Here is a snip of information that has shocked and outraged many pension commentators.

I will start with some simple advice from the Low Income Tax reform Group (LITR)

You may be able to draw money out of your money purchase or defined contribution pension very flexibly – as much as you like, when you like, from age 55. But do not rush. A hasty decision could cost you heavily in the form of an unwanted tax bill and even a tax credits/benefits overpayment. This page highlights key tax and related points to be aware of.

You have a great deal of control over what you take out of your money purchase or defined contribution pension and when.

The rules are very complicated in many ways and you should try to understand them before you act.

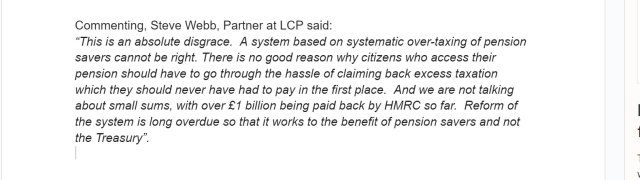

The £48m repaid by HMRC to taxpayers is more than double the £22mn in overpaid tax repaid in Q1 last year. In one way, we should be celebrating that people are engaging with their pensions by spending their pension pot. This money is – according to Jon Greer of Quilter, demonstrating “the continued necessity for people to access their pension funds amidst the cost-of-living crisis”. If pension saving is helping people heat and eat , then good. We save to spend and that formula works for the Treasury as it does for the person feeding the meter.

In another way, we could be roundly condemning a system, which eight years after kicking off is still working very badly.

I’m with Steve Webb on this, I may be with John Greer if he is right that this increase in money is emergency funding for households in trouble. If however, the Quilter view is that this is money that is no longer attracting management charges- I take a different view.

The need for a wage for life – taxed as a wage for life

When people join a pension scheme, they probably have a vague understanding that the pension scheme will pay them an income when they stop working. That’s what I thought and still do.

The trouble is that for most savers, a pension is a pot of money, which they access at their peril, often with dire tax consequences,

The First Actuarial Muppetometre was designed to help people understand that simply cashing in pensions without taking the care, LITR advises, could leave you..

Were the HMRC regulated by the FCA and subject to the Consumer Duty , they would be in the dock for abusing their vulnerable customers. (Steve Webb’s point).

The freedom to fuck up is not freedom – it is servitude for all but the few

There has to be another way for people who don’t get pension taxation and don’t get LITR’s , MaPS’ or a financial adviser’s help.

Last week , Pension PlayPen heard from Arun Muralidhar about a SeLFIE, a sort of national savings bond people could buy which paid back a set rate of income for 20 years.

On Friday, I heard Adrian Boulding , brilliantly explain how a CDC device could turn a pot to a non guaranteed pension (and could be live by the end of this parliament).

So there are other ways available.

It is now up to people like me, and Adrian and Arun and Steve Webb, to make sure that whatever solution we want to simplify the current mess – becomes a reality. I know that Steve’s eventual annuity is a good idea – it’s based on buying an annuity when an annuity makes you feel good (when you are older), I know that Arun’s plan makes sense for people who don’t want to go anywhere anything called “investment” and I know that CDC style pensions are the way forward for the majority of people who want an income but no guarantees. Currently none of these plans are available.

All of these plans give us freedom from freedom, by converting pot into pension. There will be nay-sayers on all sides arguing that people don’t want to lock their money away or rely on others to manage their cashflows. For these people there are financial advisers and DIY spreadsheets to do the cashflow modelling and longevity estimation.

But for most people, financial advice and DIY spreadsheets are no good. They are not a sustainable feature of their retirement living. They want something good that gives them a wage for life – an AgeWage.

We cannot give up on the good, just because the bad is not being complained about. The bad that is being done by HMRC is increasing because we aren’t suggesting good. That is bad on our part, we can’t blame HMRC for everything!

So let’s get on and get these new ideas moving.