Covid-19.arg

Global and UK Economic Recovery up to September 2020

COVID-19 Actuaries Response Group – Learn. Share. Educate. Influence.

Joseph Lu

Summary

- There are clear signs of economic recovery in the UK following the lockdown between March and June, as shown in the monthly GDP estimates in the UK. This is supported by improved turnover and trading of businesses. These are consistent with the recovery of the global economy.

- However, the job market is still wobbly with falling vacancies and hours of working, compounded with rising redundancy. It remains to be seen if it will improve with the economic recovery.

- OECD projections suggest the UK economy, unlike the global economy, will not have fully recovered by the end of 2021.

- Ultimately, with rising infection in the UK, the economic upshot will depend on the spread of the virus, government’s policies on daily and business activities, and the ability of health services to manage the pandemic.

Introduction

In this note we summarise two recent and worthy reports on the current economic outlook with particular regard to the effects of the pandemic – one by the OECD, one by the ONS.

The OECD Interim Economic Outlook of September 2020 reports on global economy:

- The COVID-19 pandemic has led to government policies and public behaviour that limit movements and economic activities, aiming to combat the spread of the disease. As a result, global economic outputs slumped in Q1 and Q2 (Figure 1 below).

- In response to the recession many countries implemented fiscal and monetary policies swiftly and in large magnitude. Consequently, we have seen a rebound of economic activities since Q2.

- However, the outlook remains uncertain, depending on the virus, policies, people’s behaviour and economic confidence.

- Policymakers can play an important role in shaping the recovery by:

- Supporting the economy, do not withdraw fiscal support too early.

- Helping people find new jobs, target those who most need support.

- Seizing the opportunity for change, such as investing in digitalisation and the environment.

On a global perspective this picture is an improvement on the OECD’s June projections (Figure 2), which showed a more significant negative impact from a “single hit” scenario, together with substantially worse “double hit” scenario (to which they ascribed similar likelihood).

What has happened in the UK’s economy?

- Based on ONS data, UK GDP has bounced back to some extent but is still below its pre-pandemic level. For example, it grew by 6.6% in July 2020, the third consecutive monthly increase, but it has still only recovered just over half of the lost output caused by the pandemic (Figure 3).

- Different sectors have recovered to different extents. For example, the construction sector was hard-hit between March and April, but recovered more rapidly between May and July.

- Within the service sector, some services are more affected than others. For example, the output of accommodation and food sub-sector in July was 60% lower than that in February. The equivalent figures for wholesale & retail, finance & insurance, real estate and public administration and defence for July are within 5% from that in February.

- Likewise, different manufacture sub-sectors have performed differently. For example, manufacturers of basic pharmaceutical products have seen about 10% higher outputs since February. But the outputs for manufacturers of transport equipment have seen a drop by more than 60% between February and April only to climb back to 25% below pre-pandemic level in July.

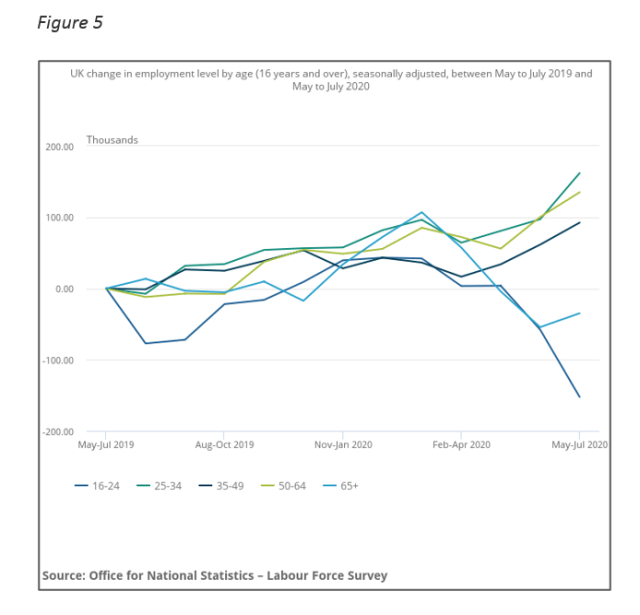

- Employment prospects have been adversely affected since February, with falling vacancies and working hours and rising redundancy (Figure 4). Younger employees, age 16-24 years, are particularly hard-hit (Figure 5). It remains to be seen if the economic recovery would eventually improve employment prospects.

Own calculations of ONS data. GDP monthly estimates, UK: July 2020 published on 11 Sept 2020.

Own calculations based on ONS data – Labour market overview, UK: September 2020. Weekly hours worked and vacancies are seasonally adjusted.

There has also been a large decrease in the number of young people, aged 16 to 24 years, in employment over the last quarter (Figure 5).

The ONS published ‘Coronavirus and the latest indicators for the UK economy and society: 1 October 2020’ which reveals that:

- The shape of decline followed by recovery of turnovers of businesses broadly reflects the recovery in the UK’s monthly gross GDP. This further confirms the UK’s V-shape economic recovery, but there are problems ahead with rising daily infection cases.

- 85% of businesses were currently trading, compared with 66% of businesses in the previous survey of 1 June to 14 June 2020.

- 11% of the workforce were on partial or full furlough leave. With the furlough scheme ending in October, the workforce affected by the state’s policy-induced reduction in economic activity needs to be managed to avoid disruption in employment.

- Recent counts of cars in London, 21-27 September, were comparable with that of the average level seen immediately pre-lockdown, according to traffic camera data. This indicates a recovery in public confidence in carrying out daily lives which is conducive for economic recovery.

What is the outlook for the UK economy?

The OECD, in their September forecast, projects a 10.1% reduction in real GDP for the UK in 2020. This is a slight improvement on their “single hit” projection from June 2020, which forecast a 11.5% reduction in GDP. But it is significantly worse than their global projection of a 4.5% reduction in real GDP.

They project a continued bounce back in 2021 of 7.6% growth, although this would leave UK GDP 2.5% below 2019 levels. This is in contrast to their global projection of 0.5% cumulative growth over 2020 and 2021 in aggregate.

This economic stress raises some wide-ranging questions, as it will affect different sectors, jobs and demographics differently:

- Would this economic stress widen socio-economic gaps, leading to widening health and mortality gaps?

- Will the inter-generational wealth gap widen, as the younger generation suffer more in job losses in this crisis?

- How will the economic stress affect the retirement savings and retirement planning of the UK’s ageing population?

- Will the fall in asset values lead to later retirement?

- As COVID-19 hit the older population harder, how will it affect their work and income?

Unlike several previous economic downturns that were caused by asset bubbles, this one is caused by a health crisis that has led to government interventions that has shocked the economy. State financial packages, economic policies and easing lockdown have managed to absorb the shock to a large extent but not fully. What lies ahead is a balancing act of managing a health crisis without disproportionately damaging the economic activities that support health and wellbeing.

12 October 2020