Last week, the Pensions Regulator issued a press release which contained the following statement

The Pensions Regulator has now written to me – through Nicola Parish with the following statement.

We read with interest your blog dated August 7, entitled, Square pegs – round holes; retirement advice needs a rethink, in which you discuss the investment pathways open to pension savers. We note your assertion that TPR is suggesting those who help savers access pension pots to pay household bills may be scammers, and that savers should not use their pots to pay bills.

I would like to make it clear that that is absolutely not what we are suggesting.

Our Scams Strategy seeks to help savers spot the signs of a scam, encourage schemes to adopt higher standards of protection for savers’ pots and secure the intelligence we need to work with others to pursue and punish criminals. Last week we issued a timely warning that people who are struggling to pay household bills may be more vulnerable to scams and need to take great care.

Of course, we agree that people can draw down (or ‘cash out’) their pension after 55, as long as they pay the correct tax rate, but it is incumbent on us to point out the risks of doing so in relation to scams. We recommend savers seek regulated advice and of course must do so if a cash equivalent transfer value is over £30k, and the member is seeking to transfer. We also encourage savers to use the MoneyHelper service if they are concerned about the cost of living crisis.

We are not saying that trustees or regulated advisers who offer savers guidance based on what is legal and sensible are in some way part of a scam. We are though keen to educate people on how to spot a scam to avoid them falling victim to the scammers.

The Pensions Regulator has asked me – if I revisit this subject – to clarify their position. I have to say my thoughts are seldom far from the plight of those looking at the common month with deep concern. I’m concerned for the many people I know through my family, church and through my social life who are between fifty and seventy, struggling with their finances and ignorant about pensions.

Their number one question to me right now is “can I use my pension to pay my bills” and my factual answer is “yes – and this is how“. Some of that money will be spent in the Cockpit public house to be sure, but most won’t.

These people will talk to people they trust , but they will not talk to anyone who might be a snooper, and that includes most people in Government ( a major obstacle for MoneyHelper). They are right to be cautious.

In reality most people in authority do not see the drawing down of pension pots prior to state pension age as a good thing.

The official line from the DWP is that though it is legal for people to draw down or cash out their pension , people who are found doing so may be disallowed the benefit on grounds of “deprivation of capital”.

A former TPR Director has written on Linked in that money in occupational schemes should not be transferred to contract based schemes but stay under the control of trustees, to prevent members from financial self-harm

And Baroness Altmann has written on this blog that

the vast majority should not be looking to touch their pensions if they have other ways of supporting themselves through this crisis.

The Pensions Regulator is right, in my view, to point this out and I would be really nervous about any public programme or pressure that urges people to spend their pensions, rather than keep them if they possibly can.

So people who have pensions are facing the opposition of the Department that pays benefits, a former older people’s Czar , the Pensions Regulator and all those influenced by these powerful voices.

I call that a pretty strong nudge. But a nudge to what?

We are facing a genuine financial crisis, one that pensions can play a part in mitigating, by ensuring that people are confident enough to access their pots in a sensible way to pay household bills as they arise. Those bills are arising now and its those in their late fifties and sixties who are most in need of supplementary cash to pay them.

Research from the Institute of Fiscal Studies using ONS data suggests that the highest levels of absolute poverty are in the years leading up to the taking of the state pension. The dark green line represents a cohort of savers who are failing to bridge the gap from the end of work to the beginning of the state pension.

The reality is that people – when they get to State Pension Age are much better supported by benefits than before

Where I think there is a mental disconnect between TPR and the harsh reality of the moment is in considering all “pensions” the same.

For the 10m who have only saved through workplace pensions , what TPR and the DWP, and Ros call “a pension” is no more than a small reservoir of capital to be spent at some point after 55.

TPR need to accept that financial advisers are not providing a service for those struggling to make ends meet, simply harking on about the need to take financial advice is the wrong message for those with a small pot , in need of spending.

And ordinary people should not need to pay for financial advice when cashing out their pension. The advice is a cost they cannot afford, even if it was available. They need to use the resources proportionate to their need – MoneyHelper being one, MoneySavingExpert being another. There are a range of charitable websites devoted to debt management and the management of tax and benefits , all of which are available from any connected device.

