Every so often we get asked questions by people to whom the answers really matter. I’ll leave you to guess who might be asking these ones!

a)Is there really a problem for unadvised small and micro employers to understand the market and identify pension scheme(s) suitable for them?

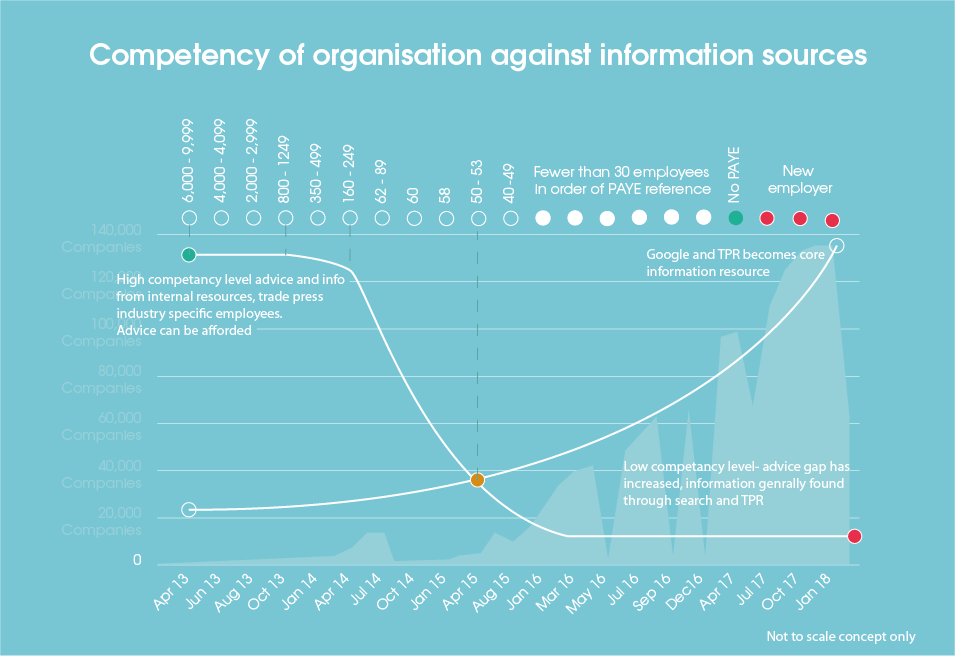

We think there is and your research confirms ours. The economics of commission based distribution meant that most companies staging up till now had a workplace scheme but as we move into the back end of 2014, the percentage with a workplace pension reduces alarmingly. (see chart below)

What schemes are in place for smaller employers are often uncompliant with the post 2015 qualifying rules (e.g. commission, AMDs, lack of governance, high charges, no default, and restrictive entry). The problem may be worse than your figures suggest as so many small schemes won’t be fit for purpose

A google search on “choose a pension” calls up a handful of providers, TPAS and tPR. Pension PlayPen is not advertising on this phrase but manage to appear 5th on the google list after yourselves, CAB, this is money and the FT. This suggests we are the primary commercial site for this kind of search.

Short of answering the ads of L&G, NOW and Standard Life there is no way of assessing what is out there!

b) Are there already solutions to this problem out there suitable for small and micro employers?

The great thing about advising on workplace pensions is that the advice is unregulated!

It is quite extraordinary that with such freedom, there is virtually no comparative advice on workplace pensions to be had.

We know only of only one product and it’s ours! http://www.pensionplaypen.com (choose a pension- CAP) which attempts to provide the complete service detailed below. We are “inside”partial services such as Chris Daems’“AE in a Box”and HR Essentials’“AE project management service”.

80% of our business is referred with the majority of referrals coming from accountants and IFAs. The market is moving towards us, we have not got the time, resources and muscle to promote ourselves as we would like to. But so far in July we have picked up 4 national awards as the media begin to “get it”.

http://www.pensionplaypen.com is often referred to as “employer facing” and this is true. But we have over 500 intermediaries registered on www.pensionplaypen.com with numbers increasing by 50 a week.

So what are the alternatives?

Many employee benefit consultancies will offer a whole of market broking service but at a cost of several thousand pounds – assuming a bespoke service to an employer.

