Yesterday the FCA published the latest edition of its Retirement Income Review

Latest data from @TheFCA Retirement income market interactive analysis 2023/24 https://t.co/LKoNDr4JT7

— Tom McPhail (@PensionsMonkey) September 26, 2024

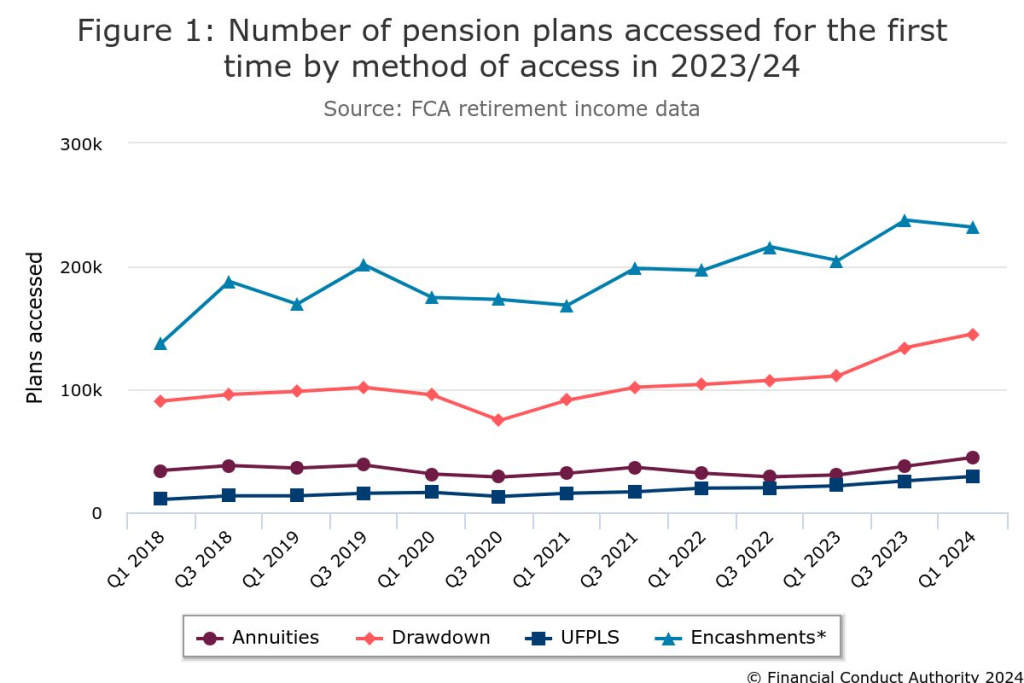

We learn that the number of pension plans accessed for the first time surged in the past year, as economic pressure continues to mount, FCA data has revealed.

The regulator’s latest retirement income market statistics, published today (26 September) showed the total number of pension plans accessed for the first time increased by 19.7% to 885,455 in 2023/24 from 739,652 the previous year.

Around 30% of pension plans accessed for the first time in the past year were accessed by plan holders who took regulated advice.

This was down from 32.9 % the previous year.

Quilter head of retirement policy Jon Greer said this ongoing drop suggests that more people are navigating the complexities of pension withdrawals without professional help.

This, he said, raises concerns about the long-term sustainability of their retirement strategies.

Sales of annuities saw the biggest jump, from 59,163 in 2022/23 to 82,061 in 2023/24 (38.7%).

Sales of drawdown increased by 27.9%, from 218,183 in 2022/23 to 278,977 in 2023/24.

The overall value of money being withdrawn from pension pots rose to £52.1m in 2023/24, from £43.2m in 2022/23 – an increase of 20.6%.

Greer said the substantial increase indicates that more individuals are turning to their pensions to manage their financial needs.

This, he suggested, is likely influenced by the cost-of-living crisis “forcing people to dip into their pension pots” to supplement other forms of income.

The regulator and the government have made it clear that they intend to improve the UK pensions system.

The FCA published its thematic review of retirement income in March 2024.

It suggested that while there are no systemic issues in retirement income advice practices, there are pockets where they could be improved.

This includes approaches to determining income withdrawal and gathering information to demonstrate advice suitability.

The new Labour government yesterday (25 September) closed its call for evidence on the first phase of its landmark pensions investment review.

The review will aim to boost investment, increase pension pots and tackle waste in the pension system.

Greer said:

“This review is expected to prioritise clearer guidance and support, helping individuals make informed decisions and avoid detrimental financial mistakes.”

The simplest way to help people access their money without detrimental retirement mistakes is to let them draw a pension. IFAs commenting on the news seem to agree

What a mess

what a mess

I agree, it really is time to put in place some member protection, or the saving of a generation will be go wasted.

People want pensions and they don’t want to or can’t find advice on how to do their own. The Government’s plan for a default decumulation option for workplace pensions cannot come a moment too soon.

In addition to cost of living pressures, illness prompting early retirement etc, I suspect another driver of the big increase in access is the fear of Labour winning in the run up to July, and the fear that “Labour are going to steal my pension!” or eliminate TFC, or reintroduce LTA or… (insert scare story from paper of choice here).

Another factor in withdrawals is mortgage interest rates. It used to be the case that a pension pot would grow faster than the interest rate paid on a mortgage. That has changed and now it can look better to take pension money to pay off a mortgage early rather than later.

I’ve moved part of my pension into drawdown. I didn’t take advice and I’m happy that I know what I’m doing. I’d be really annoyed if I was forced to take (and pay for!!) “regulated advice” to tell me what I already want to do. Just sounds like the people in the industry trying to force changes to ensure they get their cut when people no longer feel the need to voluntarily pay for that advice.

As far as “putting pots into drawdown” – this doesn’t mean that the total value has been withdrawn, quite the opposite. The lump sum may have been taken but the rest could be taken as a recurring income at a sustainable rate. The interesting information would be what effective withdrawal rates people are taking from their pots. This should take into account that people may decide to take a higher percentage earlier in retirement before their state pension cuts in. This is also something that annuities (and similar products) should take into account. My drawdown projection assumes I’ll require less income from age 80 onwards. In my case I assume a 25% reduction. My projections also take into account state pension at 67. I don’t believe pension products allow any staggered front loading options?

Some DB schemes allow flexible benefits from

earlier ages.

eg you may be able to choose whether to have a lower starting pension that increases when you reach your State Pension Age, or a higher starting pension that reduces when you reach your State Pension Age.

Another example (from the NHS Scotland scheme)

If you retire before you reach State Pension age, your pension will be reduced for early payment.

However, if you plan to retire after your 65th birthday but before your State Pension age, you can elect to pay extra contributions that reduce, or remove, this reduction.

https://pensions.gov.scot/nhs/growing-your-pension/taking-your-pension-early-no-reduction

Of course one number never tells the whole story.

What I found interesting was the age distribution of those entering drawdown, 75% were between 55 and 64 and 22% were between 65 and 74. A finer breakdown could be particularly revealing – just how many people are close to 65 and actually retiring. (And how many over 65 are already in retirement and for whom this is just one of a number of pensions?)

Or a bit of all the above. And don’t forget those of us who’ve experienced missold pensions, juicy-for-some trailing commission with-profits investments from back-in-the-day chancers exploiting the unintended impression that financial advisers were

bad and independent financial advisers were therefore good – remember all those FSA adverts? I’ve been trying to make sense of these mysteries since before Mark Dampier was the new boy at HL, never mind Tom McPhail. The irony now is that, all other things being equal, I’m so superannuated I can’t benefit from the Holy Grail of Pension Superhaven, even if I want to! Oh well, can’t win them all.