|

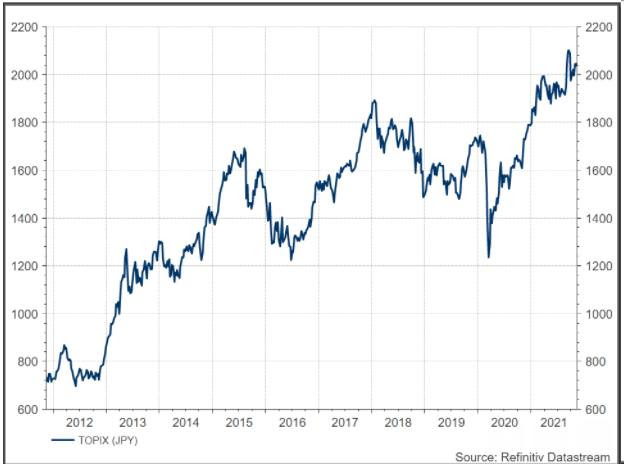

Japan’s stock market has almost tripled in nine years! Even typing that sentence feels weird to me, because the Japanese market has been the punchline to Wall Street jokes since at least 1990, when that country’s epic bubble burst. For 30 years, brokers and fund managers have been pounding one table or another about how Japan had great companies trading at low valuations. International investors have taken stakes in moribund Japanese groups and pushed for western-style shareholder-friendly reforms. A few have made money. Most have been punched in the face and sent packing. And the joke is not quite over yet. Convert that happy little chart from yen to dollars and add the S&P 500 and the MSCI World, and you get this unhappy little chart (all three are rebased to 100):

And, of course, the longer-term story for international investors in Japan has been just awful. Here is that last chart again, this time back to 1975:

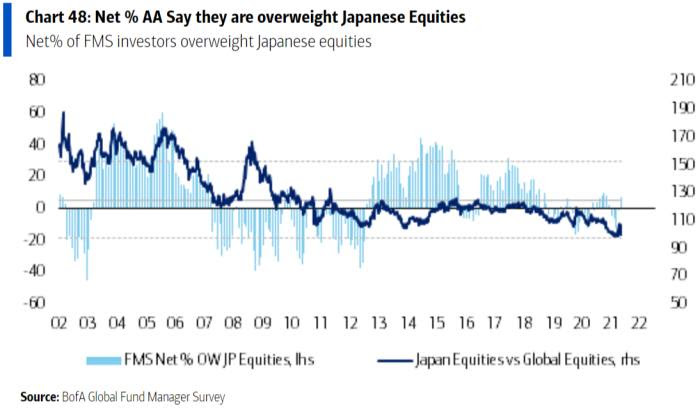

Long experience and recent performance has left global investors very skittish about putting big bets on Japan. This chart from Bank of America shows (in the little light blue lines) the net percentage of managers who are overweight Japan (that is, the percentage who are overweight minus the percentage that are underweight). The dark blue line is a dollar-based performance measure of Japanese stocks relative to global equities:

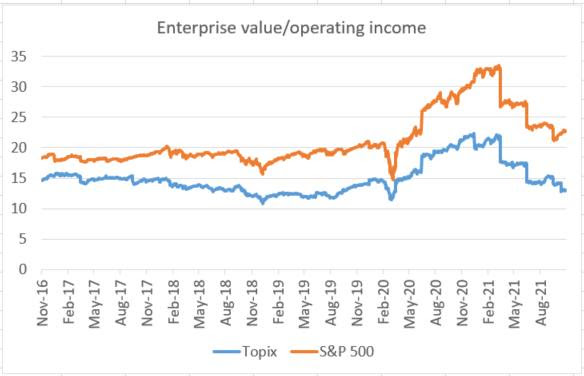

A net 7 per cent of managers say they are overweight Japan (the current figures for the US and Europe are 16 per cent and 34 per cent respectively). Several years of sustained interest that began in 2012, coinciding with the start of Abenomics, has all but disappeared. Underperformance has, of course, left Japanese stocks looking enticingly cheap. Almost half of the Topix trades at less than one times the book value (and more than half the index has no net debt). Below are enterprise value/Ebit ratios for the Topix and the S&P. The Japan discount is presently 50 per cent above its five-year average:

But, again, this is an old story. Valuations are the siren song that has led generations of investors into what turned out to be a value trap — a relatively cheap market that proceeded to get relatively cheaper. But at some point things might just change, and the better (not to say good) performance of Japanese stocks in recent years suggests that the tectonic plates could be shifting. Even the recent solid-but-not-great performance comes with a caveat: it was heavily state-supported. Since 2013 the Bank of Japan’s quantitative easing programme has included the purchase of domestic equity exchange traded funds. The BoJ now owns ¥36tn ($313bn) in stocks (or about 5 per cent of the total capitalisation of companies on the Tokyo exchange). But the bank all but stopped buying ETFs back this spring. In addition, in 2015, the huge Government Pension Investment Fund said it would double target allocation to Japanese stocks, which had been 12 per cent. The reallocation is complete. As of last year 25 per cent of the fund, or ¥47tn, was in domestic stocks. So the demand previously supplied by the BoJ and GPIF needs to be replaced if Japanese stocks are going to take another leg up. The obvious candidate is international buyers in search of value. But they need a compelling narrative to buy into. Valuation is never a sufficient reason to buy. Pelham Smithers of Pelham Smithers Associates makes the case that there is an exceptionally strong market within the wider Japanese stock market. “Aggregate performance has been very poor, but vast swaths of the market have performed exceptionally well,” he says. Smithers points to the great performance of various actively managed Japan funds as evidence (to pick one example, the Baillie Gifford Japan Trust has appreciated 440 per cent in a decade, in pounds). But can the market as a whole finally perform? “The question is whether the clunkers have fallen enough that they can’t hold the market back any longer, or whether the world-beaters have become too expensive?” Smithers says. He thinks the answer to the latter question, at least, is no — citing as an example Tokyo Electron, an outstanding semiconductor company that trades at a big discount to US peers. Another case for buying is that, after years of resistance, corporate Japan may be putting a slightly (slightly!) higher priority on shareholder value. The break-up of Toshiba — which may lead to the sale of one or more of its units to private equity — is the most prominent example of this. It raises hopes that other sclerotic conglomerates will break up. Toshiba may be a special case, however, because of its history of scandal, heavy foreign ownership and the political sensitivity of its nuclear business. Mizuho Securities points out that since tax incentives for spin-offs were introduced in 2017, only one company other than Toshiba has taken advantage (Koshidaka Holdings, an “operator of karaoke rooms [and] fitness studios targeted at middle-aged women”). Yet Toshiba is not completely alone in shaking things up, as my colleague Leo Lewis has pointed out to me. OK Corp, a supermarket operator, is in a bidding war with one rival, H2O Retailing, over another, Kansai Super Market. Shinsei Bank is fighting off a hostile takeover from the internet brokerage SBI. An activist hedge fund from Singapore is getting in the middle of a deal between the energy company Eneos, one of its subsidiaries and Goldman Sachs. For those — like Unhedged — who hope for a fuller embrace of shareholder capitalism in Japan, these are just glimmers of hope. But change has to start somewhere.

|