The Pensions Regulator has published its 2022 to 202 DC trust: scheme return data

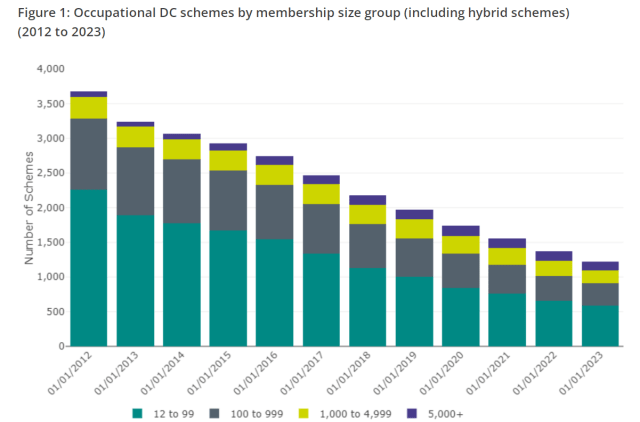

The two key images are the chart and table below. They talk to the consistent picture we have seen since this research and analysis began – shortly before the start of the auto-enrolment project. Visually the distribution of schemes looks like this.

Numerically, this table tells the same story.

Picking the nuts out of that

It’s interesting to think of these in the light of TPR’s strategy to move focus from DB to DC. Tomorrow we will have the Regulator laying out a package of DC reforms which no doubt will attract guidance and enforcement from TPR.

And of course there is a lot more to DC saving than TPR regulated schemes. A huge amount of retirement wealth is stored in non-workplace pensions which are certainly not aiming to be pensions in the accepted use of “pension” but which are being used for everything from inheritance planning to advised and non-advised drawdown. About 10% of DC money is being voluntarily annuitized. TPR’s numbers do not cover GPP/GSIPPs which are regulated by the and have IGCs and GAAs as fiduciaries – rather than trustees.

Numbers are based on data on the TPR register on 31 December 2022.

These are the numbers that matter

TPR now recognises 26,990 – “D.C. schemes”.

The “you cannot be serious”

Of these 25770-have fewer than 13 members most are executive/owner arrangements used for tax-planning, some are genuine small schemes for employees’ benefit

TPR knows very little about over 10% of the schemes , and many more are by nature too small to be of public concern. If you are in a small DC scheme, my advice is look at getting out unless you are pension confident. TPR does not have the resource to pay attention to your scheme

The semi-serious

On the other hand there are still 1,220 schemes with more than 12 members. This is down from 1370 a year before and down from 3660 in 2012. This is rapid consolidation. The DWP will be wondering if this down to them or to other factors. Other factors include

- The cost of running your own scheme is high relative to participating in a DC master trust

- Greater transparency and awareness of VFM can turn pensions from an employee benefit to a PR problem.

- The risks of getting it seriously wrong are down the line but if American experience is repeated, could lead to class actions from disgruntled employees – why take that risk?

But almost half of the “larger schemes” look like vanity projects. 590 of the 1220 have 12-99 members.

All of these members generate regulatory levies and most of them no longer work for the sponsoring employer.

Getting serious

There are 26.4 million members in the 1220 non-micro schemes. This is Up from 23.4 million a year before and this represents a serious escalation of the small pots problem

25.8 million memberships are in the 130 schemes with 5000+ members. These are the schemes that Guy Opperman considered viable , though it should be noted that there are several commercial master trusts either up for sale or enjoying little support from their shareholders. All the indications are that most master trusts would sell if they could find a buyer at an acceptable valuation, Nest being the exception.

The number of memberships in the 1090 schemes with 12-4999 members is falling at each size level. This is one of the least easy to explain statistics. My suspicion is that many of these schemes are finding ways to transfer to master trusts groups of savers – typically deferreds and especially older deferreds for whom they have no investment pathways Member Growth is concentrated in a very small number of schemes – the very largest 130.

Soon that number will dip below 100. This concentration of schemes has advantages if Government can really ensure VFM is improved, it carries the risk of concentrated strategies – a risk we have recently seen in DB schemes.

Assets show similar patterns.

Of the total £143bn in DC assets ( still a very small number, much smaller than LGPS and tiny relative to corporate DB) , £135bn is with 130 large schemes and that is the only group where assets grew in 2022. This is almost certainly because contributions exceeded investment losses here , whereas other schemes had either low contributions or higher losses.

Do assets present a risk?

I am very concerned about the damage in the long tail of legacy occupational (and contract) DC schemes. If they aren’t being measured, who knows what assets are invested in.

I remain haunted by these three bullets in this year’s L&G IGC report. When did the 380,000 members get out or 15 year gilts. By extension, how many schemes – who don’t have an IGC but scantily supervised trustees, remain in the wrong assets?

I hope that L&G will put my mind at rest – as they have promised to do.

Other thoughts

It takes patience to work through all the tables in the Pension Regulator’s report

Sometimes dual section hybrid schemes are included and sometimes not. I found myself confused with the detailed narrative and do not want to draw conclusions where I have insufficient stamina to do so properly

But a few snippets are interesting.

- These statistics reinforce the conclusions. I’ve drawn above.

- Only 500 of the 1220 non micro schemes are open to new joiners.

- The number of active members in non micro schemes is 11.2 million up from 10.2mn a year before.

- The number of deferred members has increased from 13.2mn to 15.2mn.

- The ratio of deferred to active members is highest for the smallest schemes.

What is worrying for master trusts is that while the number of schemes is consolidating, the consolidation is not feeding through to member accounts which are still struggling to exceed £5,000 per member.

Despite most member’s pots falling in value in 2022, I am surprised to see such a flat asset/per pot chart over the past 7 years. Assets per pot a third what they were at the start of auto-enrolment and this spells trouble for the commercials of larger occupational schemes.

If member’s are voluntarily consolidating, they aren’t doing it to their occupational workplace pension.

Conclusion

My conclusion is that the number of D.C. schemes is falling pretty quickly and everything is consolidating into the largest schemes – the master trusts.

Whether this would have happened anyway or whether the Government’s consolidation initiative have made a difference – is hard to say.

There are two factors inhibiting scheme consolidation. The first is the complexity of occupational DC schemes which are often carrying hybrid benefits (e.g. have some residual guarantee). The second is that efforts to consolidate at the member level are frustrated by our not having a dashboard and having a “red and amber flag” system in place which is making pot consolidation a problem for savers. Putting aside the important need for master trusts to consolidate between themselves, it looks as if we need to continue to put peddle to metal – to get a really valuable private DC pension system

The trend is towards consolidation but it could and should be an accelerating trend – and really it isn’t.

Pingback: Receiving value for your money – the DWP gets it 95% right. | AgeWage: Making your money work as hard as you do