I’m flipping furious with the Pension Regulator’s insinuation that those helping the hard up to access their pension savings to pay “household bills” are scammers. Here is an extract from someone who provides guidance to the over 55s for a living. He sounds as upset as I am.

I wonder if people like Ros Altman have much if any contact with the poorer members of the public. In my work … I see a wonderful cross-section of society. There are all too many who aren’t working and may not have worked for some years because of their own health conditions or because they are caring for others. Some of their health conditions come from working in the many physical jobs we need in society. I suspect Ros has never done any of these jobs.

Others, through health, lack of education or abilities, are not able to get jobs on much more than minimum wage.

There is a substantial problem with people getting into debt. You might like to talk to Citizens Advice if you want some figures and descriptions of some circumstances, including errors by government departments.

The suggestion that people should max out their credit cards is particularly dangerous for them. Some people don’t have credit cards at all and poorer people are only likely to get ones with APRs of around 30% or more.

Their use may be acceptable for a problem that is guaranteed to be short-term, but it just a route to further debt in other circumstances. I get a few people who want to take pension money to pay off / pay down credit cards. This looks like a wise financial move. The APR on the credit cards will almost certainly be much higher than the likely growth rate of the funds in their pension pot.

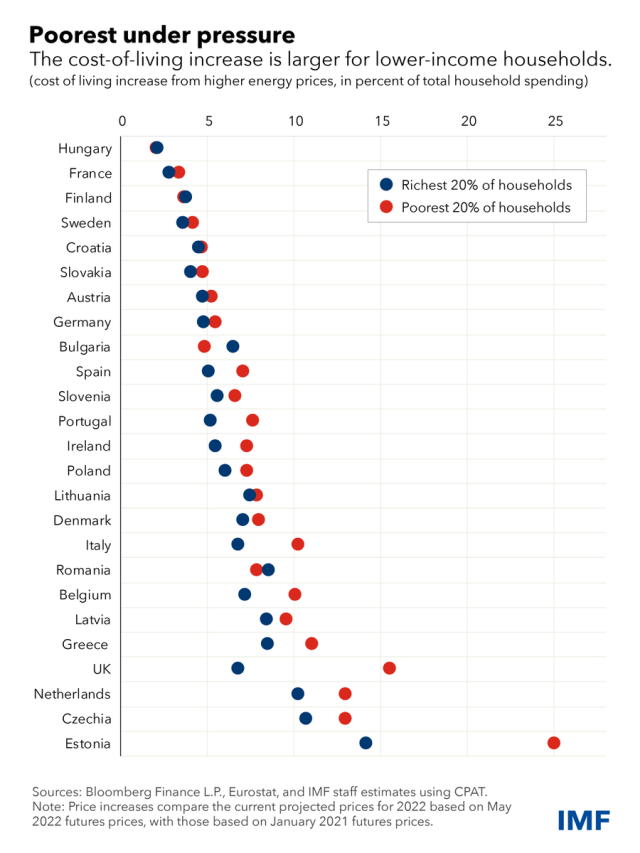

Anyone who has been following Martin Lewis will know how much a threat the rise in the energy cap is going to be to poorer households. I repeat this IMF graph for the third time.

The Government have not intervened sufficiently to help , but now it seems determined to hinder, by driving people into debt and default rather than spend what they have saved.

And it should not be for the DWP to supress me from arguing against the early encashment of small pots by those heading for a pension credit claim. Andy Young, who was once GAD’s actuary for the DWP (as well as advising Ros Altmann and Steve Webb) has chosen to go public on this.

Needy people need to manage their entitlements to means tested benefits for the same reasons that the better off manage their tax – it is worth doing. And for needy people, essential. It should be a lot easier and clearer for them to manage.

— andrew young (@glesgabrighton) August 6, 2022

There are four investment pathways; let’s remind ourselves of them

Pathway one; for those so rich they can leave their pension pot as a bequest – wealth management

Pathway two; for those who want a pension and are risk averse – annuity purchase

Pathway three; for those who want flexible access to their pot – drawdown

Pathway four; for those who want (or need ) their money now – cash out.

IF pathway four is to be degraded to “scammers way” then I am out. I am off and away from the Pensions Regulator, from the Lords and Ladies and from all those who consider pensions too “precious” to be spent on household bills.

Means testing is an insult to a citizens pride and integrity. It means that the government don’t trust us so why would we trust THEM! Also, ‘a pension saving’ is a for when we are old and not able to work – it is not a ‘windfall bounty’ to be played with by professionals, opportunists, government or profit seeking employers. When a commercial company arranges ‘a contract’ with employees offering a company pension – that should be honoured by them and government backing so that it may NOT be closed down in adverse events certainly not on sale of such to third parties!

Having managed a provident fund (a pension fund which may be drawn upon for specific purposes, including need) for over forty years, I can confirm this arrangement works well – and it leaves little room for the scammers or usurers to get their foot in the door or maybe that should be their hand in our pockets. The issue with such funds is that they may leak tax concessions.

With you Henry. There are cash-out scammers for sure, they need to be detected, and there must be redress for the cases that slip through. But to discourage people from accessing safely the cash they need now … is culpably out of touch. It’s let them eat cake. The answer to abuse is not disuse, it’s right use.

Peter. There should be a means for those of us vulnerable financially to access cash in times of a national emergency’ They should not have to ‘sell their basic assets’ to exist in our complex society. I agree there are too many ‘scammers around’ but that’s a failure of government order! All you are doing is encouraging them.

Hi Peter B – After reading both your comments, let’s agree to disagree.

I think you’re saying that people with accessible DC pension savings and an urgent need for cash, should get the cash from the government without needing to draw on their pension pot. I can understand the argument, but I don’t agree with it.

A DC arrangement isn’t a contract to provide a pension; it’s a tax privileged savings account.

Re my first comment: I could have been more explicit, scammers need to be detected *before* they do people harm. But I don’t think my words can reasonably be described as encouraging scammers.

Peter. No where in Henry’s comment is there a mention of a ‘DC savings scheme’. Is that what you identify as a ‘small pot’ (whatever that may mean)? Also, its clear that Henry says that the government should have or won’t act leaving us to ‘fend for ourselves’ in an ill paid ’employment/pension’ environment. To my mind DC is not a true old age retirement offer. I was in a company DB scheme that changed the rules by offering conversion to DC (a lesser benefiting scheme) not suited to ‘old age’ ie a scam by employers and backers thereby degrading future pensioners. Not only that, last century government asset stripped pension funds with the dreaded ‘windfall tax’ – a direct arrow to the heart of pension funds. Needless to say many of these ended up in either the FAS or the PPF!

Pingback: TPR clarifies it’s not wrong to use your pension pot to pay household bills. | AgeWage: Making your money work as hard as you do