NOW pensions, perhaps tired of being labelled the pariah of master trusts has come out fighting with the following table which shows in certain circumstances, their charging structure provides good outcomes, investment returns being even.

Because of the peculiar nature of NOW’s charging structure, the impact of the £1.50pm policy charge dilutes over time while the impact of higher percentage of fund management charges (AMC), increase over time. NOW’s costs are front end loaded, hurting those who only make a few contributions, those with higher AMCs are back end loaded and hurt people who keep their contributions going and build up a hefty fund.

The problem with this analysis is that it ignores the fact that people move jobs on average 10 times over a career and that those with 20 years paying monthly contributions to one provider are minimal compared to those with lots of small pots.

Adrian Boulding, who was brought up in the days when life companies used to report profits based on 20 year persistency assumptions, knows only too well that the 20 year career expectation is a tad rosy (for all but L&G actuaries!).

So why is he trying to pull this stunt?

I suspect it’s because NOW are in the final phase of getting their Master Trust Authorisation after which it will be the Dutch Cardano, not the Danish ATP who will own NOW.

So it’s time to get on the boxing gloves and show that NOW are still the combative and disruptive force they were when they started out some eight years ago.

And of course, one of the great features of master trust advertising is that NEST aren’t really able to do it so everybody else can say what they like about NEST without fear of getting much more than a metaphorical upper cut from the (sadly departed Debbie Gupta).

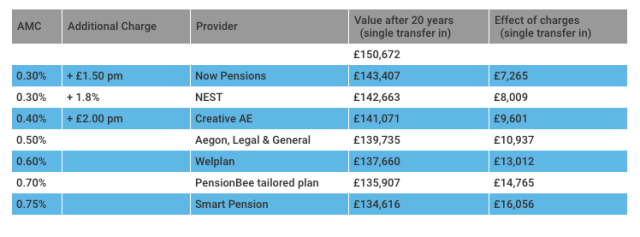

NOW are proving that old habits die hard and happily misquote NEST as having a 1.8% additional charge not just on regular contributions (See above) but on transfers in. The table below is looks at a single contribution or transfer-in of £28,000 (equal to one year’s earnings) from another pension plan:

Adrian Boulding tells me that he had spotted this mistake and re-cast the numbers but that’s not what this looks like to me. This looks like NOW simply rolling forward their numbers with a £1.50 pm management charge while NEST has a £504 deduction (1.8%) at outset. Unsurprisingly this gives NOW an edge which is totally fictitious.

So in good old -fashioned disruptive style , NOW are peddling fake news which I suggest would be picked up by the advertising standards authority if pension fund disclosures were taken seriously by anyone.

Of course no one takes this stuff seriously – why should we?

The article evinced plenty of huffing and puffing from Smart’s anonymous spokesperson and from Pension Bee’s feisty CEO Romi Savova. John Greenwood managed to collect the bitching into a single article (though disappointingly he did not get the thoughts of NEST on the misrepresentation of their single premium charging structure. You can read the knockabout stuff here.

Romi’s indignation spilled over onto Twitter

We don’t know because @NowPensions have yet to publicly respond to the @CommonsWorkPen letter from 22 February.

However, they did find time to make this misleading index, which may result in more pension pots vanishing.

— Romi Savova (@romisavova) July 26, 2019

Where is People’s in all this?

People’s Pension , which used to be relied on for getting involved in a charges punch up refused to share data with NOW pensions. They have a new charging structure that Adrian Boulding couldn’t quote but which would have made People’s look quite competitive in the second table. Like People’s, Pension Bee’s charging structure rewards larger balances; to quote Adrian

“Romi halves her bee sting on funds over £100k”

It’s becoming quite a feature of People’s – they are isolationist and grumpy, I say they should lighten up – especially that poe-faced curmudgeon Gregg McClymont who should stop reading from the gospel according to Saint “Not For Profit”.

So what of slippage?

While all this slap-stick’s been going on, we’ve failed to address my earlier question, why does nobody take any of this seriously.

One answer is that simply comparing pension plans on the basis of overt charges is bonkers. It’s not like we’re even talking total cost , there are all the costs within funds that never get displayed in any of Adrian’s boxes but eat away at outcomes in exactly the same way.

The reason no-one quotes slippage in tables like this , is that it leads into the other component of value for money – value. If you’re going to quote the cost of investing, you need to quote the value of investing and now you start getting into deep water (especially if you are NOW). You are now not swimming in the lifeguard section but in open water.

We don’t have slippage because NOW are not happy getting out of their depth.

The tawdry state of cost disclosure

Bottom line, this cost disclosure stuff is old school and pointless. People are fed up with meaningless numbers thrown at them. They want to know how their pots have done, not this abstract projection stuff.

So long as we duck reporting on people’s actual investments and persist in fooling around with 20 year projections, people are going to carry on rolling their eyes and thinking “same old, same old”.

We need to have individual reporting on people’s own pots and that’s only going to happen when NOW, Peoples, Pension Bee, NEST , Smart and others start telling people what’s actually happened to the money that they last saw as a deduction on their payslip.

Quoting costs without reference to outcomes is like buying butter without bread.

So let’s get serious for a minute and start focussing on what really matters, the members and policyholders of the schemes we invest in and manage.

In Australia, super fund performance tables is completely normal. However, that does not stop some Aussie funds trying to game these performance tables, so not perfect. But, it is a lot better than the dark ages we are in for UK DC.

As in this case as Smart Pensions is £1.5 pm plus 0.25%

I think you’re confusing Smart Pensions with someone else John. Smart Pensions has a flat 0.75% pa AMC charging structure