With a deft tweet , former Pensions Minister Steve Webb wakes us up to a startling economic revelation.

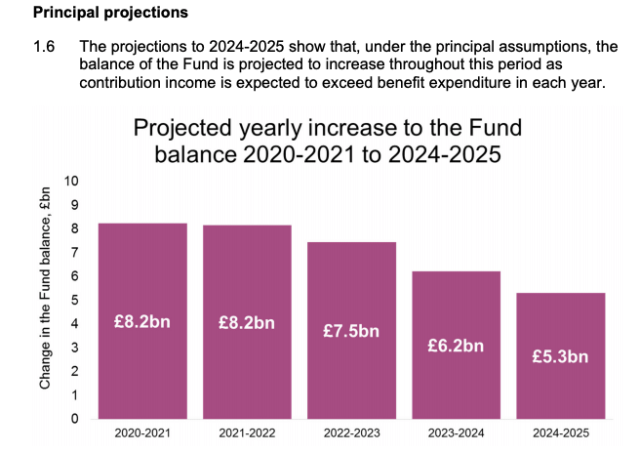

Doesn’t seem long since we were reading doom-laden warnings about the National Insurance Fund ‘running out of money’ in a few years. Today the Govt. Actuary says next year there will be over £8bn more in income than expenditure https://t.co/2IXQnrXhMw

— Steve Webb (@stevewebb1) February 12, 2020

Trevor Llanwarne’s grim warning

Trevor Llanwarne

In the last quinquennial review of the fund , the previous Government Actuary warned that by 2020 we might have to unwind the triple lock.

The triple-lock turbocharges state pension increases so that we can gradually align our state pension with the kind of benefits people expect from a first world country

Trevor Llanwarne (the then Government Actuary) warned that the National Insurance Fund might not get further hand-outs from the Treasury to meet state pension obligations. He implied that we would have to start thinking of auto-enrolment as a way-out of re-rating our state pension to something we could be proud of.

You can read all about this in blogs I wrote at the time.

Martin Clarke’s brighter vision

Martin Clarke

Martin Clarke presents an altogether brighter view of the future in his report to parliament on the current state of the fund.

You don’t have to be a Government Actuary to see that things have taken a much rosier turn than anyone expected in 2015.

So what has happened?

Well the last 5 years have been good years for work and pensions, good years (unsurprisingly) for the Department of Work and Pensions.

Far from going back to the Treasury for more money, the Treasury (GAD) are now telling the DWP that the outlook for the next five years is set fair.

Gloomsters can point to darker clouds on the horizon after 2025 as we continue to feel the impact of higher numbers in retirement and lower numbers in work, but we are in the happy position of building up a positive (notional) balance on the national insurance fund, which should go a long way to improving the lot of those who most rely on the state pension – those on low retirement incomes.

What has happened to effect this happy turnaround is that we have had full employment and reasonable wage growth, receipts of national insurance have boomed accordingly.

The projections forward show that we will have more than 6 months coverage from reserves to meet any shortfall in fallow years to come.

I don’t want to overdo this but..

Predictions of the demise of the triple-lock are premature. We will get a state pension which looks a credit to our benefit system, assuming we hold our nerve and we don’t listen to the gloomsters and naysayers (I am conscious that I should be wearing a blond wig in saying this).

Sorry Steve but you have to fall in line with the Government Actuary right now!

Pension predictions really really should look long term. My actuarial training bias.

— Steven Cameron (@_StevenCameron) February 12, 2020

We have moved on – thanks Karen!

They do. If one considers the Quinquennial Review alongside the annual Uprating report https://t.co/chR7XZEbyS

— Karen Wake 🕷 (@pensionmonkey) February 13, 2020

I look forward to Martin Clarke’s first quinquennial with relish and hope that it can paint a rather happier picture than the one we created for ourselves in 2015.

A happier prospect for those retiring.

For as long as I have been studying announcements on the state of our future pension finances, I have been assailed by gloom and doom.

Thanks Martin Clarke for your upbeat assessment of our current position, your cautiously optimistic view of the next five years and your relatively relaxed view of what follows.

I don’t want rose-tinted spectacles but neither do I want a blindfold! This reports opens our eyes to a much happier picture of public pension finances than we could ever have imagined five or ten years ago.

We should be very happy.

Martin Clarke

Pingback: Our right to dream of a fairer deal for older people. | AgeWage: Making your money work as hard as you do

Pingback: The progressive pension agenda this country needs | AgeWage: Making your money work as hard as you do