Some consultancies are offering vertically integrated products which are promoted ahead of an open market option- some IFA networks (notably Lighthouse) are also offering house solutions.

Principal IFAs suggest NOW, NEST and Peoples as Providers who will accept all employers and Pension PlayPen for those who want to make a whole of market choice.

Our discussions with SimplyBiz, Intrinsic, Openwork and Sesame suggest that middleware is more important to them than the workplace pension and there is still regulatory confusion about when advice on workplace pensions needs to be regulated. Regulated firms seem to consider non-regulated work outside their remit!

The same problem occurs with many of the accountancy firms we speak to. For them, the issue is whether as non-regulated organisations they should be even talking about – let alone advising on- workplace pension selection.

c) Could existing products or services be made more effective/adapted to address the needs of small and micro employers, e.g. could advisor-facing products be opened up to an employer audience?

The products created for advisers by F&TRC and Defaqto aim to add value through the depth of analysis of product features. There is little alignment with what tPR considers the characteristics of a good scheme, nor is there much alignment with what customers want (referring to your research).

Most advisers are still considering workplace pensions from a sales perspective (concentrating on maximizing contributions rather than focusing on outcomes).

A portfolio of 4 or 5 GPP’s with 50-100 members was all an IFA firm needed to have a successful department. They focused on this sweet spot of the market.

Very few IFAs marketed to smaller SMEs or micros as this was not cost effective.

No IFAs have developed automated selection tools which we consider necessary to deal with bulk enquiries. They have concentrated on providing AE support services which replace the annuity income lost from trail commission.

While writing this paragraph an enquiry arrived from an IFA. We quote it as it demonstrates how far IFAs are from advising on workplace pensions

We wanted to get in touch reference your auto enrolment “playpen”(sic)

As you could probably guess this (AE) is an area we are also working in, both for existing and potential new clients.

Our proposition deals with implementation and where required ongoing advisory services for the pension members via our IFA company. Appreciate there may be some overlap but wanted to ask as to whether there was scope for us to forge some form of alliance in having an informal arrangement .

IFAs are looking for long-term relationships with a small number of high-value clients. To properly deal with 1.2m new employers they should be offering a light-touch automated service at low-cost with no obligation for the employer to see them again.

We fear that the two models are mutually incompatible.

We have no cross-sell to the 350 employer who have used our service –indeed we don’t even contact them post sale unless they ask us to.

d) How could visibility of those products best be increased among the diverse population of unadvised small and micro employers? Please let us know if you think there are any barriers to increasing visibility to this sector of the market.

This is our big challenge. We recently met with the head of BBC economic affairs, Hugh Pym. Hugh was under the impression that the only scheme you could use for auto-enrolment was NEST. Clearly issues about choice are not confined to micro employers!

The obvious route is to invest heavily in google though we think that only a small percentage of employers will buy in such a random way.

Assuming that IFAs don’t get their act together (and we see very little appetite to advise on a product with such little certainty of payback, then the next stop is the accountants and HR specialists

Websites such as www.accountancyweb.co.uk and www.hrzone.co.uk , publications such as Payroll World and the various online groups that they spawn are the ideal places to get brand penetration so that micros know the name.

However there needs to be an enormous amount of trust building between the pension providers and payroll, HR and finance functions. Our experience so far suggests that most accountants do not think they can advise on workplace pensions full stop. Until that impression is dispelled (and it’s not being dispelled by ICAEW) then it’s hard to see most practitioners helping in choosing a pension.

We don’t see the majority of small business groups being able to do much more than bring people together (and even here the numbers who attend pension meetings are very small). The Federation of Small Businesses, of which we are a member, seem to see AE as a revenue generator and a chance to promote their in-house IFA.

We would be interested to know how successful they have been with this model but suspect that these organisations are not proving the turnkey some thought. There is resistance to the fees necessarily charged to advise face to face on a bespoke basis.

The scaremongering story that the Pension Regulator is going to fine you £10k a day is a lot easier to market than the long term benefit to an employer of getting the workplace pension decision right

e) What would the appropriate level of scope and sophistication be for solutions for small and micro employers who want to choose a scheme without the services of an intermediary?

We’d like to say www.pensionplaypen.com but we are clear we haven’t cracked it yet. The big issue won’t so much be the AMC but the on boarding costs between providers.

