My twitter feed is full of invective from financial advisers who are up in arms that I am passing myself off as a financial adviser. Page after page of lectures and just when I think it’s dying down , Paul Lewis will throw another hand grenade into the pond.

I certainly am. I advise people about their finances in print, on air, and even personally in meetings. It is all not only lawful but very useful. You are confusing financial advice with regulated financial advice.

— Paul Lewis (@paullewismoney) February 19, 2023

I don’t give regulated financial advice , but it you want my non-regulated financial advice, spend your days doing productive work and not on twitter.

Paul Lewis is of course one of the most read, watched, listened to and respected people talking about money. He doesn’t have the reach and influence of Martin Lewis but he adds a lot more value than twitter feuds over whether Henry Tapper is a financial adviser, ever will.

I feel a little jaded with social media. Despite me being elevated into the pantheon of “successful group admins” by linked in, I am now less than a week away from hitting my 30,000 connection limit after which I have to start disconnecting to connect, a stupid waste of time which serves no useful purpose.

Facebook has become a miasma of unwanted approaches from devout evangelicals and young ladies intent on showing me their nipples and more.

So for entertainment, I have been filtering the comments of the now 255 Money Mail and This is Money readers who vie with each other for the best rated comment on Tanya Jefferies and my post on how to ditch your useless financial adviser.

Despite howls of indignation when I mentioned this on twitter, I think it would be salutary for all IFAs doing their “consumer duty” work, to read what the general public think of their professions. I am sure that none of the comments would apply to their practices but if they want to know what the disaffected punter would look like (knowing that such people are other practice’s clients), let’s look at the top 10 rated posts

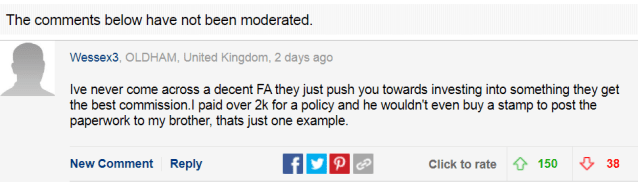

In top spot is Wessex3, – exiled to Oldham and very grumpy.

Revving up behind is Kawasaki Versys who like Wessex3 is unimpressed by the VFM on offer from the IFA.

Interestedx gets more mixed reviews – I note a hardcore of disapproval of around 30 – suggesting an IFA fan club). Clearly some people haven’t been carrying out their RDR research – tut tut.

A more positive approach that earns him only 8 negative ratings is from Andrew from Derby. His comment should send a shiver through a few fund picking IFAs as they contemplate their value assessments.

Planter Punch from Deadwood USA, understandably has a flag thrown at him for his dubious provenance, but the story sounds plausible , much to the son’s disgust.

We have to get to #6 before we see some support for an IFA (with a flag thrown). It’s nice to see the sixty somethings don’t see themselves as wealthy but still get advice they value.

Sir Sparky picks up on my kind words for SJP. One thing that seems to unite IFAs , their clients and the fully disgruntled is a dislike of SJP. It is amazing that SJP keep going, let alone prosper as they do.

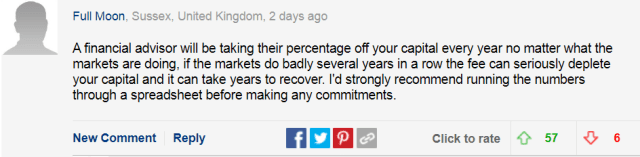

Full Moon picks up on one of the bete noirs of the FCA – the unwarranted ad valorem fee where remuneration doesn’t seem aligned to success – simply to funds under advice.

Finally, my personal fave; Tamla Motown manages to combine brevity with wit and squeeze in at #10.

Hello Henry,

Comfort yourself that you are having an effect… which is far better than nobody commenting. At least, from the relevant comments, you can gauge whether you are correct or not i.e. market research, if you like. Obviously those who are ‘hurt’ by your comments will scream.

Incidentally on Moneybox this weekend, a Professor Crawford Spence, of King’s College, London was interviewed. Apparently the College approached 69 Managers of Actively Managed funds for research purposes. In that research ten percent voluntarily advised they they (the Managers) invested their own funds in Passive funds e.g. Index-linked. Professor Spence gave statistics to support their view.

Elsewhere I have read that the European Court of Justice has recently ‘struck down’ the right of public access to beneficial ownership registers. The grounds being that such access was an interference with the fundamental rights to respect for private life etc. i.e. those set out in the EU Charter of Rights. Apparently a ‘second such ruling that will severely limit corporate transparency and the ability of authorities to unmask financial crime’.

It reads like an open door for, say, another LDI scheme and further savings fund disappointments.

Kind regards,

Tim Simpson

Henry, it would be good to know how wealthy are those people.

Many people think they have a clue, but they in fact do not even know the basics.

They cannot even explain why markets go up, or the difference between speculation and investing.