The Financial Conduct Authority wants to encourage more consumers to invest through non-advised services in what it terms “a guided sales model”. There are rumours this could feature in the Queens Speech.

It has been discussing the potential development to encourage more people into investing with key industry players.

Money Marketing has learned the regulator is considering options on how to get more people to invest in “relatively straightforward products” by improving the consumer journey.

A document shared by the FCA and seen by Money Marketing, shows the intended direction of travel and how it differs to current market practice.

The proposals are linked to the regulator’s wider work on consumer investments and points to greater support for hybrid models, smaller fund selections and stronger nudges to help consumers make decisions.

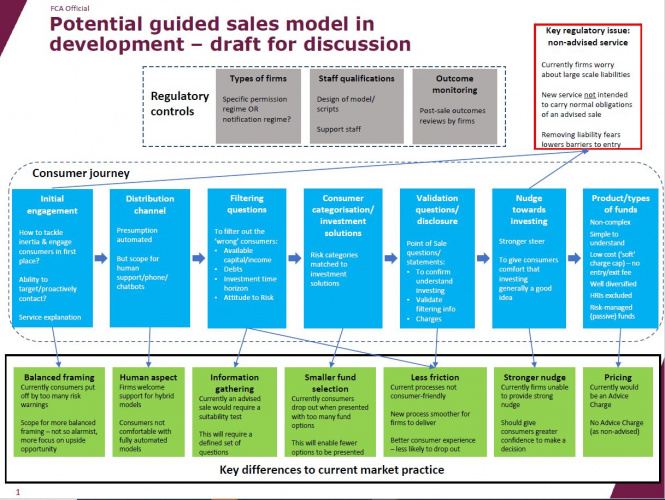

The FCA’s potential guided sales model in development discussion document

Source: The FCA

Money Marketing understands several providers have had conversations with the FCA about the document (shown above).

This is believed to have first been shared with some industry players in the summer of last year.

In its business plan for 2021/22 published in July 2021, the regulator set out its consumer priorities for the year ahead.

One such priority was to “enable consumers to make effective investment decisions”. It said it would publish its consumer strategy to set out its ambition for the market in early 2022.

Ahead of that, the FCA decided to publish more detail on its consumer investment strategy to explain the work it will be doing.

In September 2021, it provided information on its strategy and feedback received on its work in the area so far.

The FCA said it had set ambitious outcomes for the work and outlined it will “publish metrics to be transparent” about whether it is meeting these.

According to the regulator’s strategy roadmap, the FCA said it would review the regulatory regime to enable more firms to support more consumers to invest in straightforward products.

A consultation was pencilled in for the first quarter of 2022, with a policy statement expected in Q3.

Money Marketing gathers the guided sales document forms part of early engagement with the industry on this topic.

A spokesperson from the FCA confirmed: “As part of our consumer investments strategy, we want more consumers to invest their money when that is the right option for their circumstances. Many consumers find investments complex to navigate, and we want firms to support them through this journey.

“We are considering the best way forward for this work and we have been engaging with industry to gather their initial views on our developing approach. We are considering the feedback and will use it to inform our final proposals, which we will set out later this year.”

The draft discussion looks at the consumer journey and puts forward ways this could be improved.

It looks at how to make it easier for people to start investing. The regulator has previously expressed concern about the large number of consumers who have fairly significant holdings in cash.

The FCA thinks such people, who may not have quite enough money to pay for financial advice, could be better served to taking the first step to investing.

This could potentially be via direct-to-consumer investment platforms such as Vanguard, Hargreaves Lansdown, Nutmeg, AJ Bell and others.

Details of the document

The guided sales model document suggests consumers may be put off by “too many risk warnings” and outlines scope for “more balanced framing”, which is not so alarmist and could focus more on the upside opportunity of investment.

It also indicates consumers may not be comfortable with “fully automated” models and outlines the need for the “human aspect” with hybrid options.

The document states: “Currently firms worry about large scale liabilities. [The] new service is not intended to carry normal obligations of an advised-sale.”

The proposed move is expected to remove liability fears and lower barriers to entry.

Consumers would also be presented with fewer fund options to try to keep them engaged with the process, as currently too many options leads to many dropping out.

The FCA hopes a new process would be smoother for firms to deliver, which will offer a better consumer experience.

It argues the current process is not consumer-friendly and causes friction.

The model will be target-customer focused and is likely to include a defined set of questions to determine the best avenue for a customer.

Currently an advised sale would require a suitability test.

The approach would look to filter out customers not suitable to go down the self-investing route, such as those who have debt.

If the FCA’s policy statement is minded to take a similar stance, we could see more of a push towards low-cost passive products.

Stronger nudges may also come into play and there would be no advice charge as it is a non-advised model.

Consumers might still have to take a bit of a leap of faith without getting advice, but it may pave the way for opportunities for advisers later down the line if their needs become more complex.

This seems a slight shift from the regulator’s usual way of engaging in a piece of work of this scale. Often the first chance the industry gets to have its say is when a consultation paper is published.

“The only thing we learn from history is that we learn nothing from history …” (Hegel)

So: “According to the regulator’s strategy roadmap, the FCA said it would review the regulatory regime to enable more firms to support more consumers to invest in straightforward products.” Ah, yes, those ‘straightforward products’ – remind me, which ones are those, again? What’s the definition of ‘straightforward’?

I think that was what lay behind CAT standards, wasn’t it? And Stakeholder Pensions – the ones people could buy with out advice (except the FSA had to develop “Basic Advice” specifically for Stakeholder Products)? And what about the Carol Sergeant Review, which spent years with the industry looking at this – anyone care to guess how many straightforward products that Review came up with and what they were?

So, we’ve been there before, many times (many, many times …) and while people today may be a lot brighter than they were 20 years ago (I stress the word “may”), I would not like to guarantee that a “solution” to this “problem” will emerge.

“The guided sales model document suggests consumers may be put off by ‘too many risk warnings’ and outlines scope for ‘more balanced framing’, which is not so alarmist and could focus more on the upside opportunity of investment.”

I suppose if the risk warnings did not put anyone off, they would not actually be doing their job. Before we get too hung-ho about “guided sales” we should remember that many providers of products (not just financial ones) are highly adept at using behavioural economics to influence how consumers make decisions – and that “guided sales” is exactly that, a way of selling products, more products, to consumers for whom they may or may not be suitable. “Balanced framing” may tip the balance in the other direction.

“The document states: ‘Currently firms worry about large scale liabilities. [The] new service is not intended to carry normal obligations of an advised-sale.'”

“The proposed move is expected to remove liability fears and lower barriers to entry.”

Well, of course, that reduces the liability to the provider of the guidance, but it leaves the liability fairly and squarely with the consumer – and recent experience shows just how well fitted they are to take on this liability.

And finally – how is this guided sales process going to be funded? The idea of reducing barriers to entry implies that new entrants will come into the market (whatever that market is – is it a market for products or for guidance?). But how is the guidance to be funded? Are people who don’t pay for advice going to pay for a liability-free guidance? Or is it going to be wrapped up in the product price, just like commission?

And I have just come across this from 2014 – https://www.fca.org.uk/publication/guidance-consultation/gc14-03.pdf. A Guidance Consultation on that “advice-guidance” boundary. I don’t suppose anyone at the FCA today remembers that, though …