Ian Pittaway , chair of Aegon’s IGC (and master trust) is independently minded. He is not going to be told what value for money is by Government and his introduction to the 2023 IGC report makes this clear

Ian Pittaway , chair of Aegon’s IGC (and master trust) is independently minded. He is not going to be told what value for money is by Government and his introduction to the 2023 IGC report makes this clear

The IGC has developed its own value for money principles to reflect Aegon UK’s book of business. These value for money principles reflect research amongst Aegon UK’s customers and also amongst broader consumers which asked what they regarded as key to value for money.

This sounds like a 14th century feudal lord telling the King he’s going to manage his fiefdom the way he and his vassals want it governed. That’s fine , so long as everyone is thinking the same way, but in pensions – everyone has their own view

The findings showed that as well as looking for low charges and good returns on their investments, customers want a choice of funds, which are responsive to the appetite for investment risk they have and that they want to be able to keep track of their policy’s performance online

This is exactly right. People who own a personal pension policy – whether through the workplace or directly, ought to be able to know the return they have on their money , choose funds that suit them and have the information delivered to them on-line.

I’ve been working all year with Aegon delivering personalised performance numbers for a group of 12,000 members of an Aegon TargetPlan offered by a large employer. Despite the underperformance of the BlackRock Flex Lifepath Default on offer, employees have been downloading an app, seeing their personal performance and comparing it to the performance others have been getting in different workplace pensions.

I had expected to see details of this arrangement in the report but sadly, the report has nothing to say about keeping “track of their policy’s performance online”. It doesn’t mention that this is actually happening and it contains precious little information for policyholders looking to see how they are doing compared with other savers.

So I’m looking forward to a call from Ian, who is a gent and works round the corner to me. I’d be delighted to show him how Aegon has worked with its client to get this information in its policyholder’s palms!

Value for Money with Aegon

Aegon- despite Ian’s protests – will be assessed on the same basis as everyone else, the member experiences and outcomes of saving will be what gives their GPPs a red, orange or green rating and it won’t be the IGC who determines what goes into those ratings.

Member experience

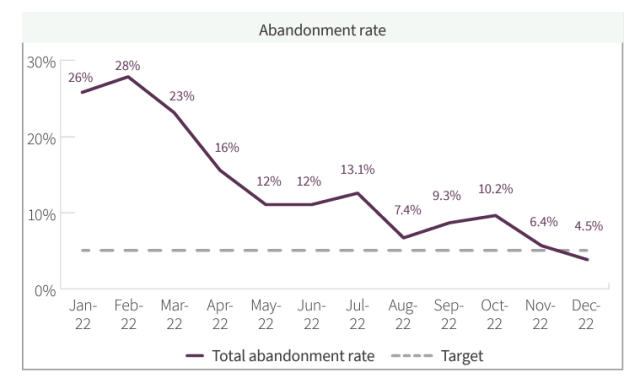

Judging by this report, Aegon will be struggling to demonstrate VFM based on recent member experience. At one point last year over one telephone call in four was being abandoned

Service levels were not being met

and customer satisfaction ratings were terrible

Although we’re told 2023 is better, this is about 2022. and this last chart tells us that customers are not happy with their experience of Aegon.

The IGC does not duck publishing these charts and it rightly calls out the member experience as not being value for money. This is the right call – I wish that more IGCs would do the same.

Like their neighbours Scottish Widows, Aegon are investing heavily in digital engagement tools (good) , but this should not be at the expense of traditional customer service. People are scared of pensions and need a human voice at the end of the phone and a proper job of guidance.

Member outcomes

What goes into a good outcome is contributions, good investment returns and the right investment pathway at retirement. Good returns are assisted by low charges but low charges don’t necessarily mean good outcomes.

It’s disappointing that IGC reports still devote the bulk of their pages to charges rather than properly investigating investment performance. One of the default investment products – the BlackRock Flexi Lifepath fund has had a bad couple of years (after some very good ones). I had to look into this on behalf of a client and discovered the problem was down to the asset allocation (no cash) and the hedging strategy (no pick up from a weak pound). Invested money in long-date gilts (as stated by the IGC) may have contributed but I’m surprised that a fuller explanation isn’t given.

What is clear is that the investment pathways must have been stuffed with long-dated gilts to have achieved these disastrous returns. Imagine transferring into a product for “growth” that lost 17.2% in 2022

Imagine investing into a product to help you buy an annuity that lost 40% in a year

Ironically, the Target Plan solution invested in bonds – presumably the other solutions invested purely in long dated gilts. The problem stated for the Target Plan’s retirement solution was that it was overweight in gilts. Investors need a better explanation than this and they need , (as the Chair has said) products more suitable to their needs.

While I am comfortable with the way the report records VFM on service, I cannot understand why it gives a green for investment performance

So I suspect will these customers

BlackRock’s Flexi Lifepath default sits at the bottom of the CA league table of workplace pension defaults (NOW excluded). It is hard to understand the difference in performance between it and it’s ARC counterpart. Aegon savers really need more from the IGC on these matters.

In all honesty, I am baffled by the VFM assessment, I give it an amber

Is the IGC effective?

With some IGC reports, I feel that the the IGC is simply reacting to information it is given. With others I feel the IGC is helping to improve experience and outcomes.

With Aegon, where outcomes and experience are so divided between different products, I sense that the IGC is as baffled by what is going on as I am. I don’t think the IGC is doing harm, but I don’t sense it is doing much good and I think it needs to find a way to understand just what lies behind the wild results it reports.

I give the report an amber for its effectiveness, but this could easily turn to red.

Style and tone

Clearly the IGC knows its stuff and its experienced chair sounds authoritative at all times. But too often I am confused between what I’m being told and what I’m reading.

I am not quite sure what I should give it – so will give it an amber