The Aviva 2021 IGC report is an accomplished document that sets standards in certain areas. It is the first IGC document I have read that excited me about ESG and its analysis of the provider’s investment pathway proposition is also first rate.

The tone of the document is friendly – almost intimate and the Chair’s opening comments and the explanation of the way Aviva got through the early months of the pandemic are genuinely interesting.

The document is well laid out and easy to navigate.

But I have issues with the sections on investment and the attitude of the IGC to FCA’s proposals to make IGCs more effective. Though this is a good read, I am not sure it is quite as independent as the composition of the committee would suggest.

The empty chair

The report begins with what I think is a joke. The chair sending the message, like almost every office chair in 2020 – is clearly out of the office.

This is not the only moment of humor in the report. I enjoyed this wry observation in the section on Aviva’s response to the pandemic

We have also seen evidence that the average length of

calls increased significantly with customers spending

50% longer speaking to an Aviva call handler than in

2019. That could be due to an increase in complexity of

the call but could equally be that people were just

happy to have somebody to talk to.

At the end of the report , I enjoyed this personal touch.

It’s a long report at 90 pages, but its style and personality carried me through.

Value for money assessment

Inevitably, the IGC’s verdict is that value for money is being offered to most savers.

nearly all of you are receiving good value for money and for many of you very good value for money.

Which is comforting so long as you can identify yourself as getting good or very good value. The trouble is that it is far from obvious who is getting what.

It seems that investors in the “my future growth” default have got since 2015 , returns of 10.7% while other funds have delivered over the same period between 14.7% and 7.1%.

This range of returns in what are all bracketed as multi-asset funds suggests that what savers are getting out of Aviva investments is down to the default they find themselves in.

With the best will to the IGC, I don’t think these tables show any such thing. They shoow that there is a lack of precision in the statement “nearly all of you are receiving value for money” and this needs addressing.

The benchmarks seem to have been picked at random and the reader expected to make sense of this information, in truth , most readers stare at these tables with blank incomprehension and we wonder why people don’t engage with their pensions!

But where I lose my confidence with the IGC’s even handedness is when I look in detail at comparison performance with other workplace pensions.

These comparisons show the Aviva funds in a good light, but they are not necessarily comparisons with other defaults and they are not comparing returns with the defaults of master trusts.

This selection is at best random and at worst is painting a false picture of the value that Aviva investors are getting.

Since members are primarily reliant on investment performance for good outcomes, it is important that we understand this performance in terms of the outcomes given. In the case of these tables, we aren’t even told if performance is net or gross of charges.

This lack of focus on the context of these funds worries me. It worries me too that the IGC are prepared to accept this state of affairs

Aviva provided us with details of transaction costs for

all of the investments available to you. These showed a

significant variance in transaction costs with a range

varying from a negative cost to a charge of over 2%.

The costs for Aviva’s own default funds were at the

much lower end of the scale as can be seen in the table:

Let’s be clear, all funds on an Aviva Workplace Pension Platform are Aviva’s funds whether they are managed by Aviva Investors or not. The responsibility of the platform and of the IGC is to protect savers from harm. If there are funds with 2% pa transaction costs on its platform, then some savers are very unlikely to be getting VFM and should be told so.

Have they been?

Effectiveness

There are wins for members as a result of the IGC’s work. They have clearly renegotiated charges on investment pathways and the report is bringing to light anomalies within the range of defaults which should alert employers and advisers to ask serious questions.

But for all the jovial tone, the report is light on serious action to address these issues. Instead of looking in detail at the outcomes arising from the range of defaults, they are entrusting a study of how savers are faring to a study of each others reports and the work of a pensions consultancy. This is the IGC’s response to the FCA’s proposals that member outcomes are compared against those in other schemes.

It is likely that new rules will require us to assess value

against other providers using information that is

publicly available. This is a challenge and will likely be

a comparison between other IGC’s reports. However,

we are exploring also other sources of comparable

information: to help facilitate this we have agreed to

participate in a benchmarking exercise with Redington,

an independent investment consultancy, which will

allow us to compare Aviva’s offering against other

providers in a number of areas. The exercise is

designed to compare certain groups of employers of

similar size to understand if they could potentially

receive better value elsewhere.

It’s disappointing that the IGC is using its report to complain that the FCA is requiring them to provide information that is clearly helping employers and members making comparisons.

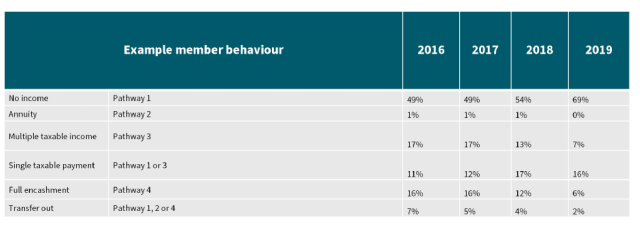

It’s a shame that this part of the report is so weak, for other areas of its investment reporting are strong. I like the attention to the experience of Aviva retirees when reporting on the investment pathways

The IGC’s analysis of the pathways going forwards is authoritative and fascinating

The same can be said of the IGC’s analysis of Aviva’s IGC proposition which is founded on a corporate example

In 2010, Aviva set itself a target to reduce their own

operational carbon emissions by 70% by 2030. They

have already achieved a reduction of 76%

compared to 2010 levels in 2020 and have set a

target of a further 5% reduction in 2021 to achieve

net zero by 2030. Many of the areas they measure

have benefited from significant reductions in travel and

office occupancy during the pandemic, however, Aviva

are setting targets to maintain levels of business travel

to reflect levels reached within 2020.

The IGC has indeed reported on ESG far harder and far longer than any other and they deserve commendation.

Conclusions

I enjoy Colin Richardson’s reports and this is his best in terms of tone and organisation, it gets a green as a read.

The value for money section focuses on what matters most- costs and charges and performance, but it is let down by poor performance reporting and a lack of focus on member outcomes. I give it an amber.

As regards its effectiveness, I give it another amber. Although it has worked hard on behalf of legacy customers and future users of the investment pathways, it seems to accept the situation surrounding the various defaults and some very high transaction charges. Worse, the IGC seems to be using its report to complain against the FCA for requiring better benchmarking, On the basis of the benchmarking in this report, I suspect the FCA cannot require hard enough.

Pingback: The 2021 IGC reports – links, reviews and ratings | AgeWage: Making your money work as hard as you do