs of a public offering to achieve that.

It happens that the current outlook for private equity is not stellar. Funds have unprecedentedly high amounts of uninvested cash and also access to extremely high levels of leverage, resulting in extremely high prices for the companies they might wish to buy.

It should be said that the presentation of the returns of private equity funds is all too often an exercise in the dark arts. The figure published are almost always those which present the fund in the best possible light and allow the manager to extract maximal fees.

I would also point out that all of these ‘asset classes’ can all already be bought on the London Stock Exchange where they are listed and traded as closed end investment trusts; for example: Pantheon International plc (private equity); 3i Infrastructure plc (infrastructure; BH Macro Limited (hedge funds) and Tritax Big Box REIT plc (property). The investments made by these closed end investment trusts can pay whatever performance fees they feel appropriate. In addition, of course, these investment trusts do not suffer the liquidity problems of ‘gating’ and the like, as the pension fund owns and can trade shares in the investment trust in the market. Indeed, an investment trust could consist entirely of illiquid investments, with no effect on its share price. The proposal to modify the charge cap is not only unadvisable, itis unnecessary for the promotion of investment in the desired classes and forms.

Conclusions

In moderation, illiquid instruments could serve to increase the returns achieved by ‘pension’ funds. However, this should be limited in extent, unless it is proposed also to restrict the ability of scheme members to switch funds (and cash).

There is no reason at all to associate illiquid investments with performance fees. Indeed, performance fees applied to the capital of a firm, and the returns on the instrumental claims on that, are misplaced. Such fees should be applied to and contained within the performance of the firm.

The so-called alignment of interests of manager and investor through the use of performance fees is more Potemkin village than reality; there is a clear principal/agent conflict.

The charge cap has led to lower costs for pensions savers, though there are still some evasions which need to be addressed. It has been a success. The proposal to accommodate performance fees by smoothing over many years would be a mistake; it would misrepresent the true position of the fund and raise costs while the gains seem likely to prove illusory.

As all of these alternative asset ‘classes’ may be accommodated within closed end investment trusts, modification of the charge cap is unnecessary.

Postscript

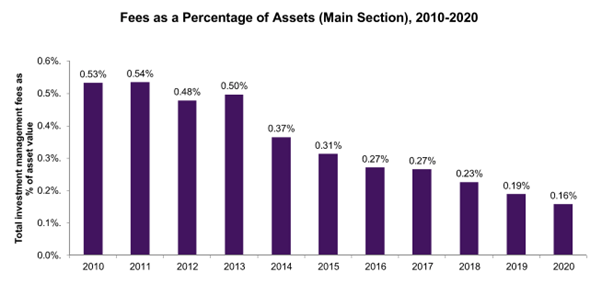

Since writing and submitting this response, my attention was drawn to the following analysis of the costs and charges of NatWest schemes. Firstly, we are shown the benchmarked income and fee expense of different classes of assets held by the scheme over the period 2010 – 2020.

There are not many conclusions which can be drawn from this analysis alone, though it is interesting that liability hedging is costly, as should be expected, though rarely recognised. The NatWest analysis continues with a breakdown of the proportions of gross value added retained by the scheme and paid to the fund managers involved.

This is a most basic measurement of value for money. It is striking that hedge funds and insurance had fees and charges which were as high as or higher than the investment returns earned. Private equity is also striking with some 85% of the gross value added being paid away to its managers. The sectors offering the best value for money are quoted equity and credit, the traditional asset classes of DB schemes.

The final figures show that the NatWest scheme has been rather well managed in the sense that over this time they have reduced management costs markedly. The reductions have saved the scheme 1.45% of its value to date and hold the prospect of saving almost 16% of its value over the coming forty years.

[1] The reported NAV was £11.82 at end March 2020, while the share price was £5.57, a 53% discount. I am indebted to the Secret Pension Fund Manager for this illustration.

[2] There are further relevant measures of the price of liquidity, such as the on-the-run/off-the run spread of US Treasuries. There are also measures of the quantity of liquidity, such as the volumes of new debt security issuance and secondary market turnover, most of which is now brokered rather than principal account traded.

[3] See, for example the work of Peter Morris and Ludovic Phalippou of the Said Business School Oxford. There are also commercial performance analysts who have similar findings – see Chris Sier, Clearglass and Henry Tapper, Agewage.

Pingback: Pensioners cannot afford private equity’s current fee scales | AgeWage: Making your money work as hard as you do