A new mindset needed from TPR

TPR needs to accept that many of the first generation of AE savers may do no more with their retirement saving, than bridge to their state pension age, using the little capital they have to avoid absolute poverty. While any money is capable of being scammed, there is no reason why money being drawn out of workplace and non-workplace DC pensions is any more vulnerable. Indeed the pension has a purpose, which is socially important – it is alleviating immediate acute poverty. People who are struggling to pay household bills are unlikely to reinvest the proceeds of their drawdown into scams, they want household bills to be paid.

TPR’s view is an anachronism, it needs to change. The 10m people who have started saving since 2010 need help managing the drawdown of this money and according to statistics supplied me by Emma Douglas of Aviva and the PLSA, cash-outs are up a third this year, partial encasements nearly 40%. Rather than worrying about these people being scammed, we should be focussing our attention on making sure their immediate financial needs are met – firstly by making the money readily available and secondly by ensuring those cashing out their savings are aware of issues to do with tax (the taxman is not a scammer but can act like one).

It is absolutely in the prerogative of the saver how that money is spent. The deprivation of capital rules are a historical anomaly dating back to Gordon Brown’s introduction of pension credit (and made a nonsense of by pension freedoms). Ros’ description of pensions as “precious” owes much to her days fighting for the rights of members of schemes such as ASW. Andrew Warwick-Thomas’ championship of the right of trustees to determine when members get money is a very 20th Century notion (a kind of benevolent paternalism).

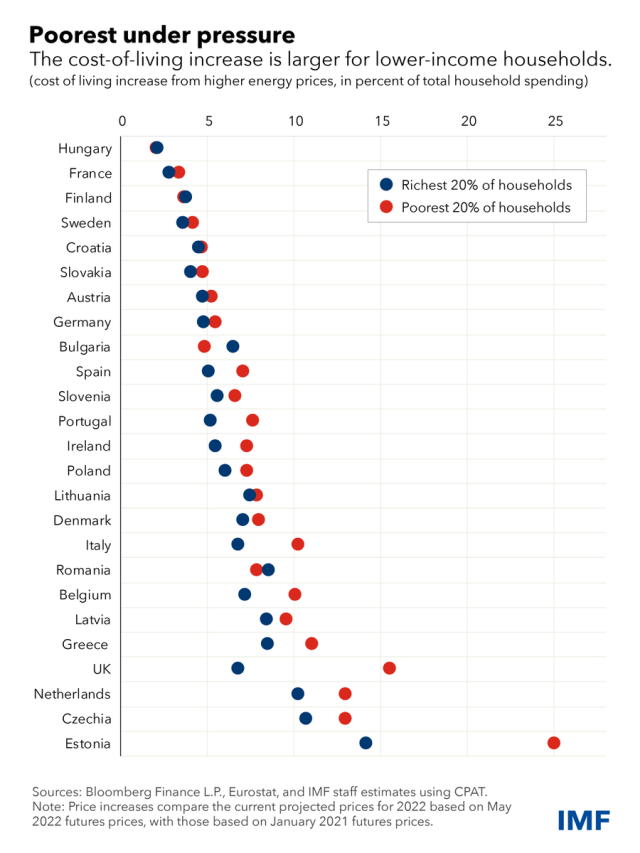

A sea-change in attitude is needed right now in Brighton, Caxton Street and among those who have charge of our workplace pensions. That sea-change can start by people in power understanding this chart.

The red dots in the UK are very often between 55 and 67. We cannot have the blue dots not recognising the plight of the red dots.

Retirement savers are facing a second crisis, following the Covid Crisis of 2020. Instead of lockdown, they face financial meltdown, not of their Banks but of their personal finances.

Financial scams are an issue, but scammers will follow the money – focussing on the six and seven figure pots from CETVs not the small beer from AE savings.

Money drawn down from a pension pot to a bank account needs to be executed with due care. The identity of the pension account, the person instructing the transfer and the owner of the receiving bank account must be verified as the same person. But this is no different from any other financial transaction and should not give cause for concern.

The campaigns to make people aware of the threat of scams are important (I am promoting some in a parallel blog) but they cannot become a means to prevent people from drawing money so badly needed.

It is not for pensions people to fret at the onward destination of the money once drawn, that is beyond the powers of the Pension Regulator and where money is subsequently stolen, it becomes a matter for the police.

What I am calling for is different, a positive approach from the pensions industry to calls on capital from people in need of cash to pay household bills. Instead of worrying about scams, TPR and others should be promoting the value of saving over the past ten years, which can now be put to proper use, paying household bills.