Below is today’s email I got from the FT’s unhedged service. Normally it’s written by gnarled veteran Robert Armstrong, but he is sick, so Batman gives way to Robin in the form of Ethan Wu, who I find wonderfully entertaining . You can sign up here to receive Unhedged in your inbox every weekday.

At one point on Friday, the S&P 500 was down 20 per cent from its peak around the turn of the year. That would have put us in a bear market by the standard definition. But even now that the market has risen by a few ticks, and even if we get a bounce in the next few days, we are undoubtedly in a bear market. Bears have two key characteristics:

Currently we are checking both boxes pretty comprehensively. Few, if any, markets have provided a haven. Even markets that have performed reasonably well in local currency terms, such as the UK’s, have been undercut by the strengthening dollar:

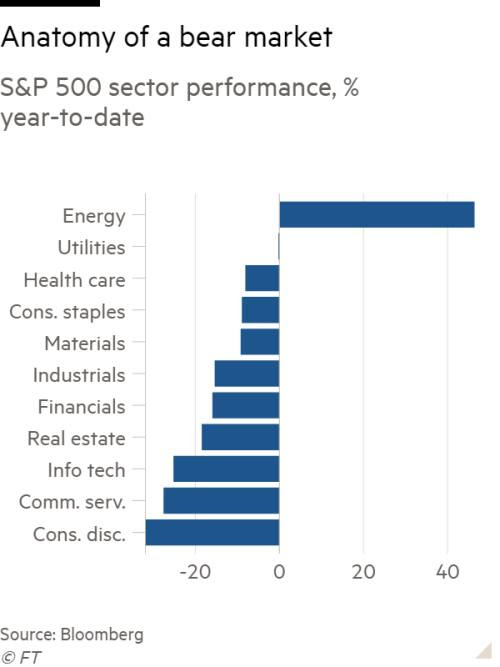

Other than energy and commodities, there have been few haven sectors:

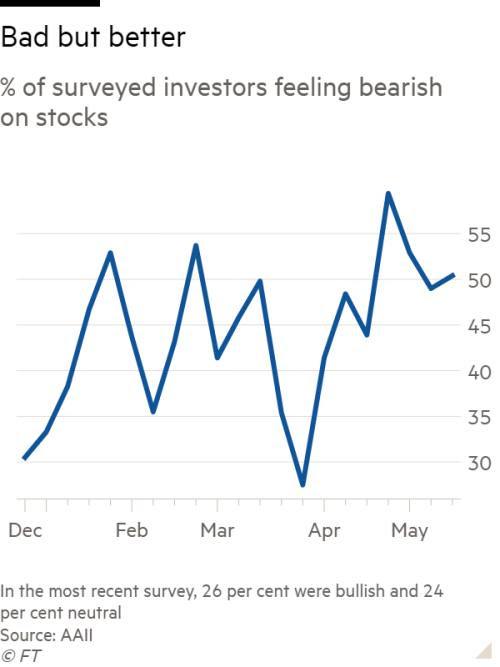

This has driven investors to hoard cash, holdings of which are at a 20-year high, according to Bank of America’s fund manager survey. Likewise, the latest American Association of Individual Investors weekly survey shows bears outnumbering bulls by two to one:

Margin debt has fallen $57bn since January, from unusually high levels:

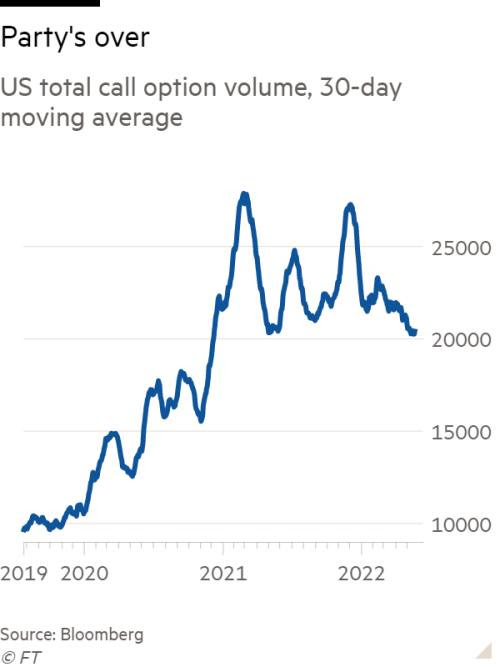

Speculation with options is quieting down, too:

Bear markets are important because they are signals to investors that they should start getting greedy. Long term prospective returns are improving, in some places quickly. This is not to say there might not be more big declines to come. But it’s time to make out your shopping list and, if you have resources to invest, these should be exciting times. It is impossible to call the bottom — no one rings a bell, as the old phrase has it. But we should be alert to signs of capitulation, a total washout. What might that look like? When we are approaching capitulation, some combination of these things tend to happen:

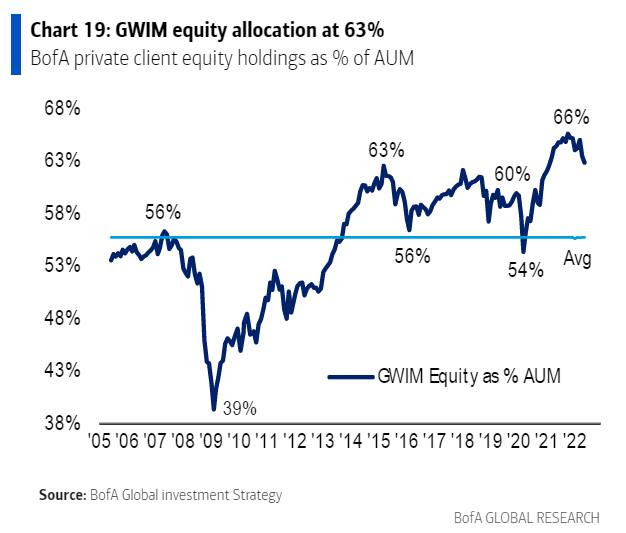

On the second bullet point, Patrick Kaser at Brandywine Global Investment Management pointed out in an email that contrarian investors were still putting money into Ark Innovation ETF, a basket of speculative tech. Despite broader markets selling off, an average $36mn a day flowed into the fund so far in May, according to Bloomberg. “That means a segment of speculators still have hope and believe in a recovery,” says Kaser. You can see residual hope in some of the indicators charted above, too. They’re heading in a pessimistic direction, but from high levels. Despair seems a ways off yet. Bearish sentiment is high but recently ticked down some, margin debt remains above pre-pandemic levels and call option volume is only back to late 2020 levels, and so on. Another example comes from Bank of America’s wealth management division, whose clients are cutting equity exposure from very high to merely high:

The stubborn remnants of optimism have limited the bear market drama, as Peter Atwater at William & Mary notes in an email: What we’ve experienced feels more like a slog than the kind of high emotion decline into a “Get me out of here, now!” capitulation climax. We’ve also seen little in terms of retail investor capitulation. Don’t get me wrong, there is plenty of worry, but especially among cultish stocks, we’ve seen no mass exit. At the same time, I sense there are many young professional investors who feel like they deserve war medals for what they have just been through. I’m not sure I have ever seen such histrionics for what at this point is just a 20 per cent drop.

|

"one of ten websites and blogs every investor should bookmark"- The Times.