NEST insight 2015 suggests a shift in the way employers take decisions about the pension they will offer to their staff. 88% of employers staging with NEST in 2014 relied on payroll software to do so. The majority of employers did not take advice on the choice of pensions and if they made a comparison it was with “the other major mastertrusts”.

The worry is that without the incentive of commission, there is little incentive for advisers to set up workplace pensions. Accountants feel they are being dragged into pensions by dint of their ownership of payroll bureaux but are uncomfortable offering advice on pension choices.

So increasingly, it is payroll personnel who are being left with the task of implementing not just the auto-enrolment process, but the sourcing of workplace pensions.

Our research suggests that payroll, without the skill and knowledge to differentiate the various proposals , will simply signpost products with the least perceived risk – the large mastertrusts.

Payroll are not happy with this as they see themselves on the hook for the outcomes of whatever they signpost.

Increasingly they are looking for alternative ways to help their clients to take pension choices which can be documented and certified by an independent third party.

Insurers should also be concerned by these trends. Without advisers recommending their solutions they are at risk of being cut out of the long tail of decisions from the 1.3m employers still to stage auto-enrolment.

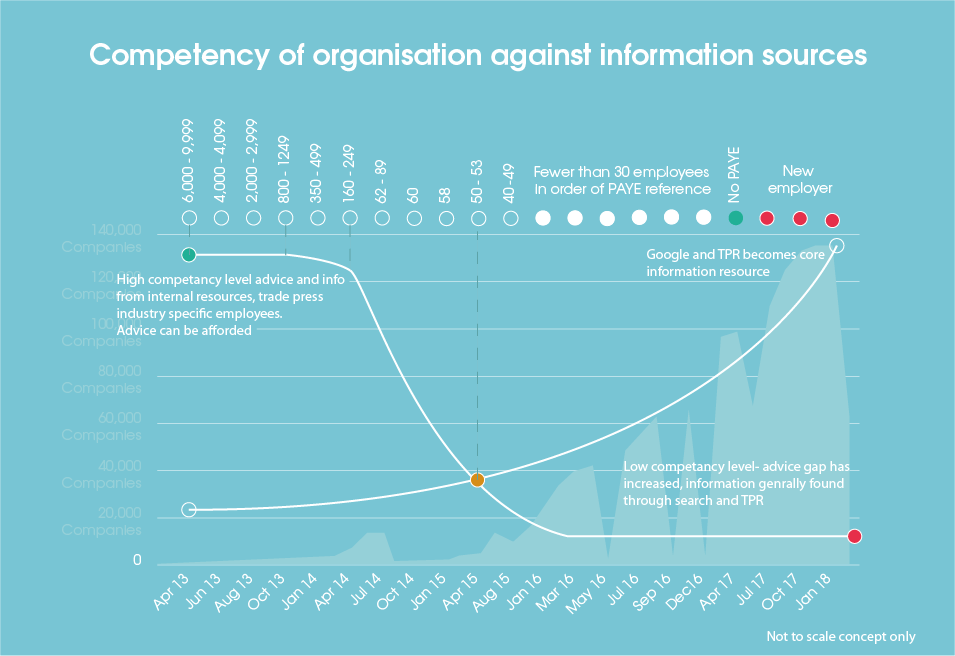

Why digital guidance is necessary.

The cost of making a decision on pensions must be nugatory. We suggest that employers will be unwilling to pay more than £500 in total to get to a fully documented decision.

This simply cannot be achieved by IFAs using conventional methods. A straight through process that analyses employee data, assesses the whole of market and makes clear comparisons is essential. Reports need to be self-generated by employers rather than laboriously produced by third parties.

For insurers , digital guidance , available through payroll is their best hope of pitching their offering against those of the major mastertrusts, NEST, NOW and People’s Pension.

Why is digital guidance not available?

Setting up a digital guidance process is hard and requires a range of skills and considerable knowledge. Without the reward of an asset or contribution based fee, guidance needs to be priced at a point the customer is prepared to pay. To date , no-one has created a mass market digital guidance service.

Why http://www.pensionplaypen.com is cracking that mould

For employers to take properly documented decisions on the workplace pensio they use for auto-enrolment, they need a service that costs la lot less than £500, can be integrated into the payroll auto-enrolment hub and can be used with or without an adviser.

Pension PlayPen is not just a means for employers to find the full range of major workplace pension offerings, it is the way for insurers to find employers.

Indeed, for many insurers it may become their primary means of distribution.

Conflicts with existing distribution?

It the existing advisory model, which has driven most employer decisions in 2012 through to 2014 is to work for the much larger volumes of 2015 and beyond, there will need to be more of it and it will need to be much less expensive.

So far we have seen little appetite among traditional advisers to either drop their price or scale up. Indeed, most traditional advisers are walking away from auto-enrolment at the point when they need it most.

We forecast this trend when we produced the original strategy for http://www.pensionplaypen.com

This chart suggested that the need for self-served information would increase dramatically from the beginning of April, while the capacity of highly competent advisers to deliver advice would fall off a cliff from the middle of 2014.

Far from conflicting with existing distribution, digital guidance (www.pensionplaypen.com), replaces it.

Truly independent guidance

The aim of http://www.pensionplaypen.com is not to promote master trusts over GPPs or vice versa, it is to ensure that employers have proper choice from both and that the decision taken is taken in the full knowledge of what is available.

We think it is really regrettable that insurers are not being considered by most employers but see no way that this will change unless employers can get access to truly independent guidance.

This is not going to happen because of google or the Pension Regulator’s directory or because “something will come up”. The only source of independent guidance available to employers is www,pensionplaypen.com .

Over the next year, we intend for this website will become embedded in the services they are using to stage and manage auto-enrolment.

If 88% of employers are using payroll software to stage and manage auto-enrolment, we intend to be a part of 100% of these software packages.

Next steps

We are not a large organisation. We need to find you, meet you and do business with you , whether you are

- A payroll software provider

- A pension provider

- A Payroll bureau using payroll software

- The accountant owning said payroll bureau

- The adviser keen to help with the use of our offering.

You can help us to meet the needs of the 1.3m employers to state (and the 250,000 employers born each year). You can use our service, you can promote your pension on our service and you can even advertise on our website (which helps everyone.

If you are reading this and feel your organisation should be integrating with us in one of these ways, please call Henry on 07785 377768 or email him on henry.tapper@pensionplaypen.com .