Pete Glancy

In this blog I take issue with Pete Glancy and his premise that we have a “decumulation dilemma”. We have no such thing, we enter into a pension scheme to sort out our pension dilemma, it is the provider of such “pensions” as the Scottish Widows Master Trust and the Scottish Widows Group Personal Pension to sort that dilemma out. It is not our dilemma – it is theirs. My comments in blue.

In advertorial in Corporate Adviser , Pete asks;

Is a retirement income about flexibility, certainty, legacy – or a mix?

The simple answer to that is that a retirement income is a pension , something we buy when we give our money to a pension company for management of our wage in later age.

Auto-enrolment has delivered a robust and well-established pension saving model, but the pension income side of things is less well developed.

This sounds like an admission of failure by pension companies but turns out that the guilty party is the saver!

Those who can’t afford the services of an Independent Financial Adviser will undoubtedly struggle to construct their retirement income in a way which meets their needs and those of their family, and last them as long as they need it to.

There are some huge premises here. First that those who have money, will pay for advice on something they have already bought, the second that those who don’t pay up are consigned to the damnation of not meeting the needs of their family – becoming a burden on them in later age! Laying guilt on savers for not doing their own pension is a bit rich, from a man whose job it is to get their pensions paid!

Meanwhile, policy makers are still working through regulatory and legislative approaches which will determine what is, and isn’t, possible in the future.

Excuse me if I cough, but the Government’s statements are very clear, the Pension Schemes Bill will require pension schemes to provide a pension from the pot ,by default and as a choice, how much work is there to get your head around that?

Asking 1,500 retirees what they want from a retirement income – using plain English and avoiding complex product terms – has helped us shape our new ‘Decumulation: Understanding the Needs of the Nation’, report. It looks at what people want from their retirement income as they weigh up flexibility, certainty and, for some, the importance of leaving a legacy for their loved ones by passing their pension on.

Yes indeed, 80% of the 1500 said they wanted a consistent income that lasted as long as they did, exactly what the Pension Schemes Bill demands. People want to know that the money they use to purchase this pension will go to their family if they don’t last long enough to get it back – why not? It’s what Q-Super has been doing in Queensland for some years. So what’s the problem with giving them what they want, Pete?

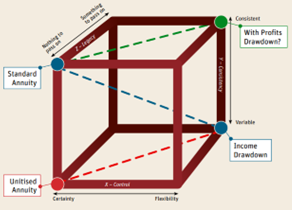

Mapping their needs and wishes onto a simple model in the form of a 3D cube (pictured, below) captures this in a more visual way which hasn’t been possible before.

Why do we need a model to explain what is wanted? Whoever said they wanted with-profits drawdown, standard annuity, unitised annuity, income drawdown? These are phrases dreamt up by insurance company marketing departments and disseminated by policy geeks, they are not phrases that anyone has ever used, let alone products that the 80% are asking for. They describe and ask for

a pension with cash back on early death.

Retirement matrix

We’re calling this a Retirement Matrix tool which allows current products and any new potential ones to be mapped onto a simple 3D cube.

This 3D cube isn’t simple at all, it is more like a Rubrik’s cube, easy to unpick if you are Pete Glancy, Robert Cochrane and all the other folk at Scottish Widows but totally baffling to me and everyone else! It seems to visualise a load of trade-offs between products that we now have to consider because the financial services industry has built them. We need to do this because of the premise that it is us and not Scottish Widows who have to design , build and operate the pension they promised us

Simplifying things visually is designed to make considerations such as default decumulation options and the potential role of Collective Defined Contribution (CDC schemes) easier to envisage. It also better illustrates how products currently in the market might be used to best effect.

CDC is a non-guaranteed pension, it lasts as long as we do. Annuities are guaranteed pensions supplied by insurers , occupational scheme pensions are guaranteed by sponsors or capital, all are designed to last as long and our partners do. All provide a high degree of certainty but do so in slightly different ways. Take your pick which one you offer as your “default decumulation option”, Pete – just get on with it.

All retirement income products have attributes which sit on three distinct but interconnected axis.

- On the ‘Control’ axis: a product can facilitate flexibility of expenditure at one end, and the guarantee of income for life at the other.

The language of the doom loop – “facilitate flexibility of expenditure”! What can be more flexible than a quarter of your pot sitting in your bank account to spend as you like? 80% of your customers have told you that they want a consistent income paid to them as long as they around- they are paying you to pay them -Pete!

