Two of my favorite journalists in agreement

Absolutely this! https://t.co/mqAFsXwS2H

— Josephine Cumbo (@JosephineCumbo) August 26, 2022

It is a disgrace that the Government is allowing an anxious nation no guidance other than the blandest of assurance that they will be alright.

Things are not alright.Test how you feel about the fuel cost rises and compare with twitter

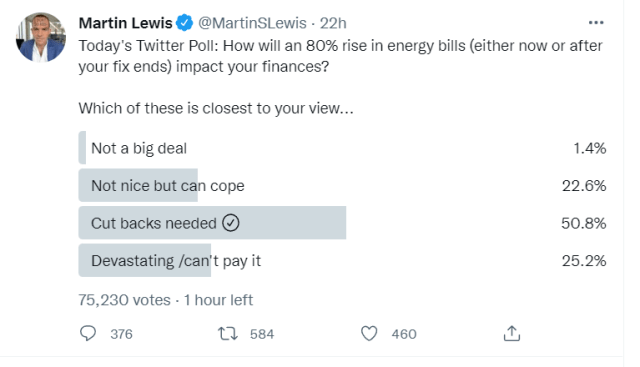

Today’s Twitter Poll: How will an 80% rise in energy bills (either now or after your fix ends) impact your finances?

Which of these is closest to your view…

— Martin Lewis (@MartinSLewis) August 26, 2022

Then consider the demographic who does not use twitter and certainly doesn’t vote on it.

For it is those people whose money we – in pensions – look after.

Our collective response so far, has been to warn savers that stopping saving will cost them dear in future pension rights.

This is not a good look for pensions.

For many schemes , rules, hard-coded into pensions software mean that people have a binary choice of paying a set level of contributions or becoming a deferred member, effectively preventing them restarting pension contributions till the next re-enrolment date.

We have come a long way since the days of capital units where people who stopped paying into their pensions found themselves with rights that were subject to a 5% pa charge, a way for insurers to recoup commission paid to advisers. In the old days, insurer’s main pre-occupation was to ensure “persistency” – many failed. Savers found their circumstances changed and were prevented from continuing a policy because they lost a job or moved to a job where there was an occupational pension. Some savers were so appalled by the lack of growth on their plans that they jacked saving in and many savers found it easier to cancel a direct debit for the pension than skip a mortgage payment or lose the chance to go on holiday.

But the idea of the “feckless” saver, only too ready to mess up the financial projections of the pension book, runs deep in the psyche of insurance companies. It is not so long ago that most personal pension policies carried a “waiver of premium” option, a form of income protection that insured “premia” – (the insurance word for “regular savings”) were paid by the insurer , so long as the saver was off work for ill-health. I remember being told to sell “WOP” and other insurances within the pension to improve persistency. At the first sign of a saver missing a contribution , my job was to terrorise them with the ill-consequences of losing WOP or DIS (death in service).

I mention this, because we are now witnessing the old entitlement among pension providers re-emerging. Pensions Expert’s article cites representatives of Scottish Widows, Legal & General and Canada Life, expressing concern that people may get smaller pension pots in retirement because they take a pension holiday today.

But preparation for the financial hardship people are experiencing is not translating into much more than words. Instead of making it easy for people to manage their finances by pausing pension contributions, we still want to lay on the guilt trip. We are robbing our future selves of a secure retirement, missing out on employer contributions and denying ourselves a return to the workplace pension till the next enrolment. This all reminds me of the tactics I used to stop people cancelling their “premia” forty years ago.

The way forward is not to revert to the past , but consider people today sympathetically. Opting out of a workplace pension is not something we do lightly, we do it with a heavy heart because we value our savings and we know the “free money” arguments.

Wake up and smell the coffee

What is happening to people’s finances right now varies. Take Martin Lewis’ poll and you will find a variety of responses, Many people will manage fuel payments out of income or out of savings.

But these findings, from 75,000 respondents should tell the pension industry that 3 in four people are going to need to cut back on discretionary spend and a quarter of all savers have no way at present of paying their bills.

The Government may find a way to ease the plight of the 25% who are devastated, but there is no certainty of that. These people need a plan B and that plan B should involve discretionary payments such as pensions.

Rather than talking them out of stopping saving, why aren’t we finding ways to minimise the damage. How can we encourage employers to continue paying, even when a saver can’t? How can we ensure that savers can return to saving when they can, rather than when rules let them?

It’s time to wake up and smell the coffee. In August 2022, savers don’t need to be told off, they need help.