This article is for the advisers to small employers who are considering offering an auto-enrolment service, both to help the employer get started and to keep the employer compliant in months and years to come.

Of all the considerations, pricing is probably the hardest.

- Price too high and not only will you not get business, but you may prejudice existing customers against you.

- Price too low and you may find yourself incurring more cost than revenue.

- Adjusting pricing upwards or downwards is never helpful to a business, best to try and get it right first time.

In creating a pricing model, most intermediaries will take market soundings and establish what services other firms are offering, what they are charging and what customers are prepared to pay.

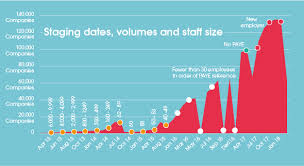

Clearly the larger the customer, the larger the budget and as customers are decreasing in size (a function of the staging calendar), so far pricing has fallen.

However, the size of employers is about to plateau, in future (nearly) all employers staging will have between 20 and 1 employee.

For these employers , there will be varying degrees of dependency for advice and intermediaries might consider a pricing model that offers tiered levels of service depending on the level of hand-holding needed.

To do this you will need to work out what services are you providing.

The Pension Regulator has established a ten stage process for an employer to complete the staging of auto-enrolment plan.

1.Mark your staging data in red in your diary

2.Nominate your point of contact to the Regulator

3.Find out who you have to enrol and what it’ll cost

5.Check your payroll know what they’re doing

7.Assess and enrol your workforce

9.Ensure your ongoing processes are in place

10.Complete your declaration of compliance

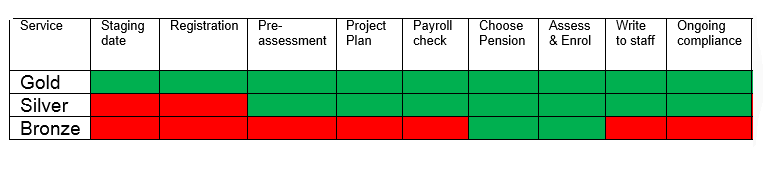

Could these be priced individually to help an employer select their own price? Some are quite easy (1,2 and 10 for instance). Some are difficult (notoriously #6 and 7) and some look harder than they are (using the Pension Regulator’s Project Plan tool makes 4 a doddle).

Presenting bundles of services priced on a gold, silver and bronze basis might mean hand holding on all ten (gold), those services “payroll dependent” (silver) and those that are establishing the pension interface (bonze).

Creating this matrix should enable bespoke pricing for clients wanting a tailored service. I would strongly suggest that any accountancy, bureau or IFA establishes on a time-cost basis an estimate of its cost of delivery for each part of its service.

Outsourcing the pension selection service

Where an intermediary does not feel competent to provide a service (such as helping a customer choose a pension) then the intermediary should investigate the cost of employing an outsourced provider.

This is particularly common when a “pension selection” service is needed. While many intermediaries are happy with a “pre-select”, where one pension provider fits all, many intermediaries are looking to provide a whole of market selection process using the research and selection algorithm of a digital service.

There are currently four such services to choose from

Increasingly we expect to see these services embedded into the payroll software service offering. It is worth checking with your software provider and with the selection service providers whether discounts can be achieved for bulk use.

Pricing the on-going service

Intermediaries can choose to price the initial work into an on-going service price or charge it as a standalone (implementation) fee. While it may look attractive to roll all initial costs into the monthly service contract, it may be less risky (and more transparent) to price for implementation and on-going service separately.

A customer has three ways to meet on-going compliance requirements

- Using payroll software

- Using third party software (supplied by the provider or independent middleware supplier)

- Doing the calculations and running processes on a DIY basis.

The market expects the majority of employers will manage the ongoing compliance using payroll software. But that a proportion will use options 2 and 3. Explaining that all three options are available may be sensible, customers generally appreciate the offer of choice and those who choose a DIY or middleware option, will probably have special needs for such an approach.

As with the pension selection process, intermediaries may wish to create an alliance with a middleware supplier where the payroll software simply isn’t fit for purpose. There are a wide range of middleware suppliers, the majority can be found in the CIPP’s Directory of Friends of Auto-enrolment.

Getting the messaging right

Employers are likely to approach auto-enrolment with trepidation. Providing a pricing plan that explains what is important, how much it will cost and how an employer can choose a service that’s right for them will ease the tension.

Approaching pricing in the way I’ve outlined is likely to go down better with your customers than a “finger in the air” approach. What’s more, it will make your service market leading for prospective clients shopping around

Fantastic article Henry. You are definitely right, one of the biggest decisions for any adviser is getting the pricing right. This can be difficult enough for well, established compliance services being provided, such as preparation of accounts or tax returns.

How do you price a new service, which you and your team have no experience of?

Whilst the key is value pricing, you are perfectly correct that the starting point is looking at the services you will provide, create different price bundles to allow clients to choose the bundle and a price that suits them the most.

We know that this may be difficult for many advisers, especially those just breaking into Automatic Enrolment and so we have created a FREE Pricing Pack, which includes the bundles of services that Henry mentions, a marketing brochure and a spread sheet calculator. The calculator allows you to create your own price for each service, but as a starting point we have included a suggested price from. We will be giving this FREE Price Pack to anyone attending the Automatic Enrolment room presentations at the AVN National Tax Conference on 23rd September.

And because we know Automatic Enrolment is a huge issue for employers and a significant opportunity for our profession to truly help our clients and increase loyalty, we are inviting anyone in payroll to attend for FREE http://avnconference.co.uk/article3.html.

Thanks Ian.

I hadn’t come accross AVN before but it looks like you are doing a useful thing for payroll. Hope the conference goes well and that you can use some of the ideas in this article in helping accountants and payroll price their services.