Tone and style

I’ve waited a long time to say it , but Fidelity’s 2021/2 IGC report is a corker. I thought it would be even before I read it when I saw what the IGCs priorities were for this year

-

Ensuring changes to FutureWise are implemented across all pension plans as soon as possible;

-

Monitoring improvements to the retirement journey so that members can focus on important investment decisions;

-

Ensure members have access to comprehensive retirement tools that that incorporate their total retirement picture;

-

Monitor the consistency in the fund range for non-advised employers including sustainable investment and decumulation options;

-

Ensure member communications are focused on providing members with confidence in their default and how it is designed in their interests.

This is the agenda of a group of people (collectively the Committee) who independently know about DC and have been doing this job a long-time.

Fidelity’s report focusses on the things that matter to me, a DC saver and when I read it, I feel it has people like me in mind. I don’t have any savings with Fidelity, but this report suggests that those who have Fidelity as their workplace pension , are being properly protected and their savings maximised. There’s a video which comes with the report which you can access it here, it is reassuring if not that informative and it is good to hear the voice behind the words.

I have never heard Kim Nash speak before but I have imagined her plain-speaking is consistent digitally with what appears on the page – it is – thanks Kim Nash. Kim has consistently written clearly and well and this report continues that tradition, it is a joy to read and gets a green for tone and style.

Value for money assessment.

Rather than take issue with the FCA, the IGC has adopted the VFM principles which are now consistent with TPRs (Important as Fidelity also has a master trust run on similar lines).

I’m disappointed that the report doesn’t compare how savers have done. There are some tables that show the gross returns over various periods but these don’t make much sense to savers who want to know the impact of cost of charges and to see how their outcomes compare with those in other schemes (including had they been in the Fidelity master trust).

This is particularly important when the principal focus of the IGC is on the management of Fidelity’s default fund – known as Future Wise. I have looked at the 2022 version of Future Wise , a flyer for which can be accessed here.

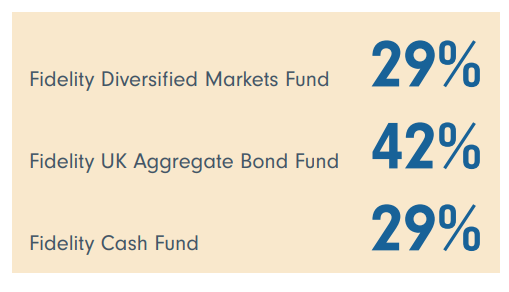

Right now the fund is invested for people of my age like this

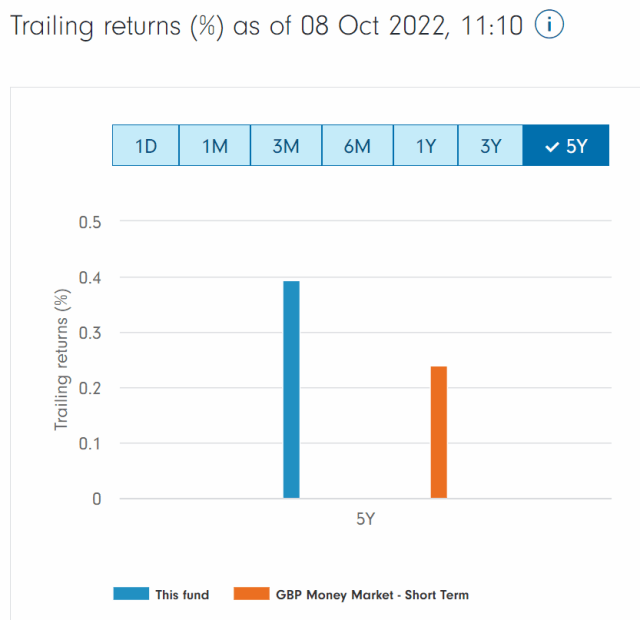

To give you an idea of just how important the allocation to these funds is, here is how the Aggregate bond fund has done this year (2022) (42% invested in Future Wise)

the Fidelity bond fund used in Furture Wise

And below is the return on that UK aggregate bond fund

And here is the return on the Fidelity Cash fund

You can see that all three funds invest close to their benchmark. But when you compare the three funds with each other you can see that the Cash fund would have made you about £400 on A £100,000 investment, the Diversified fund would have lost you £9000 and the bond fund (supposedly the least risky) would have lost you around £24,000.

Simply avoiding lifestyle and investing in the Fidelity global equity fund would have made your £4000

This strategy is designed to protect you in your later years of investment. Would the IGC in October 2022 have felt happy with FutureWise delivering these negative returns? Bearing in mind Fidelity’s aim for this fund is to protect people’s savings as they move into drawdown, conventional wisdom that bonds (and even cash) are safe – relative to equities – does not always hold true.

Turning the question round, if I had asked the IGC committee which of the asset classes would have provided best protection for their saver’s money in October 2021, I doubt they would have replied – global equities.

Fidelity has done well in surveys

As can be seen from the Corporate Adviser survey, Fidelity’s approach has worked progressively less well , the closer a saver gets to retirement. I fear that the tables to the end of 2022 will reinforce this.

My worry for the savers with Fidelity, is that the IGC is insufficiently challenging the value of Fidelity’s “conservative” strategy with its Future Wise Default fund and that by not focussing on the outcomes for their older savers, they are leaving themselves and their savers exposed to the problems we have seen this year with “de-risking” strategies.

I give the report an orange for its VFM assessment. It insufficiently challenges the assumptions made by Fidelity , which look to have got older savers in 2022 into a fair amount of trouble.

Effective?

In previous years , I have lambasted Fidelity for high transaction costs , and the IGC for letting this go. At one point the transaction costs exceeded the average annual management charge meaning people were paying more in undisclosed than disclosed charges.

This situation has turned around and I am not taking the credit for it – credit goes to the IGC for these numbers

I like the way the IGC lays out its stall on what it will be focussing on and I think it focusses on the right things – getting FutureWise right and ensuring that non-advised savers get the support they need – especially at retirement.

These are the things that the IGC can do and – with their skills – I expect them to do. I don’t expect them to get everything they want immediately, but I do expect them to exert their influence positively – all the signs are that they do. I give the IGC a green as an effective unit – lobbying for the “member”.