The insurers are now mostly charging for implementation and ongoing services on top of the AMC and this is providing a propulsion of new business to NEST, NOW and Peoples which are free to use.

The second major issue is the support for AE from the provider. We are finding that employers are flexing the weightings for admin and payroll support “up”and depressing the weightings of member-centric product features (investment, at retirement services).

We worry that members will be asking employers the criteria for the decision taken “cheap and easy for us to use”may not be the answer the member wants to hear!

We think the scope of any service must include

- A means for an employer to do a workforce assessment and model the cost of contributions under the various certifications, phasing and salary sacrifice

- A means to understand what providers will offer a quote and a means of understanding the nature of that quote

- A means of comparing one quote against each other- we use a balanced scorecard

- A way of recording the process into an audit trail which can be used now and in future to justify the decision

- A simple means of kicking off with the provider- ideally with an API to minimize fuss and bother.We think that the service must have the capacity to deal with sophisticated employers (we offer pretty well the whole First Actuarial analytics if needed). But it must be presented in such a way that it is idiot-proof and doesn’t intimidate and drive-away SMEs and micros without any pension sophisticationThe Answer of course comes with experience, our own analytics tell us when we are getting it wrong and every iteration of our service is close to what the customer needs and wants.

- You hear

- Just look at what the public need and how it plays in the Provider’s Boardroom

- There is a system that addresses this problem- we own it! The hardest bit for the pensions industry is to rid itself of the conflicts that stymie innovation.

- f) If you don’t think the market will or can address this problem, why not? Please indicate whether these are purely commercial considerations or other more basic/fundamental considerations

- Simple practical steps on how to choose a pension scheme without having to understand scheme types The Provider hears

- You hear

- “we’re losing our brand here – our USP is our marketing and this is driving a coach and horses through our sales and marketing strategy”

- Practical questions to ask to ensure the scheme is suitable (e.g. can I buy it direct, will it do everything I need to do)The Provider hears

- You hear

- “this means people rating what we do and calling us on our deficiencies – we’ve always had control of what people said about us- that’s why we had direct sales forces and had the IFAs in our pocket- this is too scary”

- Shortlist of AE schemes available to themThe Provider hears – “so we’re supposed to advertise our rivals when we’ve got these employers eating out of our hands – forget it!” You hear

- Ability to compare charges and any employer fees of shortlisted schemes

- You hear

- The Provider hears “margin erosion”– we’re not having that!”

- Ability to compare wider AE support offered by scheme (e.g. workforce assessment , communications to workers)

- The Provider hears“which means pitting our auto-enrolment hub and supported middleware against integrated payroll solutions”

So we think that there is very little appetite from the pensions industry to help here. These conflicts make it impossible for the ABI, frankly the NAPF aren’t at the races, our conversations with Unbiased don’t suggest they are planning on building anything for the IFAs (a cottage industry) and none of the major pension consultancies are interested in sharing their prized intellectual property. As one partner of a rival firm wrote to us

“Frankly you have to be mad to try. The chances of getting your fingers burned are high, development costs are high, the skills needed to offer something as simple as needed without compromising our integrity just aren’t there”

Nor are commercial organisations going to endorse an organization like ours without wanting a finger in the pie and the pie has not got enough fruit in it to warrant fingering.

The price people will pay for a choose a pension service is driven by need. At the moment employers do not feel they need to choose and so plump for whatever claims to sort out the problem.

If advisers and accountants continue to duck the pension selection issue then it’s hard to see how things are going to improve.

It would be helpful of Government to do something to promote choice. NEST is a net beneficiary of “no choice”and we can understand the DWP wanting NEST to pick up business (it has a debt to be settled).

But NEST is not the only fruit and we want other master trusts and insurers to be properly represented

So some kind of market intervention is probably needed.

This post was first published in http://www.pensionplaypen.com

If you have small children and want to visit an amusement park they can enjoy, check out Legoland California in suburban San Diego.

Bob, give me a boost, I see a lot of aluminum cans in this dumpster — 2.

I’m telling you, B-Rex is a genuine Jayszoo-Johnny-One-Note and damned proud of

it’absorbed by it ‘virtually reeks of it.