Royal London’s IGC report has the best opening of any report I have read.

The primary purpose of the Independent Governance Committee (IGC) is to act independently to assess the ongoing value for money provided to Royal London’s Workplace Pension and Investment Pathway customers. This is done by reviewing;

-

Plan charges;

-

Transaction costs;

-

Investment strategy and performance; and

-

Customer service and communications.

Not only is this bang on message with the VFM assessment project but it makes sense of what VFM is trying to do. “Review” is the word- Royal London’s IGC has been doing this for years and their reports have morphed from early stage marketing documents to the more austere reports produced by their IGC chair – Peter Dorward.

Royal London’s report is important. They are the sole insurer offering AE workplace pensions purely as GPPs. Not having a master trust means this is all we get from Royal London – there is no master trust chair report.

The best word to describe the Royal London IGC is “conservative”. The report sets out to characterise Royal London as an organisation that knows its limits. It does not have its own advisers (uniquely to its peers) and is therefore reliant on savers making their own “pension” decisions (through investment pathways) or on IFAs helping their policyholder’s out.

The concession that Royal London has made is in the area of “digital guidance”

As Royal London does not offer financial advice to customers, we are closely monitoring the development of Royal London’s digital capabilities and financial wellbeing service, which aims to provide support and guidance to customers who do not have their own financial adviser. Wealth Wizards, acquired by Royal London in 2021, is expected to support Royal London to further enhance its financial wellbeing service for Workplace Pension customers.

One would have thought, in the fast moving world of Fintech, that the expectation would be that Wealth Wizards would already be “on stream”. But these things take rather longer at insurers – longer that many customers have got. With so many advisers walking away from the workplace pensions set up when workplace pensions made them money, support for Royal London policyholders remains a difficult area – especially with the Consumer Duty upon us.

Value for money

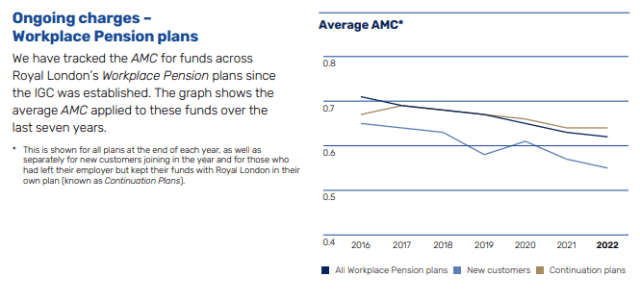

Although workplace pension providers pretend VFM is about membe outcomes, their focus is actually on competitivity and – in the space that Royal London play, the primary way in which VFM is currently measured is through the AMC offered to individual employers.

The graph above, produced by Redington (who do comparison services for IGCs), is that Royal London’s existing customers are charging above the average for workplace pensions. Were there a line to show the price offered to new employers (customers), then the 2022 price of around 55 bps would be well above the average. Royal London are not competing on price, it would be interesting to know how much new business they are securing.

My concern for Royal London customers is not that they aren’t getting competitive pricing but that the product offered is not being nurtured by a new business stream and might ultimately be considered a “legacy” business by an insurer with other products to focus on.

This touches on a more general observation about Royal London strategy. With all their peers actively competing using master trusts as the headline product, is there a space for the more expensive and less collective GPP and Stakeholder products, used by Royal London customers?

Future value for policyholder’s money depends on the sustainability of Royal London’s support for its workplace pension business.

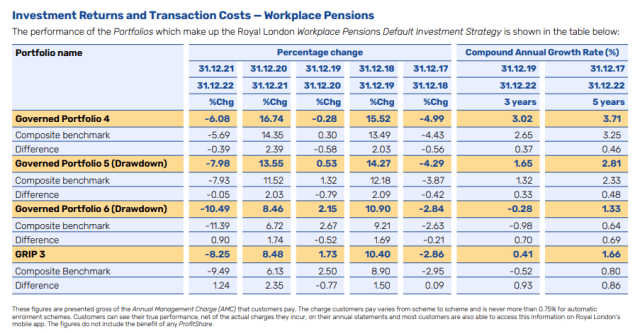

The investment section of Royal London’s report is excellent. It is easily accessible via a tab on the PDF and contains a detailed assessment of the Governed Portfolios offered by Royal London. Despite the high degree of governance on offer , these portfolios have not fared well for savers over 2022 (the reporting period).

Bravely, the IGC focuses on how the 2022 returns compared with illustrative returns (the closest things members are given as an expectation.This table shows that while those who can take risk, took a big hit, so did those who couldn’t. The people who took the biggest hit (a loss of 17%) were the people who had no time to recover.

If you give someone an expectation that they should get an inflation adjusted return of (0.8%) when their money is at highest risk, then giving them a loss (after inflation of 17%) is hardly value for their money. But the IGC states of these numbers

We are comfortable that due care has been given

to setting up Portfolios to manage performance and resilience of the delivery of that performance going forward. Nevertheless, we consider the inflation-adjusted rates of return achieved since launch to be strong, which contributes positively to the Value for Money received by customers.

Policyholders may take a different view.

I am also impressed that Royal London use the CAPA tables which show that the fund that delivered such low returns did better than its peers (hence the sanguine comments above)

The IGC further congratulates Royal London for better longer term returns

We are comfortable that due care has been given

to setting up Portfolios to manage performance and resilience of the delivery of that performance going forward. Nevertheless, we consider the inflation-adjusted rates of return achieved since launch to be strong, which contributes positively to the Value for Money received by customers.

I don’t know how bad things have to get for a conservative IGC to get radical but it strikes me that the non-advised workplace savers who have been given illustrations showing growth on their money, are in need of something rather better than what they got. Simply not being as bad as your competitors does not make your value for money “good”.

This is the downside of the Royal London “conservative” approach to reporting VFM. It relies on industry norms, not on member expectations. Consequently the report succeeds as an industry report and fails its consumers. For all its excellence, the IGC is not really challenging Royal London to explain how its risk protection failed its older savers so drastically in 2022. I give the report an amber as a VFM report.

As a piece of work – this is a great IGC report which is easy to read and navigate, it is really informative and – from a professional standpoint, I doubt I will read a better, in terms of content and style I give the report a green

As a demonstration that the IGC is effective , I see plenty of challenges to its provider. The IGC really does look independent and it knows what it is doing. It is a conservative approach to challenge, there is no strategic challenge on the big issues that personal pensions find hard – CDC, longevity insurance and most of all – the support that personal pensions need from advisers and those providing guidance. But I think it unfair of me to mark the report down on this, this is a matter for Royal London’s executive not its IGC. So I give the report a green for the IGCs effectiveness in driving value for saver’s money.

Pingback: How IGCs have performed this year and since 2015 | AgeWage: Making your money work as hard as you do