Conventional and Index Linked Price Performance

Iain Clacher & Con Keating

Jon Spain

Acknowledgement: We owe thanks to Jon Spain for data and insights into Retail Price Inflation (RPI). We also note that he raised concerns over Liability Driven Investment (LDI) as leading to crisis with the actuarial profession as early as 2009.

Introduction

This note considers the divergence of the price behaviour of Index Linked Gilts (ILGs) from that expected from the movements of matched duration conventional gilt prices, and some of the ramifications of that. As LDI and leveraged LDI are concerned with hedging by matching the durations of assets and liabilities, this difference carries concerns for the quality of the hedge with it, and the potential for losses to arise.

Data

We illustrate these issues using the interest accrual adjusted daily dirty prices of two index linked gilts and their conventional spot gilt yield equivalent prices. As the subject is highly technical in nature, we have attempted to illustrate this in simple terms.

The choice of dataset used is not arbitrary; it runs from June 2017 to the start of November 2022, as we believe this to be sufficiently long to illustrate both normal and stressed market conditions. The average daily returns of these datasets are less than one basis point; in this regard it may be considered a full cycle, but we would caution that averages can hide many a sin. However, we do believe that this more simplified analysis still allows for meaningful insights to be generated. Figure 1 below shows the scatter plot of returns for the 1/8th % ILG due 2036 and its conventional equivalent.

Figure 1: 1/8th % ILG 2036 and Conventional Gilt Returns – June 2017 to 31st October 2022

Figure 1 also shows an ordinary least squares regression of the ILG on the conventional. If the ILG behaved as its mathematical fixed income properties would imply, the slope of this regression line would be unity and the intercept would be zero. The reported intercept value is not statistically different from zero.

Results

The first point to note is that the relationship between the ILG returns and the conventional is weak; just 63%. This means that any hedge would be weak with much room for error based on the noise in this relationship. The second, and more important result, is that the returns arising from changes in the gilt yield are explained by an allocation of just 0.7 ILGs rather than 1 ILGs. The IILG is far more volatile than was expected, 1.41 times.

If we were to have hedged all interest rate and inflation risk using this linker based on its theoretical duration, we will have profited unintendedly as rates fell and returns were positive and lost when rates were rising as experienced recently.

Over the period of the dataset, RPI averaged 5.00%, starting at 3.7% p.a. falling to 0.9% in 2020, and then rising to 14.2% in the most recent month. Prices, as measured by RPI, have increased by 30.8% over the period. By contrast the price of the ILG has fallen by 5.6%, and the conventional gilt price is unchanged (-0.0001%).

In summary, the ILG over-hedges interest rate variability within this period and also fails abjectly to hedge inflation over this term.

Figure 2: 1/8th % ILG due 2068 and Conventional Gilt Returns – June 2017 to 31st October 2022

From Figure 2, we can see that the results for a much longer dated ILG, the 1/8th 2068, are broadly similar to those obtained for shorter dated ILGs, though here we would draw attention to the differing scales between the shorter-dated and longer-dated gilts.

Over this period, the conventional gilt has fallen by 3.7%, and the ILG has collapsed to just 52% of its initial price. The decline is even more pronounced using clean prices, it is at 40% of its initial value.

The 2068 1/8th ILG had a duration of 50 years at the start of the dataset, so if our liabilities had a duration of twenty years at that time, the loss arising would have been just 16%. The earlier 2036 1/8th ILG had a duration of 19.3 years at start of the dataset, so its loss, at 5.8%, would have been only slightly higher than the earlier reported 5.6%.

At the inception of this dataset in June 2017, the spreads to RPI were minus 154 basis points for the 2036 1/8th ILG, and RPI minus 149 basis points for the 2068 1/8th ILG, and they are now minus 9 basis points, and plus 12 basis points. A bubble well and truly punctured.

Further Points

We are not the first to raise concerns about the use of index-linked gilts. See for example: The Government Actuaries Department’s analysis for the Ministry of Justice of the Personal Injury Discount Rate.[1] That contains, inter alia, the caution:

“We would note that in practice, the ‘risk free’ portfolio is likely to be only a theoretical construct and even a portfolio invested in 100% ILGs would not lead to ‘risk free’ claimant outcomes.”

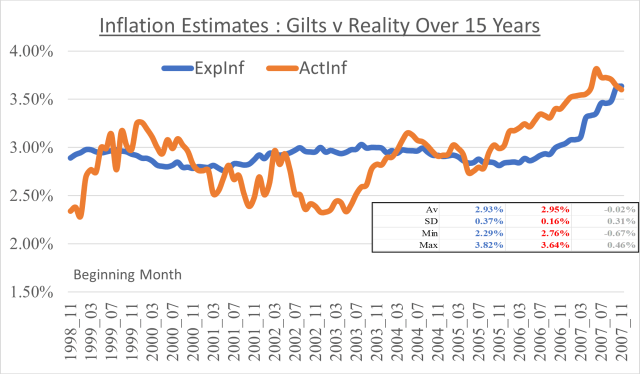

Figure 3: Expected and Experienced Inflation

We would also note that ILGs are only weak predictors of future inflation, as figure 3 above illustrates. This shows the actual inflation experienced over the subsequent 15 years along with that implicit in the gilt markets. As can be seen there is a pronounced cyclicality to the errors.

Conclusion

Index linked gilts assure their owner of achieving RPI if bought at a clean price of par (100%) and the gilt is held to maturity. Their small coupons are of little value in matching the required pension payment cash flows. Their intermediate performance, by contrast, may bear no resemblance to inflation adjustment, as in the illustrations above.

Their volatility characteristics make them of little value as substitutes for conventional gilts; they are more volatile, which will lead to gains or losses depending on the direction of interest rates, and therefore produce highly inefficient hedging.

As leveraged LDI involves the possibility of sales being required to meet collateral calls, and these being likely to occur in times of increasing interest rates and falling asset prices, it seems only too likely that using ILGs in that setting will result in significant losses. In addition, as they do not reproduce the return characteristics of conventional gilts, they are unlikely to be an acceptable surrogate for them.

We believe that the poor trading characteristics (a thinly traded market), excessive variability of price, and the ‘bubble-like’ behaviour of earlier years, in which the expected returns of ILGs fell significantly e.g., the 10-year ILG fell to RPI minus 3.20%, are all symptoms of the excessive concentration of ownership of ILGs in pension funds, which is over 80% of the outstanding stock.

[1] https://consult.justice.gov.uk/digital-communications/personal-injury-discount-rate/results/gad-

analysis.pdf