- On the ‘Consistency’ axis, a product can smooth returns over time so that income is predictable throughout retirement for budgeting reasons; or at the other end of that axis can be invested to seek higher levels of income but with a risk that the income in retirement might fluctuate.

People want to get paid a pension Pete, they don’t want to buy a product that depends on markets to decide how much they can spend from month to month. A pension is fixed, even a CDC pension is fixed (it just wobbles a bit!). How many people think of a pension as a “product” anyway?

- On the ‘Legacy’ axis, a product can facilitate benefits for dependents if a customer passes away early in retirement; or can exclude those benefits to secure a higher income for the owner of the pension pot.

With the best will in the world, people understand these trade offs. People who make decisions on how they take occupational pensions take these decisions all the time and they don’t struggle because they haven’t got a financial adviser, they work out what they want and then they ask for it and the pension gets paid with or without tax-free cash, where their are dependents to protect, dependents tend to get protection, almost all the decisions are done for us. All most people have to do is to fill out the form to say what bank account the money should be paid to.

Our new report ‘Decumulation: Understanding the Needs of the Nation’ (PDF, 7MB) not only creates a tool which allows the product landscape to be set out more visually, but it also allows customer demand to be captured in a way which hasn’t been possible before, with that demand then overlayed on to the model.

The report is great, its findings I quote it every day. It validates everything the Government is saying, everything AgeWage has been saying, everything that Pension SuperHaven is paying.

We see that 80% of customer demand sits on the left-hand side, which signifies an ‘income for life’. The 70% of demand sits in the back wall and reflects a desire to pass on some pension wealth were customers to pass away early in retirement. Then there’s the 55% sitting on the roof on the cube which signifies a desire for a predictable income from one year to the next, for budgeting purposes.

Pete, you are in the business of advising Scottish Widows on what they should be doing, they don’t need your cube, they just need to get on with paying people pensions that provide a predictable income, protect the family and last as long as they do. The rest is just noise.

What’s the conclusion?

Most demand sits at the back left of the cube, where needs could be met for example by annuities with guarantee periods, whether these be level, indexed or variable annuities. Yet these products currently play next to no role in retirement income.

This is feeble thinking. People up and down the UK are being paid pensions which aren’t called annuities. Those pensions are invested for the future in productive assets and are considerably more efficient (we find 10-15% more efficient) than annuities. Just because the insurance industry sells annuities (as their way of paying a pension) doesn’t mean we have to buy one. Why can’t we buy an occupational pension instead? No reason at all, infact you can buy pension with your pot when you join local government and you’ll be able to buy a pension pot with where Pension SuperHaven is inside your workplace scheme.

Decumulation-only CDC is a discussion point in the public policy space. If you say so Pete, I thought it was a way of paying pensions to people with pots

‘Whole of Life’ CDC doesn’t permit smoothing of returns over time or death benefits. These restrictions would limit demand quite considerably if applied in the future to Decumulation-only CDC, making that a niche product.

It’s not a product, it’s a pension (see above) and it’s not happening any time soon.

If any future rules facilitating Decumulation-Only CDC were sufficiently flexible to permit the smoothing of investment returns to deliver predictability and allowed for any element of death benefit to meet the ‘legacy’ need, it’s likely that customer demand would be significantly greater.

I would like to draw readers to the complexity of that sentence. Of course you could design CDC with a cash-back facility, Q-Super has done so in Australia.Very few people are buying it – but that’s a different story.

We can see, however, that customer demand is all around the cube. This tells us that there isn’t a single product that could easily be used by Trustees in establishing default decumulation arrangements in the future and that a more sophisticated framework will be needed.

This is total rot! 80% of people have told you they want the same thing, go ahead and give it them, if you won’t do it yourself, talk to me and I’ll do it for you

Everyone is different, and it’s likely that combining more than one product appropriately will be closer to the retirement income needs of many people.

Everyone isn’t different, your research suggests that 80% of people want the same thing, they may spend their pension differently but 80% of your customers want a pension paid for as long as they live (with cashback if they die early)

IFAs are skilled at helping people combine products in this way, but not everyone can afford their services. We need to help people who are less affluent benefit from these same outcomes, but we don’t yet have all of the tools.

You do not need an IFA to get a pension. I dare say that Pete has a Scottish Widows staff pension coming his way. He can decide whether he wants tax free cash and when he wants the income to start, the rest is done for him.

What is needed is simple Pete, what you are offering is way too complicated. Let’s have a word.

Clearly if you don’t know who is underwriting the risk …it’s you